$WATT: "Influencers" Running Away with Your Money

Follow Up Report on Dilution, Distribution, and Participation (Views Included)

Executive Summary

This report provides a follow-up to our main publication, released on March 24, 2026.

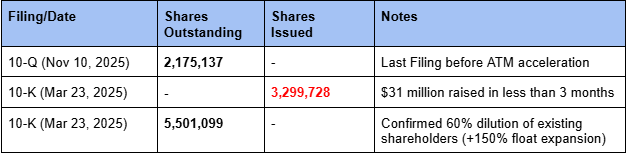

Following the publication of our report and the company’s 10-K filings, we discovered that between January 2 and March 23 of the current year, WATT issued approximately 3.3 million new shares. This was done through their current ATM offering, expanding the float by approximately 150%. Taking the 2.2 million shares reported on their 10-Q filing (November 10, 2025) to 5.5 million shares reported on their latest 10-K filing (March 23, 2026).

One of the theses of our main report was that WATT was “overwhelmingly driven by shareholder dilution rather than operating performance,” and this proved true once again in their latest filing.

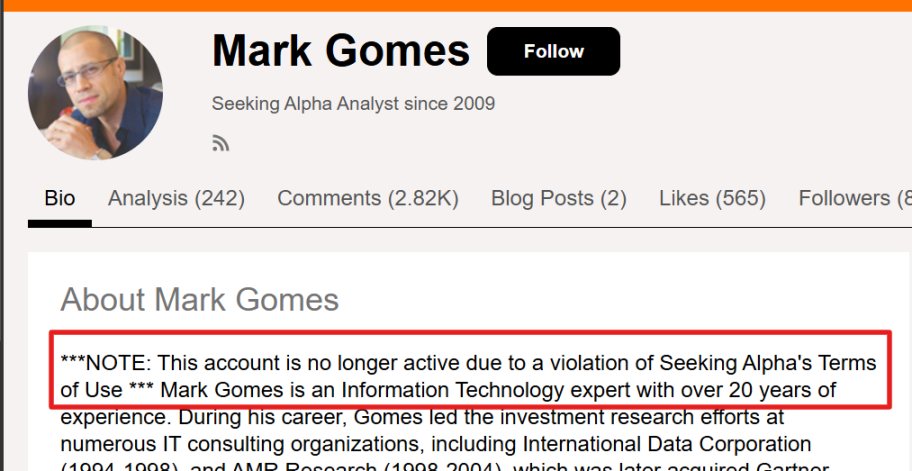

Adding to this pattern, our researchers identified Mark A Gomes, a stock promoter who has been in trouble with the SEC for acting as an unregistered investment advisor operating under the X (formerly Twitter) handle @MoneyMarkStocks, who has promoted WATT during that period and continues to do so. Gomes was the subject of an SEC enforcement action in 2017, charged with recommending stocks to followers while simultaneously selling his own shares without disclosing the sales. He also operated as a Seeking Alpha contributor, suspended since 2017 for what the permanent notice expresses as “deactivated due to a violation of the platform’s terms of use.”

The combination of these elements confirms the basis of our short thesis.

The Confirmed Dilution

The most important datapoint of our report was the share count explosion during the first quarter of 2026. The table below reveals that the company did not use the ATM during stock lows. Rather, they took advantage of extremely elevated prices around $9 or more to tap the ATM, as the amount the company raised vs. the number of shares issued yields an average issuance price of $9.67 per share. This coincides with the high-volume trading day on January 13, when more than 5 million shares were traded, the exact same day the PR was released. (This represented at the time more than twice the shares outstanding of the company.) Taking advantage of these liquidity events, the company sold equity on high-volume trading days from January 13 to March 24, 2026.

Source: WATT Form 10-K year ended December 31, 2025

Source: WATT Form 10-Q quarterly period ended September 30, 2025

The Distribution Layer

Our initial report covered the stock, part 2 covers the distribution layer around the stock.

This sits one layer above WATT’s filings. Small-cap names trade on narrative flow as much as operating reality. Every company has a story. The real question is who carries it into the market, how it is framed, and what incentives sit behind the voice delivering it.

Enter Mark A. Gomes, AKA @MoneyMarkStocks, a stock commentator with a social media following actively promoting WATT to retail investors during the 83-day window in which Energous tripled its share count, and who is no stranger to SEC scrutiny.

On September 15, 2017, the Securities and Exchange Commission instituted administrative proceedings against Mark A. Gomes, resulting in a settled order (SEC Release No. 33-10414, Exchange Act Release No. 81636). The following facts are drawn directly from the SEC’s Order:

Gomes acted as an unregistered investment adviser, distributing investment recommendations through websites operated by his company (identified as ‘Company A’ in the order, registered in Delaware with principal offices in Austin, TX).

On at least five occasions between February 2014 and July 2014, Gomes purchased shares in a stock, published bullish recommendations to subscribers and followers, and then sold his personal shares within days, sometimes hours of the recommendation.

He never disclosed that he was selling shares while recommending that others buy. The SEC found this constituted a ‘device, scheme, or artifice to defraud his clients.’

Gomes willfully violated Section 17(a) of the Securities Act, Section 10(b) of the Exchange Act and Rule 10b-5, and Sections 206(1) and 206(2) of the Investment Advisers Act.

Sanctions: Cease and desist order; bar from association with any broker, dealer, or investment adviser; $130,669.90 in disgorgement; $11,882.48 in prejudgment interest; $130,669.90 civil penalty. Total: approximately $273,222.

Source: SEC, In the Matter of Mark A. Gomes, Release No. 33-10414 (Sept. 15, 2017).

Added to this his own profile on Seeking Alpha, where Gomes was a contributor from 2009, carries a permanent public notice on his author page: ‘NOTE: This account is no longer active due to a violation of Seeking Alpha’s Terms of Use.’

Seeking Alpha does not display this notice for voluntary departures or account closures. This language is specific to disciplinary removal. Seeking Alpha’s contributor terms require disclosure of holdings and prohibit conduct inconsistent with transparent investment research. The violation notice on his profile represents an independent determination that his conduct breached the platform’s standards and terms of use, separate from and in addition to the SEC enforcement action.

Source: Mark Gomes, Seeking Alpha contributor profile.

Public commentary associated with @MoneyMarkStocks, provides the live channel. The 2017 SEC administrative order involving Gomes provides the historical lens. Put the two together, and the picture is straightforward: a documented incentive backdrop, a visible retail-facing distribution route, and a message architecture built to move attention.

Why It Matters

Small-cap narratives do not spread on merit alone. They spread because somebody packages them, sharpens them, and pushes them into the right audience at the right moment.

The company supplies the raw material, and the distribution layer makes it trade.

That is where most investors lose the plot. They read the filing, then assume the market is trading the filing. It usually isn’t. Retail is far more often trading the version of the story that reaches them through commentary, tone, and timing. Once a name depends on market participation, distribution ceases to be background. It becomes part of the capital structure.

The Historical Lens

The 2017 SEC administrative order matters because it documented a familiar mechanism: stock recommendations followed by selling, with no disclosure of intent to sell at the time of those recommendations. The matter was settled without admission or denial.

That record does not prove anything about present conduct. It does something more useful. It establishes that public stock commentary can sit inside a real incentive structure, and that communication and trading do not have to move on the same timeline, while documenting a pattern of prior conduct and current promotional activity for the purpose of informing retail investors.

Once the SEC has laid out the basic architecture, subsequent stock promotions must be read with that architecture in mind. Not as gossip, not as outrage, but more as a structure. For a market operator, that is the key takeaway.

The Channel

The current channel is public and identifiable.

The @MoneyMarkStocks YouTube presence, along with its associated social media accounts, operates as a retail-facing distribution platform for small-cap narratives. The channel presents itself as educational content. The content is framed as expertise-driven analysis, delivered to a recurring retail audience through a consistent format. The stated intent is education. The functional output is attention.

No one needs a conspiracy theory to understand what is happening. A visible platform with a repeat audience and a small-cap focus already tells the story. The only question is how the message is constructed.

The Mechanics

The transcripts do not read like research. They operate like distribution.

The first move is certainty. The listener is not given a wide range of competing outcomes. The presentation narrows the field and hands over a convincing read.

The second move is urgency. Time gets compressed. The focus shifts to the immediate horizon, the next few days, the next turn in the story. That compresses the distance between hearing the pitch and acting.

The third move is asymmetry. The listener is placed in the favored seat: early, informed, ahead of the crowd. That framing is powerful in speculative names because it lets buyers feel smart before they need to be right.

The fourth move is authority. The speaker adopts the posture of a market interpreter rather than an observer. That matters because authority carries the rest of the message. Certainty without authority sounds reckless. Urgency without authority sounds promotional. Authority makes both feel actionable.

None of this is accidental. It is how small-cap narratives are delivered when the job is not merely to describe a stock, but to create receptivity around it.

Where WATT Fits

WATT matters here as a case study in narrative distribution, not as a referendum on the technology.

Part 1 already covered the structure behind the stock: capital needs, financing dependence, and participation. Part 2 addresses the missing piece: how participation gets recruited in the real world.

A stock that depends on market appetite becomes highly sensitive to the way its story is carried into the market. That is the connection. Once belief matters, the delivery system matters.

The distribution layer is what turns a speculative setup into something retail can act on.

The Real Read

There is a tendency in small caps to separate the company from the stock and the stock from the story. That separation does not hold.

The company produces filings, and the market trades narrative.

The distribution layer then bridges that gap.

That bridge is built with channel, tone, timing, and incentive. The SEC order supplies the historical incentive context. The public platform supplies the route to market. The transcripts supply the operating language.

That is enough to identify a functioning distribution layer around the name.

An investor looking only at fundamentals misses half the trade. In this part of the market, the narrative pathway matters every bit as much as the financial output. Sometimes more.

Conclusion

Small-cap stocks do not move on numbers alone.

They move on who frames the story, who delivers it, and how quickly it reaches a receptive audience. That is the edge. Not the biography or the noise, but the mechanism.

Part 1 explained the stock.

Part 2 explains how participation is pulled in.

The filings show the supply. The market absorbs the story.

A YouTube video does not change the fundamentals of a company. It does, however, influence how that company is perceived, discussed, and traded in the market.

Once a stock depends on belief, how that belief spreads through the market becomes part of the trade. That process is visible, it follows a structure, and it is not accidental.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions—long, short, or otherwise—in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.

Where's your research to dispute Mark's research? Instead you would rather personally attack. This doesn't say much about you. Your problem is that you live in the past in regards to WATT and MARK. People who live in the past fail to see the future and that can be costly as you will likely find out. Mark challenged you to debate WATT. Instead you continue to attack instead. Again, doesn't say much about you or your research.

You must have a huge short position to have to write such a piece. You quote facts about Mark Gomes which he doesn’t dispute but he is open and transparent and goes to great lengths to explain the situation which happened 10 !! years ago. He is transparant why he believes WATT is a great buy and invites you to discuss your short report with him. Instead you just update your smear article. Both the unfortunate issue Mark Gomes encountered and the situation of WATT you describe in the other article is 100% rear view mirror. You don’t counter the CURRENT facts Mark Gomes uncovered with his research. Probably because you can’t and are stuck with a large short position. Good luck with that.