$WATT: A Decade of Promises, A Business Funded by Dilution

Wireless power for devices, drained batteries for investors

Fugazi Research Analysis

Energous Corporation (WATT) is a low-revenue, cash-burning, dilution-dependent company that develops and sells early-stage wireless charging for low-powered mobile devices and RF transmitters (used for inventory management). While revenue grew from a very low base, the company has not yet demonstrated a self-sustaining operating model and remains primarily dependent on equity sales to fund operations.

The company’s roots trace to entities with significant dilution histories. Majority shareholder DivineWave Holdings, owned by founder Michael Leabman (also founder of Movano Inc.), was associated with similar patterns of heavy ATM usage, reverse splits, and value destruction.

WATT has a history of aggressive dilution, using various equity actions to raise cash a staggering 21 times since 2019, most notably through at-the-market (ATM) registrations. One particularly active offering period increased outstanding shares by more than 140% over just 2 months, followed by a 30-to-1 reverse split to regain compliance with NASDAQ listing requirements.

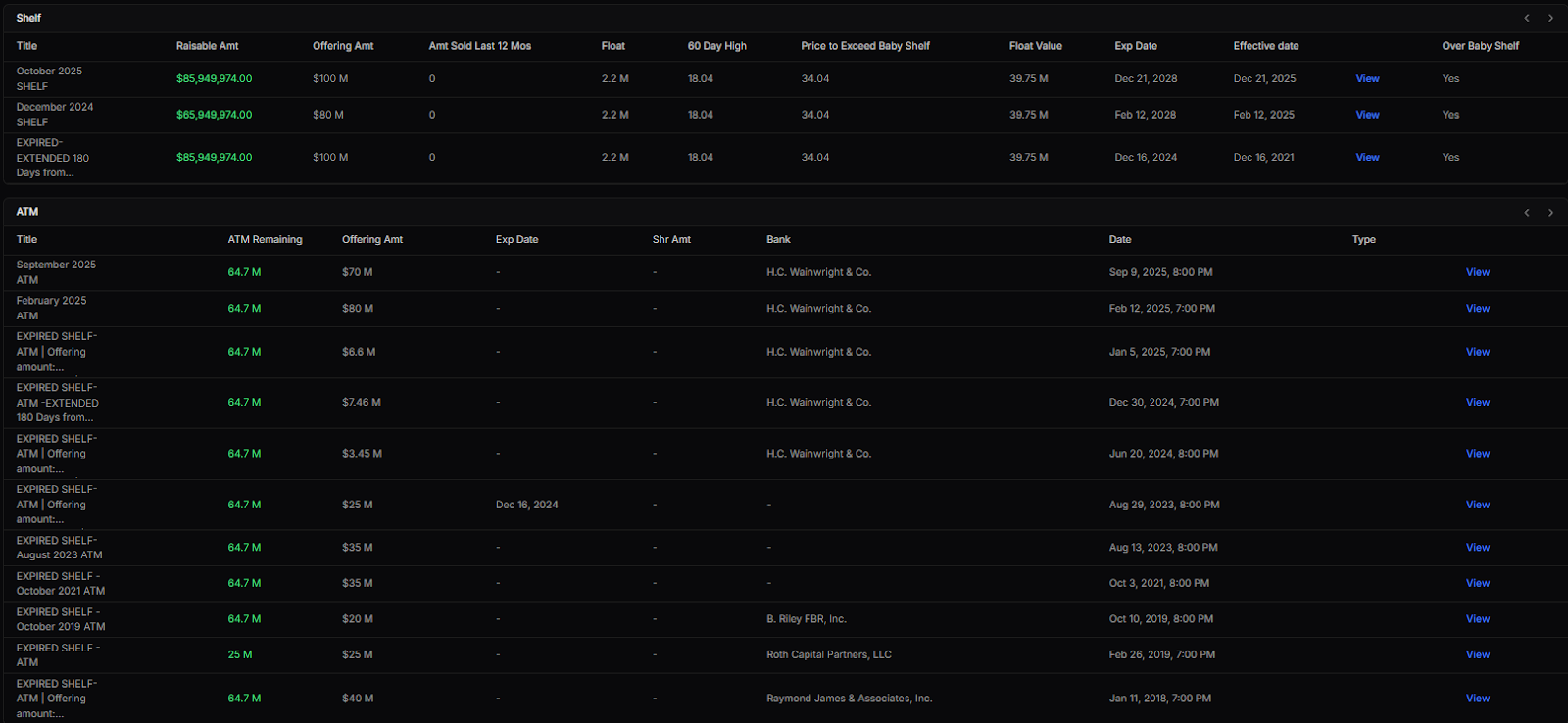

A $64 million remaining ATM (3 times the size of its current market cap) provides the company with a pre-existing tool for additional equity issuance: one they have a rich history of using, given their inability to improve sales, business performance, or streamline revenue. The net positive cash balance from cash flow is fully from equity and warrant issuance.

WATT has burned through enormous amounts of capital with little to show for it. As to their latest filing, the company confirms having accumulated a total deficit of approximately $408 million, reflecting a prolonged gap between commercialization efforts and sustainable revenue growth, despite more than a decade of promising commercial breakthroughs and contracts that have yet to be translated into sustainable increased revenue.

The company’s governance structure raises serious concerns about significant oversight and internal control gaps, as Burak serves both the CEO and CFO, eliminating an important layer of financial accountability and independent oversight. Additionally, the Board only has four members, including Burak, which is small for a publicly traded company. This concentration of responsibility and power with Burak, coupled with a small and likely distracted board, certainly raises questions as to how much board oversight is actually being exercised, particularly given Burak’s past performance and legal issues with her employers.

WATT’s leadership has a very poor track record. Mallorie Burak, the CFO/CEO of WATT, has a history of working at companies that ultimately fail. She was the CFO at Knightscope Inc. (a currently listed company with a similar dilution pattern, the same underwriters, and the same split history that turned out to be a serial diluter), leaving shareholders with a 99% loss of their investment. Burak was also involved in litigation with Thin Film Electronics following her termination. Public records show that she was involved in litigation in Santa Clara County (Case No. 20CV367979) after her departure. Allegations surrounding her termination included forecasting errors and deficiencies in internal financial controls.

Source: Santa Clara County Superior Court, Case No. 20CV367979WATT’s newly appointed Chief Accounting Officer, Gregory Sadikoff, previously worked under Burak at Knightscope, confirming a network of acquaintances tied to serial diluter companies with a history of substantial shareholder value destruction.

Based on the current filing record, given the company’s financial situation, including high operational costs, the persistent overhang of potential dilution, history of aggressively using highly dilutive instruments, and the lack of capacity to self-fund its operational model, we consider that WATT’s shares are uninvestable and lack fundamental support at current valuation levels.

$WATT Financial Summary

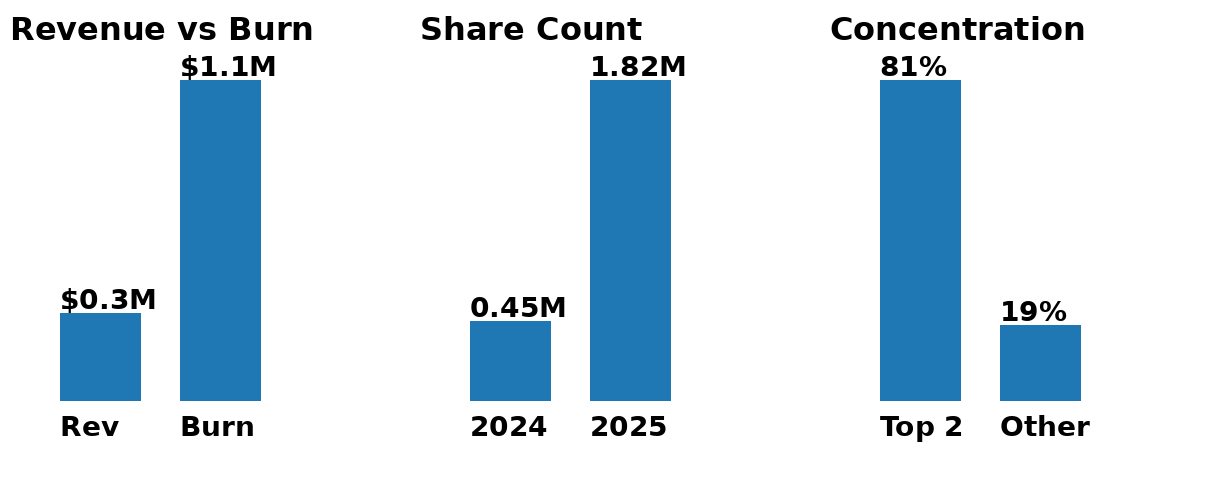

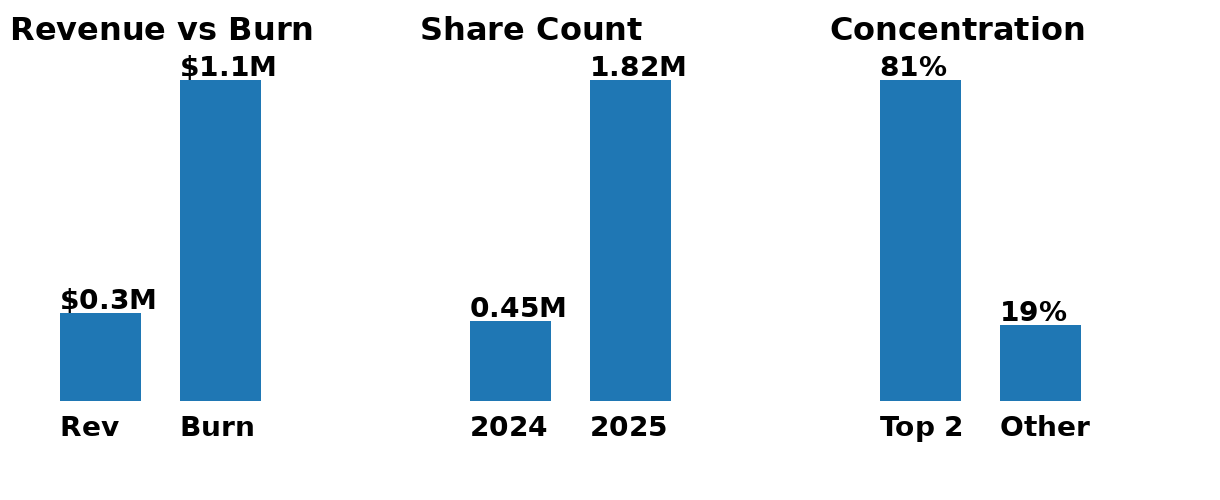

For the nine months ended September 30, 2025, revenue totaled $2.6 million, but net loss for the same period totaled $8.3 million, meaning the company lost more than $3 to generate $1 of revenue, or a -319% net margin.

At current operating levels, the company generates approximately $290K in monthly revenue while burning approximately $1.1 million in cash, indicating that continued operations rely on stock issuance as the primary source of funding.

Cash increased from $1.4 million to $12.9 million for the 9-month period 2024 vs 2025. However, $21.6 million of this cash came from ATM sales, warrant exercises, and equity issuances, highlighting that the company’s liquidity is overwhelmingly driven by shareholder dilution rather than operating performance.

Outstanding shares increased from approximately 12.35 million as of December 30, 2024, to 2.3 million as of March 08, 2026. On a split-adjusted basis, outstanding shares increased approximately 458% over the period, reflecting rapid re-expansion following the company’s 30-to-1 reverse split.

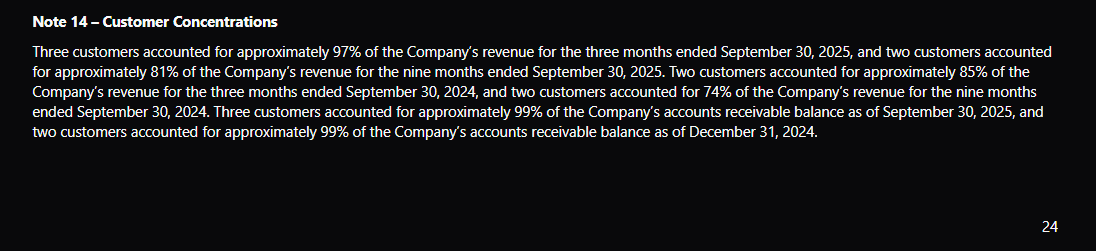

Two customers account for more than 81% of the company’s revenue, and three customers account for 99% of the company’s accounts receivable for the nine-month period ended September 30, 2025, indicating extreme customer concentration risk and a very fragile revenue base.

In their latest 10-K, the company acknowledges it has no history of generating meaningful product revenue, may never achieve profitability, may be unable to demonstrate the commercial feasibility of its technology, and warns that it may fail to meet Nasdaq’s listing requirements.

Source: WATT Form 10-K year ended December 31, 2024,

Source: WATT Form 10-Q quarterly period ended September 30, 2025

Executive Summary

WATT’s core business is the development of RF wireless power transmitters for low-energy devices and sensor tags for supply chain applications. After more than a decade of commercial promises, the company has yet to demonstrate a self-sustaining operating model, accumulating over $400 million in deficit along the way. Its financials still reflect a low-revenue, cash-burning business with deeply negative margins and no clear path to profitability.

At its current scale, the business simply does not fund itself—and never has. For the nine months ended September 30, 2025, WATT generated just $2.6 million in revenue while posting an $8.3 million net loss, meaning it lost more than $3 for every $1 of revenue, with a net margin of approximately -319%. On a monthly basis, the company generates roughly $290K in revenue while burning about $1.1 million in cash, leaving its internally generated cash flow nowhere near sufficient to support operations. Despite this, management framed recent results as progress during the Q3 2025 earnings call, which coincided with a sharp short-term move higher in the stock—highlighting the gap between narrative-driven momentum and underlying financial reality.

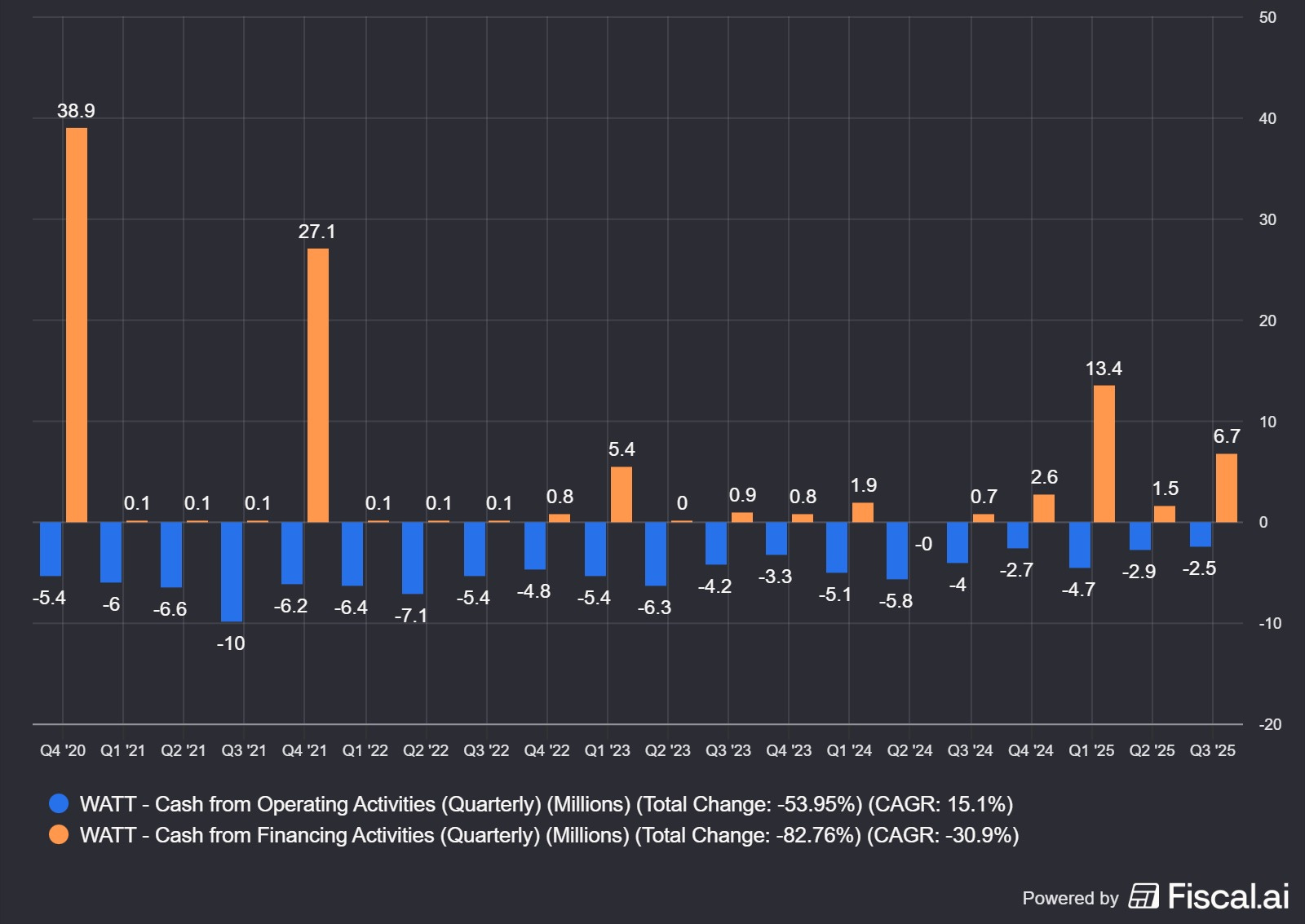

The only reason the company remains operational is continued access to equity markets. Cash increased from $1.4 million at year-end 2024 to $12.9 million as of September 30, 2025—but this was not driven by business performance. Instead, $21.6 million was raised through ATM sales, warrant exercises, and other equity issuances. In other words, liquidity came from shareholders, not customers. This pattern is not new: the company has raised capital through equity actions 21 times since 2019 and still maintains a $64 million ATM registration—an amount that is massive relative to its market capitalization and effectively ensures further dilution.

The balance sheet reflects a business that remains structurally dependent on financing. Even after recent capital raises, the company’s cash runway is limited. Management indicated that the $21.6 million raised only extended the runway by approximately 12 months, while other estimates suggest cash could already be below $6 million, though exact timing depends on ongoing financing activity.

At the same time, the revenue base itself is fragile. Two customers account for 81% of total revenue, underscoring the business’s continued concentration and instability. The company’s own 10-K acknowledges its lack of meaningful product revenue history, ongoing uncertainty regarding commercial viability, and even the risk of failing to maintain Nasdaq listing compliance. This is all against a backdrop of just ~$800K in annual revenue versus roughly $18 million in operating expenses.

Governance adds another layer of concern. Mallorie Burak serves as both CEO and CFO, a dual role that significantly weakens financial oversight—particularly for a company whose survival depends on continuous capital market activity. Her track record includes prior roles at companies such as Knightscope and ThinFilm Electronics, both of which exhibited similar dilution-heavy patterns and governance concerns. Recent executive appointments tied to her past affiliations only reinforce a pattern of leadership networks associated with repeated value destruction.

Meanwhile, shareholder dilution continues to accelerate. Shares outstanding increased from 452,533 at year-end 2024 to 1,824,844 by September 30, 2025, on a split-adjusted basis. Even after a 1-for-30 reverse split, the share count has rapidly re-expanded—highlighting a familiar cycle of reverse splits followed by renewed dilution.

After more than a decade, the conclusion is difficult to avoid: WATT is not a business being funded by operations—it is a business being funded by the market. The technology may be the story, but the financing has become the reality.

SHARE COUNT EXPANSION

WATT faces significant challenges in meaningfully scaling revenue, with an extremely limited customer base of only three entities, which account for 99% of revenue.

Minimal revenue, an unhealthy customer concentration, and a share count that keeps growing.

The cap table reflects questionable interconnections. The early cap table also contained founder-family and affiliate-linked counterparties. The 2014 S-1/A disclosed that DivineWave Holdings LLC, formed by Michael Leabman’s parents, beneficially owned approximately 20.3% of the company; that Absolute Ventures LLC, affiliated with former director Greg Brewer, held 668,337 shares purchased for $160,000; and that the company leased former office space from ProSoft Engineering, which the filing identifies as being owned and founded by Brewer. The same filing also disclosed that MS Investments, an affiliate of one of the company’s legal firms, purchased 20,050 shares for $4,800; that Cheryl Sanchez, the sister of a director and stockholder, entered into a consulting agreement at $21,550 per month; and that MDB Capital Group received a consulting warrant for 278,228 shares at an exercise price of $0.04. https://ir.energous.com/static-files/03ff2986-31df-4529-99c6-98ead5451db7

The capital structure became materially more toxic in March 2023, when WATT issued long-dated warrants with reset features severe enough that they were accounted for as a derivative liability rather than plain equity. The strike on those 2023 warrants fell from $8.00 initially to $1.66 by March 31, 2024, to $0.30 by December 31, 2024, and to $0.28 by June 30, 2025. The June 2025 filing also states that future issuances below the exercise price, including through the ATM, could trigger further downward adjustments. https://ir.energous.com/static-files/7b6b5567-cf86-46d0-ab8c-4dea68da4a79

During the first nine months of 2025, WATT disclosed approximately $18.2 million of net ATM proceeds, $0.4 million from warrant exercises, and $4.1 million from the September 2025 registered direct offering, versus approximately $10.0 million of cash used in operating activities during the same period. https://ir.energous.com/static-files/03ff2986-31df-4529-99c6-98ead5451db7

$WATT Sales and Product Challenges

The company also faces a crisis of product credibility and adoptability. Energous’s product line focuses on wireless power network technology that integrates wireless power, Bluetooth communication, battery-free sensors, and software to create a real-time communications network within a given facility. This is a highly contested vertical, and Energous’ product line ranks poorly against its competitors.

Leadership has been promising mainstream commercial adoption for nearly a decade, yet it has not achieved any such traction. In the interim, better-financed companies have captured the majority of the market, and other, more compelling technologies have been introduced, making Energous’s technology outdated. Powercast, for example, has shipped over 30 million of its units in the last decade to over 100 global customers across retail, medical, industrial, and consumer electronics. WATT, in comparison, is trying to grow minuscule sales to just a few companies with 1) a less capable product and 2) a minimal balance sheet. Yet another red flag.

The above dynamic is a massive headwind for Energous to ever make meaningful sales. The extremely tight cash position significantly erodes the possibility of large-scale commercial success, as customers need to trust that a vendor will be around for more than a few months before making large purchases. Moreover, any large commercial order will almost guarantee another dilutive equity move, simply to raise the cash needed to buy parts and then build and install the network units. Given recent cost-cutting efforts, it’s also unclear if WATT has the employee base to successfully execute a meaningful order.

The Playbook

Energous’ filings outline a clear and consistent pattern in which operating losses are funded through equity issuance rather than internally generated cash flow.

The company utilizes at-the-market (ATM) programs to raise capital opportunistically, allowing shares to be sold directly into the market over time. In addition, registered offerings and warrant issuances create additional pathways for future share issuance.

Following the August 2025 reverse stock split, which restored Nasdaq compliance without reducing the authorized share count, the company retained significant capacity to issue additional equity.

As of September 30, 2025, the company still had 200 million authorized shares, only 1.824 million common shares outstanding, approximately 1.03 million shares issuable upon warrant exercise, 78,172 shares reserved for future issuance under the 2024 plan, and approximately $64.7 million of remaining ATM capacity.

Subsequent increases in shares outstanding indicate that this capacity has already been utilized.

Warrants issued in connection with financing transactions, including pre-funded and long-dated warrants, further expand the pool of potential shares. Resale registrations allow these instruments to be converted and sold into the market, often subject to ownership caps that pace but do not prevent distribution.

This structure links operating cash burn to continuous equity issuance as the share base expands over time.

Anatomy of the Mirage

Despite reported improvements in revenue, the filing record continues to reflect a gap between top-line growth and underlying business durability. The progression in reported metrics does not yet translate into operating scale, revenue quality, or structural stability.

Minor Revenue Growth Without Customer Breadth

Revenue has increased off a low base, but lacks breadth. The current revenue base is tied to a few customers, with no clear indication of diversified demand or scalable adoption across a broader customer set. The company’s inability to obtain more than three paying customers is a clear market signal of a lack of demand for their technology. This limits visibility into the stability of that growth and raises questions about its repeatability beyond a small number of relationships.

AskEdgar - Form 10-Q

Additionally, WATT likely sits lower in the value chain than investors assume. The company has highlighted a “Fortune 10” retail deployment across thousands of U.S. locations, while partner disclosures from Wiliot and Avery Dennison suggest a broader ecosystem in which Energous provides the underlying power layer. Public materials indicate that WATT’s transmitters power Wiliot’s IoT Pixels, which are then integrated into a larger Wiliot / Walmart / Avery Dennison stack.

“Fortune 10 deployment” narrative appears overstated relative to economics.

Public disclosures suggest WATT is likely supplying a lower-value bridge-power layer within a broader Wiliot / Walmart / Avery Dennison ecosystem, rather than a high-margin platform. The company’s own figures imply ~1,500 transmitters for ~$0.3M (~$200 per unit), and despite highlighting 25,000+ units shipped, preliminary 2025 revenue was only ~$5.6M—consistent with low-dollar hardware, not scalable monetization.

Balance Sheet Improvement Through Equity Issuance & Dilution

Changes in the balance sheet reflect access to capital rather than conversion of activity into cash. The improvement in liquidity does not stem from operating efficiency or margin expansion, but from the ability to raise funds externally.

As a result, the balance sheet does not yet function as evidence of operating strength, but rather as a reflection of capital availability.Additional Equity Supply Embedded in the Structure

The capital structure contains multiple embedded pathways through which additional shares can enter the market. These are not contingent events, but structural features that can be activated over time.

This creates a forward supply profile that extends beyond current outstanding shares, where new equity can be introduced alongside ongoing funding needs.The Disconnect

The filings describe a company where reported progress exists, but remains narrow in scope, while balance sheet changes are not rooted in operating conversion, and the capital structure continues to accommodate future expansion of the equity base.

The result: a disconnect between what is reported and what is structurally sustained.

Valuation and Downside

Based on current disclosures, the company retains approximately $64 million of remaining ATM capacity, compared to a market capitalization of approximately ~$40 million.

This implies that the company can issue equity that represents more than 100% of its current market value.

Assuming continued operating cash burn at current levels with less than 6 months of runway, the company would require ongoing access to capital markets to fund operations. The ATM structure allows this funding to occur incrementally, but does not eliminate the cumulative effect on the share base.

As a result, even if revenue continues to grow, equity issuance required to sustain operations may offset or exceed any improvement in underlying business performance.

The valuation, therefore, reflects not only the current business but also the embedded capacity for future equity issuance, which may continue to expand the share base over time.

Governance and Track Record

The company’s governance structure and management background raise concerns around oversight, capital allocation, and financial controls. The current CEO also serves as CFO, concentrating operational and financial reporting responsibilities in a single role and reducing the separation between capital allocation decisions and independent oversight.

Proxy disclosures show that Mallorie Burak previously held executive roles at ThinFilm Electronics and Knightscope. ThinFilm filings indicate her employment was terminated in May 2020. Public records further show that she was involved in litigation with Thin Film Electronics in Santa Clara County (Case No. 20CV367979) following her departure. Allegations surrounding her termination included forecasting errors and deficiencies in internal financial controls. Separately, Knightscope filings disclosed material weaknesses in internal control over financial reporting, including limitations in accounting resources and SEC reporting expertise. Energous’ current Chief Accounting Officer, Gregory Sadikoff, also previously worked alongside Burak at Knightscope, reinforcing overlap across management teams with similar histories.

https://www.sec.gov/Archives/edgar/data/1575793/000110465925041253/tm252608-4_def14a.htm

While not determinative on their own, third-party research (e.g., Capybara Research, 2023) has raised similar concerns regarding governance, accounting oversight, and capital structure practices in comparable companies involving overlapping leadership. Company filings also note delays in commercialization tied to regulatory approvals and customer-side factors.

Compensation remains highly elevated relative to business scale. The 2025 proxy shows Burak’s 2024 total compensation at $849,551 and former CEO Cesar Johnston’s at $1,343,485, compared to approximately $0.8 million in annual revenue and roughly $12,000 in gross profit in 2024. The top two executive compensation figures alone exceeded total revenue and were multiple times gross profit. Burak’s compensation included $379,849 in salary, a $150,000 guaranteed bonus, multiple additional bonuses, and $135,452 in stock awards. Johnston’s severance was also significant, with Q1 2024 severance expense totaling $1.563 million—approximately 2,442% of quarterly revenue.

https://www.sec.gov/Archives/edgar/data/1575793/000110465925041253/tm252608-4_def14a.htm

The company has also historically used equity as a transactional currency. In March 2025, Energous amended its headquarters lease, downsized its space, and issued 75,000 shares to the landlord as partial consideration. This follows earlier instances, including a 2014 issuance of 41,563 shares (valued at $500,000) tied to its San Jose lease. These patterns reflect ongoing liquidity pressure and reliance on equity beyond traditional financing channels.

https://ir.energous.com/static-files/03ff2986-31df-4529-99c6-98ead5451db7

The Fugazi Verdict

Based on public filings, $WATT shows improving reported metrics from a low base, limited operating depth, concentrated revenue, and a capital structure that continues to enable equity issuance alongside funding needs.

After more than a decade, WATT has not built a business that funds itself—it has built one that funds itself through shareholders.

Unless that dynamic changes, continued dilution is not a risk; it is the model. The technology may charge devices, but the model charges shareholders.

We stand firm in our view that the company is uninvestable and will likely turn shareholders into bagholders, with shares likely to revisit single-digit pricing.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions—long, short, or otherwise—in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.

I remain a longstanding bull on WATT's share count. To the moon...

How is your WATT short coming along? Pretty painful I guess. Next time maybe do a more thorough research into the current and future of the company instead of focusing on the past 😉