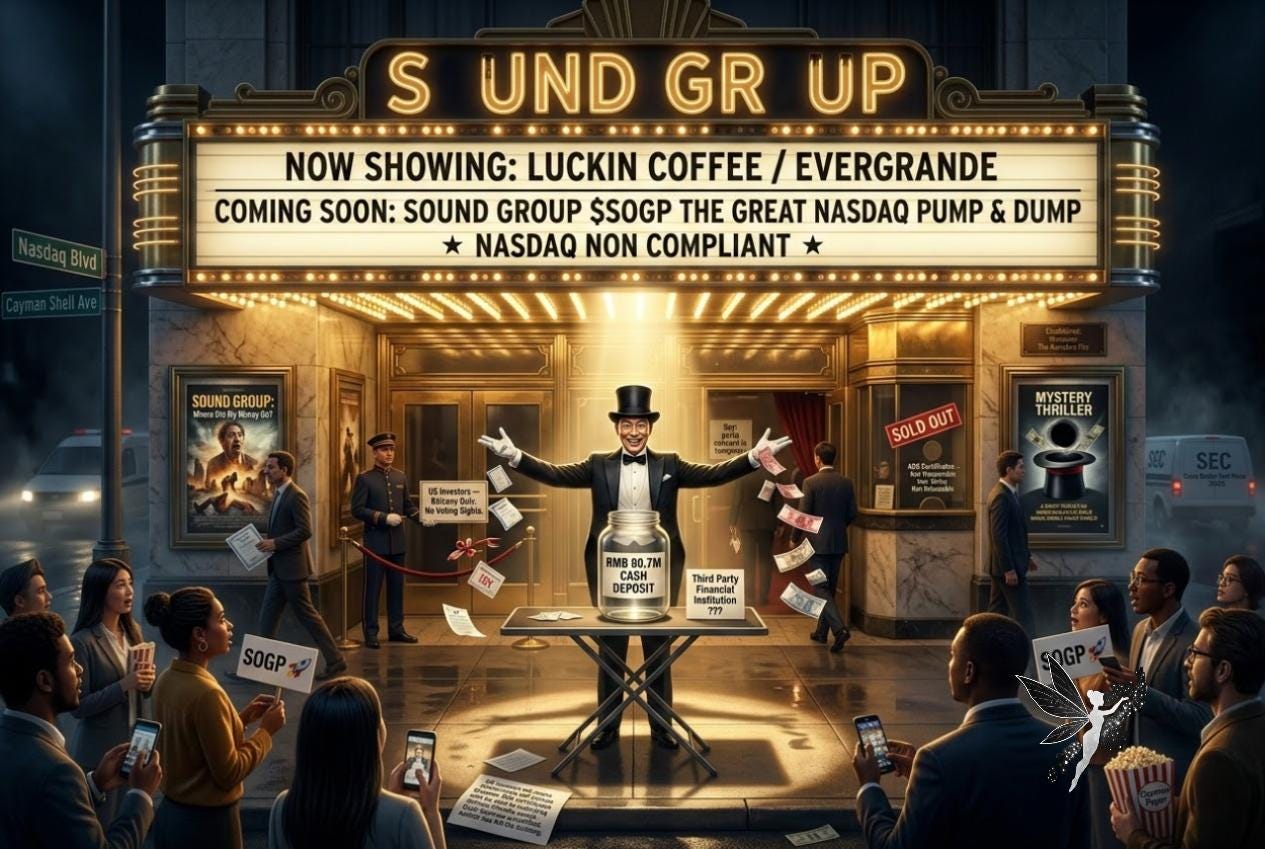

Sound Group $SOGP: Cash Holes and Control Games

Playbook Chinese Nasdaq stock manipulation

Sound Group Inc. (Nasdaq: SOGP) pitches itself as a “next-gen audio social platform” where users buy virtual gifts for hosts and podcasters. The glossy story is about engagement, community, and growth. The reality is about vanishing cash, insider enrichment, and a structure designed to trap U.S. investors.

This report shows how SOGP ticks every box in China’s ADR deception blueprint: unverifiable cash, auditor walkouts, a voting structure that blocks accountability, and a core business already under regulatory siege. Cases like this are textbook examples of how Nasdaq-listed China small caps trap U.S. investors, as documented by independent watchdogs like StopNasdaqChinaFraud.com from Edwin Dorsey, author of the Bear Cave newsletter.

Executive Findings

Cash vanished — RMB 90.7m (~US$12.8m) “deposit” fully written off, no recovery progress. The stock’s initial run-up was fueled by unaudited results — a classic ADR red flag where numbers may not be real.

Auditor quit — PwC Zhong Tian resigned in Dec 2024 after disputes on cash confirmations. The company’s earlier stock run-up had been fueled by unaudited results — meaning investors may have been trading on numbers that were never independently verified.

Governance failure — Still no GAAP/SEC-qualified accounting staff years after IPO; insiders retain control via super-voting shares.

Legal illusion — ADS/VIE structure means U.S. investors don’t own China operations, only a Cayman shell.

Revenue fragility — >95% of revenue comes from “virtual gifts,” a model directly targeted by Beijing’s crackdown on tipping.

Bottom line: SOGP is a textbook case where the numbers on paper cannot be trusted without independent verification of cash. The shareholder register is dominated by Chinese insiders and affiliated funds — Jinnan Lai, Ning Ding, Matrix Partners China, and TMT General Partner Ltd. — all of whom retain effective control. U.S. investors, by contrast, are left with Cayman ADRs that carry no real influence. Combined with a business model already under regulatory siege, this leaves outside shareholders holding the riskiest piece of the structure.

1. Vanishing Cash — The Hole That Can’t Be Plugged

In 2024, Sound Group disclosed a RMB 90.7 million deposit at a so-called “third-party financial institution” that could not be confirmed or recovered. Management had to book the entire sum as a loss.

When a Big Four auditor can’t verify the cash, the story usually ends the same way. PwC Zhong Tian — one of the last anchors of credibility — resigned in December 2024, explicitly citing issues with cash recoverability. They were replaced by a much smaller local firm. Big Four exits don’t happen casually; they happen when a hole in the balance sheet is too large to sign off.

The truth is that Sound Group’s first stock spike was driven by unaudited results. Investors were trading on numbers that had never been independently verified — the exact setup that allows “cooked books” schemes to thrive.

2. Weak Controls, Strong Insiders

SOGP admits in its SEC filings that it lacks sufficient accounting staff qualified under U.S. GAAP and SEC rules, five years after listing on Nasdaq. That is not a mistake; it’s a choice. A company with hundreds of millions in revenue can hire competent controllers overnight. The fact that they haven’t suggests insiders prefer opacity.

Meanwhile, insiders hold Class B super-voting shares with 10 votes each, while ordinary U.S. investors hold Class A shares with just 1 vote. Translation: insiders can outvote every outside shareholder combined, regardless of the number of shares outstanding.

That’s not fair governance. That’s entrenchment.

3. The ADS and VIE Mirage

What do U.S. investors really own? Not the Chinese business. Not the licenses. Not the data.

They own American Depositary Shares (ADS) issued by Deutsche Bank, which represent shares in a Cayman Islands shell. The actual Chinese business is controlled through Variable Interest Entity (VIE) contracts — legal agreements that give Cayman entities “control” on paper, not ownership. In practice, these ADS behave less like real equity and more like tokens — certificates that only hold value as long as Beijing tolerates the structure.

If Beijing decides tomorrow that these contracts are invalid — a risk regulators have repeatedly flagged — Sound Group’s entire structure collapses. ADS investors would be left holding Cayman paper with no claim to the underlying Chinese entities.

This is not a tail risk. It’s a loaded trap waiting for shareholders.

4. Virtual Gifts — Easy Money or Laundering Pipe?

Sound Group’s entire model relies on virtual gifts: users buy digital tokens with cash, then send them to hosts in live rooms. On paper, the company books this as revenue, then shares a portion with hosts and guilds.

But the system is ripe for abuse. Chinese regulators have long flagged virtual gifting as a channel for money laundering, tax evasion, and illicit payouts. That’s why Beijing has been tightening rules since 2021 — capping tips, forcing platforms to disclose real identities, and scrutinizing live-streaming flows.

When over 95% of revenue comes from this one activity, and that activity is under direct regulatory attack, the model isn’t just risky — it’s existentially fragile.

5. Connecting the Dots

Individually, each issue might look like bad luck or growing pains. Together, they form a pattern we’ve seen before in China ADR collapses:

Cash hole → RMB 90.7m deposit disappears, auditor walks.

Insider entrenchment → Class B shares ensure no accountability.

Governance vacuum → still no GAAP-qualified staff post-IPO.

Legal mirage → Cayman ADS + VIE trap.

Revenue fragility → tipping crackdown hits >95% of sales.

This isn’t a “what if.” It’s a system designed to enrich insiders while leaving outsiders exposed. And U.S. regulators are finally waking up to this playbook. In September 2025, the SEC announced the formation of a Cross-Border Task Force to Combat Fraud SEC Press Release, explicitly targeting foreign small-cap ADRs, their auditors, and underwriters involved in “pump-and-dump” and “ramp-and-dump” schemes.

SOGP checks every box of the type of structure this task force was created to dismantle.

Independent watchdogs are making the same point. Edwin Dorsey of The Bear Cave warned in a recent Investors Underground podcast:

“We’ve seen for 10 years plus Chinese companies list on U.S. exchanges and mislead investors… The endgame is they own a lot of stock, the scammers. They dump it on retail investors. And then out of the blue, we see these stocks collapse 90% in a day.”【Transcript, Exposing Scams That Steal Billions with Edwin Dorsey of The Bear Cave, Sept 2025】

Sound Group’s setup — unverifiable cash, insider-dominated governance, and Cayman/ADS scaffolding — is precisely the pattern Dorsey describes.

6. Why It Matters

For U.S. investors, this isn’t just another risky small-cap. It’s a case study in how China's ADRs implode:

The numbers on paper can’t be trusted.

The legal structure doesn’t protect shareholders.

The business model depends on a revenue stream that regulators are actively shutting down.

Without independent proof of cash, without a fix to governance, and without regulatory relief, SOGP is a ticking time bomb.

Global branding with limited reach

Sound Group promotes itself as a “global audio-centric social and entertainment company” and highlights its mission to build “the world’s largest audio platform.” Yet, actual operations remain concentrated in China, with few real-world footprints outside it beyond the administrative base in Singapore and efforts via Tiya (mobile app).

7. Deep Credibility Issues

Sound Group has not addressed several fundamental problems:

No independent bank confirmations of cash and deposits have been published.

No transparent update has been provided on the RMB 90.7m recovery process.

No evidence of a qualified U.S. GAAP/SEC accounting team being hired or certified.

No demonstration of compliance with Beijing’s tipping and content rules.

SOGP’s story isn’t “growth.” It’s control games and vanishing cash.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions—long, short, or otherwise—in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.