$SIDU: The Final Orbit before Disaster

Houston, we have a problem; control is NOT effective

Executive Summary

This report provides a follow-up to our main publication, released on January 26, 2026, with updated information on SIDU’s Q4 and full-year 2025 earnings filing and call.

SIDU’s Q4 and full-year 2025 earnings call on March 31st only reinforced our thesis that this is a company of minimal substance that will continue to exist through shareholder dilution. During the call (which lasted exactly 30 minutes), founder and CEO Carol Craig meandered from one defense and technology buzzword to the next, claiming that her microcap company (slightly above 100 employees) had accomplished building end-to-end satellite design, manufacturing, and operational capabilities, enabling multi-domain operations through proprietary edge software, AI, and an internally developed tech stack. What was completely missing in this fanciful tale of transformation was any mention of revenue-generating contracts.

Since the publication of our initial report on the company, the three main angles we covered have not only persisted but also accelerated. Upon reviewing the company’s most recent 10-K filing, we have found that the situation has only gotten worse.

Related-party revenue has increased beyond what we originally documented.

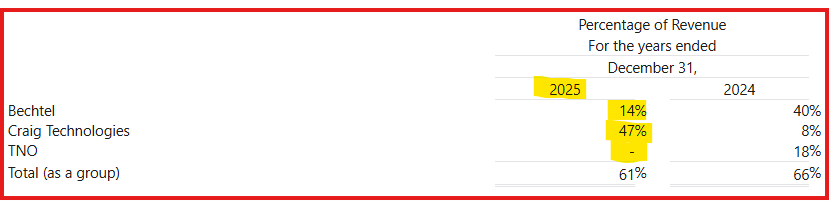

At the time of our first report, Craig Technical Consulting (or “CTC”) was the company controlled by SIDU’s CEO, Carol Craig, and accounted for approximately 47% of the company’s revenue for the nine-month period ended September 30, 2025. The full-year figure remained at the same level; however, CTC’s share of accounts receivable skyrocketed to 86%, while the two largest remaining independent customers (Bechtel and TNO) have now practically disappeared from the customer base, with Bechtel declining from 40% of total revenue to 14%, and TNO disappearing entirely from the customer concentration altogether. This confirms, once again, that Carol Craig’s position as SIDU’s best customer has only deepened since our original report.

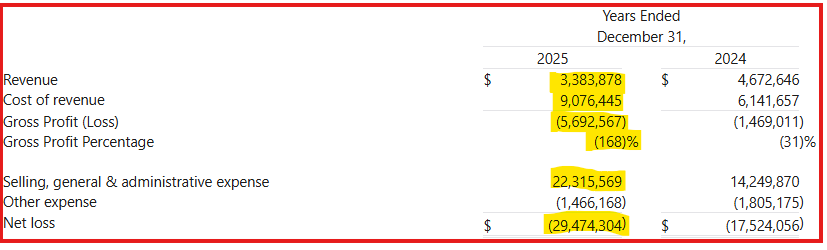

A Business that keeps on Failing. The financial details behind SIDU’s most recent annual results provide a grim insight into the company. Revenue fell 28% year over year to just $3.4 million for the full year. A figure that is dwarfed by the 48% increase in cost of revenue alone. This, combined with SG&A expenses of $22 million, results in a net loss of $29.5 million for the full year. A figure that is nearly nine times the company’s entire annual revenue.

Dilution has now turned into a permanent mechanism. At the time of our original report, we documented the January 2026 filing of a $500 million shelf registration and flagged this as the mechanism for the next dilution cycle. This was confirmed when the company entered into a $100 Million ATM sales agreement with ThinkEquity on February 26, 2026, enabling it to sell stock at market prices with no further notice of a separate offering announcement. Taking advantage of any liquidity event to dump shares into the market, leaving already diluted shareholders exposed to further dilution at any time, without warning.

The company has written off its flagship satellite, and its second satellite may be a failure. SIDU recorded a $4.5 million “Impairment Loss” on LizzieSat-1 (its first and most important satellite) after failing to re-establish contact with the spacecraft and initiating decommissioning protocols after just 18 months in orbit. To put that in perspective, this “Write-off” of their flagship satellite represents more than the company’s entire revenue for the year ended 2025.

Worse, the company’s second satellite, LizzieSat-2, is still not commissioned, despite being launched in December 2024. While Craig characterized the LizzieSat-2 as “still in commissioning”, the average time for a satellite in a similar orbit is 8-12 weeks, not 15 months. While we don’t have technical data confirming that Lizzie Sat-2 is a write-off, the odds of the satellite becoming operational this late are low. Finally, the initial commissioning of LizzieSat-3 reveals on-orbit capabilities–AIS tracking and mounting a commercial optical sensor–that were new and interesting over a decade ago. To put this in perspective, multiple universities’ satellite clubs have launched multi-payload satellites, including those with AIS tracking and commercially available optical sensors.

Most critically, the company has certified in its own filing that its internal controls are NOT effective. This comes in direct contrast to the FY2024 10-K, in which management disclosed the same controls as effective. The FY2025 10-K status of “NOT effective” is damning, meaning that, as of today, the company’s top management cannot reliably ensure that the financial information required to be disclosed is reported, recorded, or processed accurately. Meaning that for investors who rely on narratives like the Lonestar contract, SHIELD IDIQ, and the company’s satellite fleet, the company is now telling them it cannot guarantee that these disclosures are true. This is a glaring and significant point for investors.

Industry Expert Perspective (Follow-up interview)

For this follow-up report, we returned to the same senior industry expert whom we interviewed for our original publication. This space and satellite expert has more than two decades of experience in the aerospace and satellite sector, both in commercial and government roles, and has requested to remain anonymous. This source remains familiar with Sidus Space and its competitors and markets, has spoken with several company executives (including Craig herself), and has listened to Craig speak on multiple occasions.

“SIDU is a dumpster fire. 2025 comps on everything… revenue, margin, cost of sales, loss per share, all significantly worse than 2024. The only bright spot for the company is that they have $43.3 million of cash, and that’s entirely through equity raises (dilution) in Q3 and Q4.”

This aligns with the audited figures filed in their most recent 10-K. Revenue down 28% year over year. Cost of revenue 48% up year over year, a gross margin of -168%, and a net loss of $29.5 million for the year.

“The $120 million contract with Lonestar Data Holdings is questionable. Lonestar is a startup that only recently closed a small Series A round, and is currently in no financial shape to fulfill the total terms of its contract with Sidus. Additionally, Lonestar faces several other extremely well-funded competitors who have better tech and are further along–to include Starcloud (valued at over $1B), which has actually already trained an LLM in space, Google, Aetherflux and Aethero. Axiom Space (worth $2.5B in its latest funding round) also deployed its Data Center Unit-1 on the International Space Station in the fall of 2025, and launched two additional orbital data center nodes in January. Absent a major breakthrough, Lonestar is not a significant nor interesting company in the space datacenter market, and there is little reason to expect they will be able to successfully compete. Putting these two small companies with no differentiating or compelling technology together does not increase the odds either will be successful.”

The Lonestar contract has been the centerpiece of SIDU’s narrative since 2024. Our experts’ assessment of Lonestar, a financially distressed startup competing in a segment now targeted by well-financed, established big players, raises a key question. What happens to SIDU’s flagship opportunity if Lonestar fails to survive? The 2025 10-K discloses only an “initial milestone payment” with no number, no disclosure, and no commitment to a specific number, with the launch of LizzieSat-5 (supporting the Lonestar contract) vaguely described as “sometime in late 2026.”

The current public record around Lonestar does not resolve that uncertainty. SIDU’s latest year-end materials continue to present the Lonestar relationship as a $120 million lunar manufacturing program tied to LizzieSat-5, yet the most recent public Lonestar capital event was a January 2026 raise of only $6.6 million, announced together with a leadership change in which Stephen Eisele became chief executive officer, and founder Chris Stott moved to executive chairman. Lonestar also continues to describe its Freedom payload on Intuitive Machines’ Athena mission as having “performed flawlessly.” NASA states that Athena came to rest on its side, that this prevented full operation of the drill and other instruments before battery depletion, and that the mission ended early. Intuitive Machines likewise described a lander that came to rest on its side and did not return to operations. The customer tied to SIDU’s flagship lunar narrative is therefore still presenting both its capital position and its most visible recent mission in ways that do not remove the central question around the Lonestar opportunity.[l][m][o]

“The SHIELD contract for “Golden Dome” now has 2,440 prime awardees; only 23 companies who applied to this effort were denied, a fact that should not provide shareholders any level of comfort. Additionally, several dozen other satellite manufacturers who will be direct competitors to SIDU are also awardees–and many of them have better solutions, better talent and bigger facilities. Several other dozen have the software, ground command centers and other capabilities SIDU claims to have, but better. Importantly, no task orders have even been initially issued, despite the IDIQ awards being announced 4 months ago. Some government officials are privately indicating that any task orders will be further delayed by up to three more months, making it highly unlikely that any of those funds will hit any company before Q3 2026.”

In our initial report, we flagged this as a legitimate concern. SIDU announced its SHIELD inclusion as a headline, alongside the program’s $151 billion total ceiling. However, this is a program-wide figure, distributed across thousands of competitors (+2,400 awardees and essentially nothing more than a fishing license). Additionally, the first orders have not even been issued, while the timeline has been pushed further out, and there is no guarantee that SIDU will ever get even a small piece, either as a subcontractor or a meaningful contract related to SHIELD.

The conflict of interest is also particularly obvious in the Missile Defense Agency’s SHIELD IDIQ contract, which Craig touted extensively as an accomplishment. Her other company, Craig Technologies, is also an awardee on the same contract; as a certified Woman-Owned Small Business, it will have a contracting preference over SIDU. Given the extensive overlap between what both companies do, shared facilities, and, in some cases, the workforce, Craig Technologies is actually quite an effective competitor to SIDU. Given that SIDU is a public company and Craig is at least the majority owner of Craig Technologies, structurally, she is likely to personally benefit more if any SHIELD contracts are awarded to Craig Technologies rather than to SIDU. To date, we are not aware that Craig has ever addressed this conflict of interest.

“The Tobyhanna contract is extremely small, very low-margin, and not the basis for scaling any meaningful work. Importantly, it is also counter-factual to Craig’s central transformation theme–that SIDU will pursue only high-margin government and commercial work, and deliberately go away from low-margin government contract manufacturing.”

Similar to the SHIELD IDIQ, this small contract also has multiple other awardees (a total of 9), minimizing the amount of work that will go to any one company. Furthermore, the work described in the contract is the kind Craig Technologies would certainly pursue. If any task orders on the Tobyhanna contract are awarded to SIDU, SIDU could simply subcontract that work to Craig Technologies, minimizing the bottom-line impact to SIDU. This would be consistent with our main thesis that Craig is both SIDU’s best customer and that the quality of revenue is extremely concentrated and heavily identified as a circular money play. This is the epitome of self-dealing and a huge red flag. The 10-K also does not disclose the contract’s dollar value, margin, or guidance. Regardless, the size of the contract will not materially impact SIDU’s financial trajectory.

Moreover, SIDU’s own disclosures do not maintain consistency in the Tobyhanna award description. The company’s September 29, 2025, award release and its April 1, 2026, full-year results release both describe Tobyhanna as a five-year IDIQ. The 2025 10-K, however, describes the same award as a ten-year IDIQ. The September 2025 release also states that individual task orders are capped at $750,000 and awarded competitively on a best value or trade-off basis. For a contract already structured as a competitive task-order vehicle rather than a fixed, committed award to SIDU, even the basic term of the award is not described consistently across the company’s own recent materials.[q][r][s]

“The rest of the announcements… the MOU’s, the partnerships, all of it… have zero revenue behind them.”

A detailed review of their most recent 2025 10-K reveals that the filing references with Reflex Aerospace, Saturn Satellite, Vorago, and Little Place do not appear in the revenue breakdown. They are mere non-binding expressions of intent. They are only there to generate press releases without any cash flow numbers, which means that they are fundamentally zero.

Even some of SIDU’s more technical NASA-adjacent announcements shrink on inspection. In December 2025, SIDU announced a subcontractor role with MobLobSpace on a NASA SBIR radar initiative hosted by LizzieSat. NASA’s own abstract identifies MobLobSpace as the prime awardee on a six-month Phase I study with an estimated technology-readiness progression of only TRL 2 to 3, while SIDU’s role was to provide host-spacecraft requirements for possible payload integration. This was therefore an early-stage concept study in which SIDU was a subcontractor, not a larger operating contract awarded to SIDU itself.[t][u]

The Worsening Financial Situation

The financial details behind SIDU’s most recent earnings are particularly grim. The most recent 10-K filing for the year ended 2025 shows not only that SIDU remains a pre-revenue company, with revenue declining while losses widening. The central commercial narrative rests on a single large contract with a pre-revenue startup company. Nearly half of the revenue comes from the CEO’s private company, and raising equity capital has remained the primary way to fund operating losses.

Revenue keeps plummeting, down 28% from the previous year, totaling only $3.4 million for the whole year 2025. To put this in comparison, the company spends nearly THREE times more on payroll alone ($9.97 million) than it generates in annual revenue.

Cost of revenue also skyrocketed 48% during the same year, meaning that for every dollar SIDU earns, it spends $2.68 just to deliver it. The combined effect of declining revenue and rising costs widened the gross loss to negative 168%, which means the company not only fails to profit from its operations, but it actively destroys shareholder value with every dollar of business it conducts.

This, combined with more than $22 million in selling, general, and administrative expenses, produced a net loss of $29.5 million for the full year 2025, an amount that represents nearly nine times the company’s entire annual revenue. To put into perspective, for every dollar SIDU earned in 2025, it lost approximately $8.72. The company keeps burning capital at a rate that no narrative, contract announcement, or satellite launch can sustain.

Craig Technologies (owned by Carol Craig) accounted for 47% of 2025 revenue, a massive jump from 2024 numbers, which, in itself, as we pinpointed in our previous report, is consistent and increasing with quarterly numbers, representing a potential revenue sustainability risk and governance failure. In the previous 2024 numbers, the customer concentration ranged from 3 customers (Craig Technologies). However, now in 2025, TNO has completely left the revenue base, and Bechtel (the previous largest independent customer) has dramatically reduced its business with SIDU.

According to the SEC, Craig earned total compensation of $559K in 2024 (broken into $325K base and $234 “other”). Her 2025 base salary increased to $400K.

Even more, the 2024 filing disclosed that Carol Craig committed approximately 70 hours per week to Sidus. The 2025 filing says 50 hours. Her time at Sidus decreased as her company’s revenue to Sidus increased, indicating that her responsibilities at Craig Technologies may limit her ability to devote time to SIDU and negatively impact SIDU’s ability to implement operations.

Source: SIDU Form 10-K year ended December 31, 2025

Perhaps the most significant year-over-year change has been that the top management has certified that disclosure controls and procedures are now NOT EFFECTIVE. This comes as a stark change from the 2024 10-K, which at the time was reported as effective. This is a binary certification required by SOX law that, as of today, has been reversed.

The auditor (Fruci & Associates) flagged revenue recognition as a critical audit matter requiring a “high degree of auditor judgment.” These two facts together (ineffective controls and highly complex revenue recognition) represent a risk that was not present in the previous filing.

That lack of control is not merely theoretical. The company’s subsequent public materials continued to contain basic inconsistencies. In the January 5, 2026, board-change 8-K, the filing body states that two directors resigned effective January 1, 2026, while the attached exhibit states that they concluded service, effective January 1, 2025. In the February 26, 2026, ATM prospectus, SIDU used different Class A share counts within the same offering document set. In the January 20, 2026, S-3, the company separately stated that 66,419,851 Class A shares and 100,002 Class B shares were outstanding as of that date. In the April 1, 2026, year-end earnings exhibit, the balance sheet duplicated related-party receivable and contract-asset lines and included boilerplate about “expected trading commencement and closing dates” in what was otherwise a financial results release. Read together with management’s year-end conclusion that internal control over financial reporting was not effective, these are specific disclosure errors appearing in the company’s most recent public materials.[h][i][j][k]

Fugazi Research Verdict: $SIDU Remains Fundamentally Uninvestable

When we first published our initial report in January 2026, we highlighted the main structural threats that, taken together, described a company designed to extract shareholder capital and burn through dilution rather than commercial performance. Now, after reviewing the company’s most recent 10-K and its full earnings call, our assessment has not only not changed, it has hardened.

Every problem we initially identified has persisted or worsened: related-party revenue concentration, extreme dilution, the disappearance and erosion of independent customers, declining revenue, increasing operational costs, an increasing cash burn rate, and full reliance on the dilution mechanism. The financial results require no further explanation, but shareholders should be aware that the balance will continue to decline at the current operating burn rate, while the ATM facility will continue to be replenished through shareholder dilution.

Their satellite fleet, which the company uses as its perpetual technical narrative, has sustained material losses that the market has not identified. The company has offered no coverage and no technical explanation for the decommissioning or the lack of commissioning of their satellites. But the company’s own filings now document these operational and existential threats.

Most significantly, management has certified in its own filing that its disclosure controls and procedures are not effective. The auditor simultaneously flagged revenue recognition as a critical audit matter requiring a high degree of judgment. The combination means that the figures underlying every narrative management has offered (IDIQ contract, Lonestar, Satellite Fleet) now carry an explicit disclaimer from the company’s own top executives that those disclosures cannot be guaranteed to be accurately recorded or reported.

The evidence now shows that a company that has become more structurally dependent on its CEO’s private firm has failed to deliver its core business through decommissions and write-offs, has kept diluting shareholders, and has certified that its financial disclosures are ineffective. We called it in January, and we reiterate our findings today. SIDU’s shares are fundamentally uninvestable and of near-zero value.

[h] Sidus Space, Inc. — Form 10-K, Annual Report FY2025, SEC Filing (March 31, 2026)

[i] Sidus Space, Inc. — Form S-3, Shelf Registration Statement, SEC Filing (January 2026)

[j] Sidus Space, Inc. — Form S-3, Registration Statement, SEC Filing (January 20, 2026)

[k] Sidus Space, Inc. — Press Release: Full Year 2025 Financial Results (April 1, 2026)

[l] Sidus Space, Inc. — Exhibit 99-1, SEC Filing (2026)

[m] Data Center Dynamics — “Lunar data center firm Lonestar Data raises $6.6M, swaps CEO” (2025)

[o] NASA — “NASA Receives Some Data Before Intuitive Machines Ends Lunar Mission”, NASA.gov Press Release

[p] Intuitive Machines — IM-2 Mission Page

[q] Sidus Space, Inc. — Press Release: “Sidus Space Awarded Five-Year IDIQ Contract to Support”, Investor Relations (2025)

[r] Sidus Space, Inc. — Press Release: Full Year 2025 Financial Results (April 1, 2026) (same source as [k])

[s] Sidus Space, Inc. — Form 10-K, Annual Report FY2025, SEC Filing — Full Filing Text (March 31, 2026) (same filing as [h], alternate format)

[t] Sidus Space, Inc. — Press Release: “Sidus Space Secures Subcontractor Role with MobLobSpace on”, Investor Relations

[u] NASA — SBIR 2025 Phase I Selection Abstract Archive, NASA.gov (January 2024)

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions—long, short, or otherwise—in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.