SDOT: The Monkey Branching Playbook- Raise Money, Change the Story, Sell Nothing, Repeat

$132.2 million in revenue became $0.0 million in a single year, increasing debt and leading to loan defaults; management responded by selling its last trading subsidiary for $1,000.

Executive Summary

Sadot Group (SDOT) has spent two years shedding every business it has ever operated. It first began as a restaurant company, pivoted into agricultural commodity trading under the “Sadot Agri-Foods” banner, and today it’s neither. During the first quarter of 2026, the commodity operation that generated $132.2 million in the prior-year quarter reported no revenue ($0.0 million). The restaurant brands were sold to Marv Brands in December 2025; the Zambia farm was lost to a court judgment in the same month; and, on a new series of developments, on June 26, 2026, the company sold its Latin America trading subsidiary, Sadot Latam LLC, for $1,000 in cash. (less than a monthly rent for an apartment in the Houston Metro area) As of today, there is no longer an operating business generating revenue.

However, what remains is a financial hole: total liabilities of $60.8 million are offset by total assets of $2.4 million, resulting in a shareholders’ deficit of $58.4 million. Unrestricted cash is roughly $409,000, while some of their notes payable are in default at stated rates of up to 46% (practically loan-shark levels). The company incurred approximately $93.5 million in losses in FY2025 and has an accumulated deficit of $181.5 million. This is not a liquidity problem to be fixed; in reality, it is already a balance sheet insolvency, even as management discloses substantial doubt about the company’s ability to continue as a going concern.

Into that hole, management is stacking narrative. Within weeks of selling the last real business for $1,000, Sadot “acquired” a UAE software shell, Anira Consulting FZC and its “TradeOS” commodity trading platform, for $12 million, which is 97% non-cash paper, then took a six-month option on a $125.5 million California residential real-estate portfolio paid for in stock–which to exercise, would require cash or new Series C preferred stock. Neither counterparty has filed audited financials, raising serious questions about the viability of both projects. At the end of the day, SDOT is a Nasdaq-listed shell being recycled through serial pivots, while common holders are diluted by an authorized-share expansion from 2 million to 250 million and a cumulative 1-to-2,000 reverse-split sequence. Now, it leaves common equity as a residual claim, standing behind $60.8 million in liabilities and $2.4 million in assets; for this reason, Fugazi Research considers SDOT shares completely uninvestable and of ZERO fundamental value.

The make-or-break moment will occur on August 13th, when Q2 2026 earnings will be released. With so little cash at the end of Q1 and a “going concern” warning, investors will gain greater clarity on the very low odds of Sadot surviving such high-risk pivots.

Fugazi Research Analysis

In the quarter ended March 31, 2026, Sadot reported $0.0 USD in commodity sales, down from $132.2 million in the same quarter a year earlier. The entire agri-commodity trading operation that defined the company’s equity story generated no revenue.

Sadot is insolvent, not merely illiquid, as total liabilities of $60.8 million rest on total assets of $2.4 million, yielding a shareholders’ deficit of $58.4 million, a working capital deficit of $57.8 million, and, on top of that, Management discloses substantial doubt about its ability to continue as a going concern.

On June 26, 2026, the company sold 100% of Sadot Latam LLC (its Latin America trading subsidiary) to a buyer in Costa Rica for $1,000 in cash, plus a 27.5% share of receivables it does not expect to collect. With quarterly revenue already at zero, that $1,000 is the cleanest available mark on what the trading business is actually worth.

The restaurant brands (Muscle Maker Grill, Pokémoto) were sold to Marv Brands for $2.9 million in December 2025, and the Zambia farm (once the centerpiece of the agri-foods narrative) was lost to a court judgment the same month and written down by $11.8 million. Management has been liquidating the operating company piece by piece.

Notes payable of $11.1 million are current and largely in default; the most mature is due on December 31, 2025, and was subsequently extended to June 4, 2026, in exchange for an additional 25% original-issue discount applied to the principal. Stated interest rates range from 3.75% to 46.00%

Sadot has executed three reverse stock splits in nineteen months, 10 to 1 (October 2024), 10 to 1 (September 2025), and 20 to 1 (May 27, 2026), which amounts to a cumulative 2,000 to 1, each explicitly to hold the $1.00 Nasdaq minimum bid. In April 2026, authorized shares were simultaneously raised from 2 million to 250 million, restoring the capacity to dilute that the splits had just removed.

The company’s financing facility is engineered to convert into selling pressure. The Helena equity line permits sales of up to $10 million of stock at 97% of the lowest daily VWAP over the pricing period, with further downward adjustments for intraday volatility and cash-payable liquidated-damages triggers.

The headline $12 million Anira acquisition is 97% non-cash paper that was stripped of convertibility within six days. Structured on June 2, 2026, as $405,000 of common plus $6.595 million of Series B preferred and a $5 million note (originally convertible at $3.00) the preferred and note were re-cut by June 8, 2026, as non-convertible and non-voting, with the note bearing zero interest and maturing in 2028.

Management valued its own common stock at two incompatible prices in the same week. The Anira consideration priced SDOT shares at $3.00 on June 2, 2026; four business days later, the real-estate option fee was settled in shares struck at a $7.85 five-day VWAP. The Anira seller’s common tranche was therefore marked at roughly 38% of the VWAP the company itself applied days later, rendering the disclosed $12 million and $1.04 million consideration figures unreliable on their face. The option-fee tranche was sized to exactly 17.71% of shares outstanding, deliberately below the 19.99% threshold that would have required a shareholder vote.

Nasdaq has issued a stack of non-compliance notices over the trailing year: a late Form 10-K notice dated April 17, 2026; a failure to hold an annual meeting; and preferred-stock voting rights, all of which are layered on top of the recurring $1.00 minimum-bid deficiency that the reverse splits are intended to remedy.

Fugazi Research considers SDOT uninvestable at any price above ZERO.

SDOT Financial Summary

Total liabilities of $60.8 million rest on total assets of $2.4 million. On a coverage basis, existing assets fund just 3.9% of obligations, meaning liabilities exceed assets by more than 25-to-1, and every dollar of book liability is backed by roughly 4 cents of book assets. Put differently, a meaningless price-to-book value of this stock (as of the April 2026 quarterly earnings) is -$5.16 compared to its after-hours price on Thursday of $52.34 a share, a massive value disconnect.

Total shareholders’ deficit was $58.4 million as of March 31, 2026, widening from $54.8 million at year-end 2025. Before the non-controlling interest, the deficit attributable to Sadot itself is $61.1 million, so the common equity carries a negative book value of $58 to $61 million.

Current liabilities of $60.1 million are offset by current assets of $2.4 million, resulting in a working-capital deficit of $57.8 million and a current ratio of 0.04 (four cents of current assets for every dollar of near-term obligations). No solvent operating company runs at this ratio; it is a liquidation-stage balance sheet.

Cash totaled $679k, of which $270k is court-restricted, leaving approximately $409k of unrestricted cash. Measured against $60.1 million of current liabilities, unrestricted cash covers roughly 0.7% of what the company owes within twelve months.

The net loss was $4.87 million in Q1 2026. For full-year 2025, the accumulated deficit widened from $83.2 million to $176.6 million, meaning the company lost approximately $93.5 million in a single fiscal year (a loss larger than its current revenue base).

Accumulated deficit reached $181.5 million as of March 31, 2026, against a par-and-paid-in capital base that has been repeatedly raised and diluted since the restaurant era. The company has consumed all this invested capital and returned a balance sheet with negative equity.

Notes payable of $11.1 million are entirely current and largely in default, carrying stated interest rates ranging from 3.75% to 46.00%. Most matured on December 31, 2025, and were extended to June 4, 2026 only after the company agreed to stack an additional 25% original-issue discount onto principal, the company is borrowing at rates reaching 46% while holding $409k in unrestricted cash.

Impairments in FY2025 totaled approximately $31.0 million, including $11.8 million written off on the Zambia farm and $13.4 million on carbon credit assets. Roughly $31 million of previously capitalized asset value was written off in a single year, most of it tied to the “agri foods” narrative that has since been abandoned.

Accounts payable and accrued liabilities of $49.0 million include approximately $25.7 million of commodities payable and $13.8 million of accrued litigation. The company owes $13.8 million on legal exposure alone, more than 33 times its unrestricted cash, while defending claims including the Lombard Trading and factoring disputes.

Shares outstanding rose from 522,514 (December 2024) to approximately 14.8 million by May 2026, before the 20-to-1 reverse split compressed the count back to roughly 744,000. In April 2026, in the middle of this sequence, authorized shares were expanded from 2 million to 250 million (a 125-fold increase in dilution capacity granted just weeks before new issuance resumed).

The company has executed three reverse stock splits in nineteen months: 10-to-1 (October 2024), 10-to-1 (September 2025), and 20-to-1 (May 2026), for a cumulative 2000-to-1 reverse-split ratio.

In the same weeks, it disposed of Sadot Latam for $1,000 in cash; the company booked a stated $12 million Anira acquisition, comprising $405k of common stock, $6.6 million of non-convertible preferred, and a $5 million zero-interest non-convertible note. A $12 million acquisition and a $1,000 divestiture were recorded within the same three-week window, a contradiction in internal valuations that makes no financial sense.

Source: Sadot Group Inc. Form 10-K, fiscal year ended December 31, 2025.

Source: Sadot Group Inc. Form 10-Q, quarterly period ended March 31, 2026.

Source: Sadot Group Inc. Form 8-K, Anira Consulting FZC acquisition, event dated June 2, 2026. Filed June 3, 2026.

Source: Sadot Group Inc. Form 8-K, Amendment to Anira Share Purchase Agreement and Series B Certificate of Amendment, event dated June 8, 2026. Filed June 10, 2026.

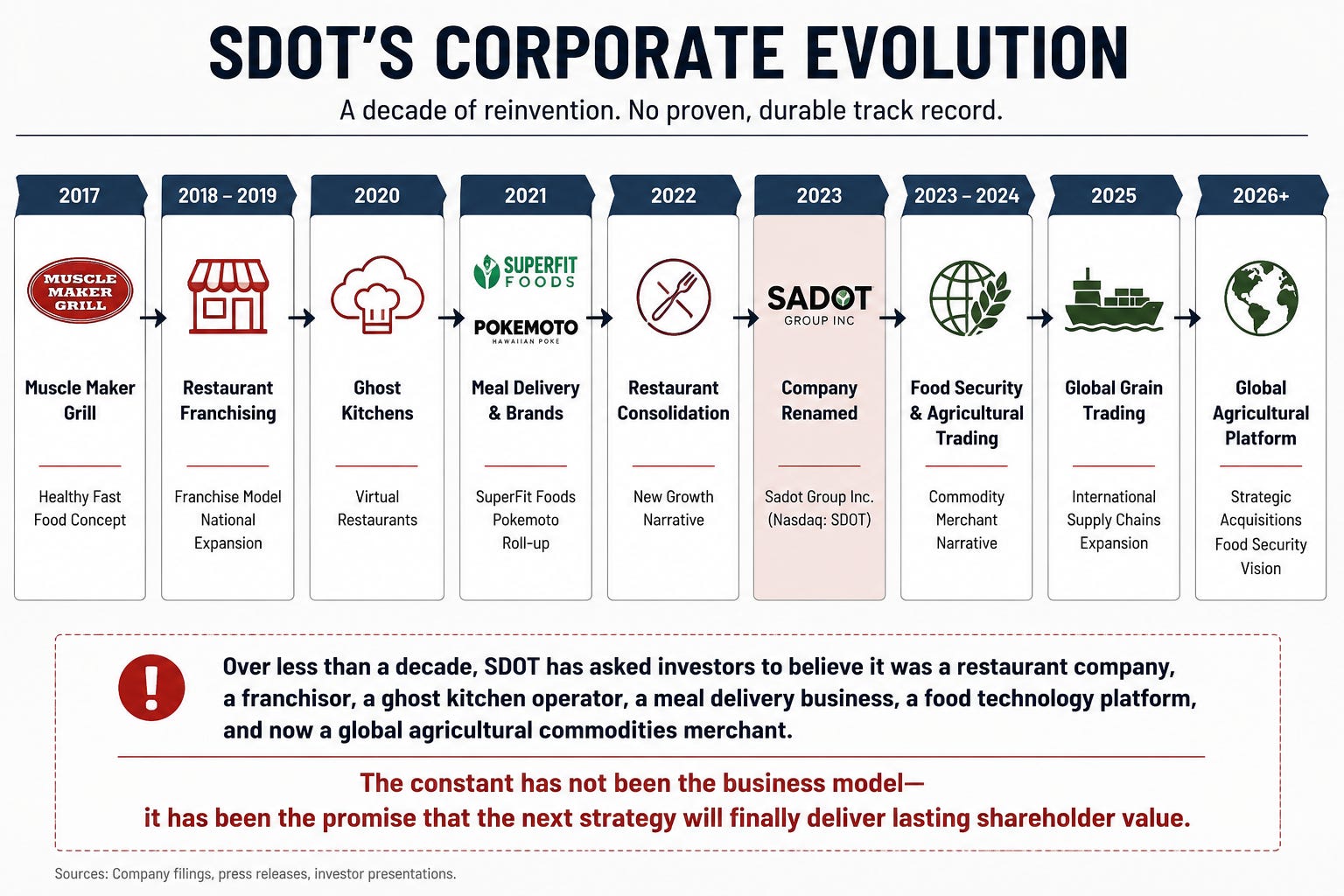

The Ever-Changing Business

Sadot Group has been three different companies in six years and is currently none of them; it was listed as Muscle Maker, Inc., a chain of fast-casual burger and wellness restaurants (Muscle Maker Grill, Pokémoto, SuperFit Foods). In 2022, it discovered that grilling chicken did not move a stock price, formed Sadot LLC, and reinvented itself overnight as a global agri commodity trading house, adopting the Sadot Group name and positioning itself in investor materials alongside ADM, Bunge, Cargill, and Louis Dreyfus.

However, by 2025, it had begun dismantling that identity too. Nowadays, with zero revenue and a $58.4 million shareholders’ deficit, management is mid-pivot into two more unrelated businesses at once: a United Arab Emirates commodity-trading software platform and a portfolio of California apartment buildings.

The agri commodity chapter is important because it demonstrates how little the “revenue” ever really meant. Physical commodity trading has enormous gross turnover against very thin margins, as a trader can run $100 million of grain through its books and keep only a fraction of a percent. In the case of Sadot, which generated $132.2 million of commodity sales in Q1 2025 and still lost money, then watched that line fall to $0.0 million in Q1 2026. The business that supposedly justified the equity story never generated value, while the accumulated deficit ballooned to $181.5 million.

The table shows a company that terminated its foreign management partner, sold its restaurants for less than a single quarter’s former overhead, wrote off its flagship farm, stopped generating revenue entirely, and then (in the same three-week window) booked a $12 million acquisition and a $1,000 divestiture. Management assigned a value to an unaudited UAE software shell company that was 12,000 times what it accepted for its own operating subsidiary days later. This is the recognizable terminal behavior of a reverse-merger vehicle. When the operating business is gone, but the listing still has value, the listing becomes erratic, but at the same time, the final product is a clean Nasdaq ticker into which new stories, new offshore counterparties, and new paper can be injected to sustain a tradeable price. The next investor buying SDOT is not buying a commodity trader, a software company, or a landlord. They are buying whatever management decides to announce next, on a balance sheet that already owes $60.8 million it cannot pay.

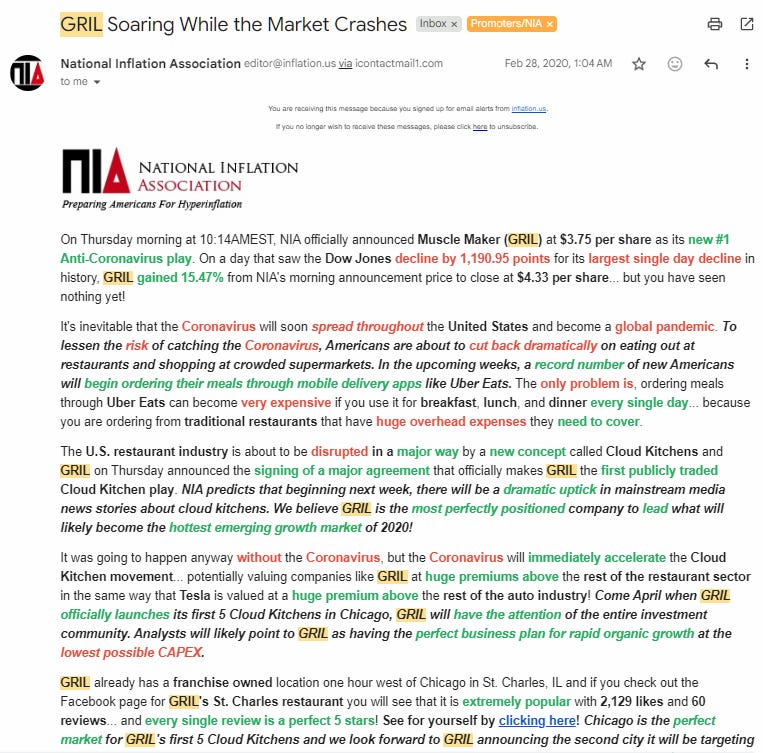

Paid Promotion History under former Ticker GRIL

For years, GRIL/SDOT relied on a paid investor-promotion ecosystem that included sponsored research, compensated financial media, investor conferences, and an unusually high volume of promotional press releases. As the underlying business changed (from restaurants to commodity trading to software and real estate), the promotional machinery remained remarkably consistent.

On July 27, 2023, the Nasdaq ticker GRIL was replaced by SDOT. GRIL was Muscle Maker Grill, which was then owned by Sadot LLC, and was sold for just over $4 million, becoming Sadot Group (SDOT). GRIL had a history of paid stock promotions and, at one point, was even tied to Jonathan Lebed’s stock-promotion company, the “National Inflation Association.” It is important to note that Jonathan Lebed, at age 15, made financial history as the first minor charged with stock market fraud by the U.S. Securities and Exchange Commission (SEC)

Above: Jonathan Lebed: Stock Manipulator, S.E.C. Nemesis -- and 15

Above: GRIL history of paid promotional stock campaigns by Jonathan Labed’s National Inflation Association

The $1,000 Liquidation

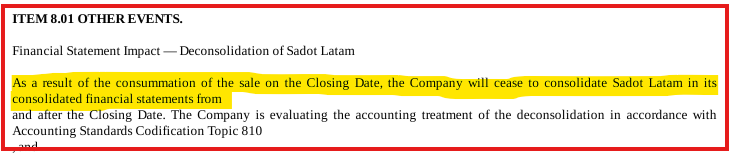

On June 26, 2026, Sadot Group sold 100% of Sadot Latam LLC, the operating subsidiary that anchored what remained of its Latin American commodity-trading business, for just $1,000. Not one thousand shares or one thousand in some other stated value, but one thousand USD, payable by wire transfer, basically giving the company away for free. The telephone number on Sadot’s own Form 8-K carries an 832 Houston, which is a Texas area code. In that area, $1,000 is roughly a month’s rent for an ordinary small apartment. Basically, Sadot’s board convened, negotiated, and executed a definitive Share Purchase Agreement to convey an entire operating company for the price of a small one-bedroom’s rent in Houston until the end of July.

Above: Sadot’s (Sadot Latam LLC) sale for the absurd amount of $ 1,000 USD in cash.

Above: For comparison, monthly rent for a random condo in Houston, TX.

The absurdity deepens when you read what was inside the box. Appendix A to the SPA lists the assets transferred to the buyer, and the first line item is a Citizens Bank deposit of approximately $250,000. Sadot handed over a subsidiary containing a quarter million dollars in disclosed cash, plus a portfolio of receivables and litigation claims, and accepted just $1,000 for it. The buyer paid a minuscule $1 dollar for every $250 of cash sitting in the entity’s own bank account, this is either a gift or a liability shedding maneuver disguised as a sale, as Sadot was not selling an asset; but paying a counterparty to absorb a legal and financial problem, and the $1,000 exists only to satisfy the technical requirement that a sale have consideration.

The genuine purpose is disclosed one item down in the filing: deconsolidation. Under ASC 810, once Sadot ceases to control Sadot Latam, the subsidiary’s liabilities are removed from Sadot’s consolidated balance sheet. The company did not raise $1,000.

The bottom line is that this stock is running on fumes. It’s a company that is out of cash, deeply indebted, has no operations that could raise cash, hasn’t posted any of its quarterly reports on its website since April 2025, and is rotating out Directors and executives to present some level of activity, and now its 20 to 1 reverse stock split is likely only being executed so the main shareholders can find the next story to milk retail investors out of their hard earned cash.

Zero Revenue Is Not a Typo

Companies report a lot of ugly numbers. They rarely report this one. In the quarter ended March 31, 2026, Sadot Group generated $0.0 million in revenue. Not “revenue declined.” Not “revenue missed.” Zero. In the same quarter one year earlier, the same business line, a physical commodity trading under Sadot Agri-Foods, recorded $132.2 million in sales. A company does not travel from $132.2 million to nothing in twelve months by losing customers or missing a season. It gets there by ceasing to have a business, which is precisely what happened.

It is worth being clear about what that $132.2 million was, because its disappearance and its existence are equally damning. Commodity trading books enormous gross turnover against margins measured in fractions of a percent, in which a trader can push a hundred million dollars of grain across its ledgers and keep almost none of it. Sadot ran nine figures of revenue through that model and still lost money every year it operated. So the collapse to zero did not destroy a profit engine; there was never a profit engine to destroy. It removed the appearance of scale, the single large number that let a going-concern shell describe itself in the same paragraph as ADM, Bunge, Cargill, and Louis Dreyfus. Strip the turnover, and what is left is the economic reality that was always underneath it: a company that consumed capital to move other people’s commodities and kept nothing for the trouble.

For a going concern, that zero is fatal in a way the market has not priced. A company with $409,000 of unrestricted cash and $60.1 million of current liabilities survives only on its ability to generate cash internally or raise it externally. Internal generation is now definitionally impossible: you cannot fund operations from operations that produce no revenue. That leaves external capital as the sole source of survival, which is exactly why the 250-million-share authorization and the Helena equity line matter, and exactly why they exist. The zero on the revenue line and the dilution machinery are the same fact stated twice. One explains the other. A business that earns nothing must sell stock to breathe, and a business that must sell stock to breathe will keep selling it until there is nothing left to sell.

Conclusion

Sadot Group would like investors to believe it is a commodity trading company. Depending on which week’s press release you read, it would also like you to believe it is a UAE software company, a California real estate investor, and, for old times’ sake, a chain of health-conscious burger restaurants. Today, it is effectively none of these.

Instead, Sadot is a Nasdaq-listed company with a Texas mailing address, a going concern warning, and $60.8 million in liabilities supported by just $2.4 million in mostly reserved or restricted assets. Revenue has fallen to $0.0 million, down from $132.2 million one year earlier. Shareholders’ equity stands at-$58.4 million. The current ratio is 0.04, a figure so far below 1 that it no longer measures liquidity and instead reflects a balance sheet in severe financial distress. Some of the debt carries stated interest rates as high as 46% and was extended beyond its December default only after the company agreed to increase the original issue discount by an additional 25%.

The transaction that best illustrates the company’s trajectory unfolded over a three-week period in June. Management sold Sadot Latam, the last operating business it actually built, for just $1,000. The subsidiary left with approximately $250,000 of disclosed bank cash and the litigation associated with its operations. Within weeks, Sadot announced the $12 million acquisition of Anira Consulting FZC, an unaudited software company based in Sharjah. The consideration consisted almost entirely of preferred stock and a non-interest-bearing, non-convertible promissory note, a structure that raises obvious questions about how management arrived at a $12 million valuation. In other words, management accepted $1,000 for the operating business it knew best while assigning a $12 million valuation to one it neither audited nor built. The company has offered investors little basis for reconciling those dramatically different valuations.

Meanwhile, in April, just weeks before the reverse split reset the outstanding share count, the board quietly expanded the company’s authorized common stock from 2 million shares to 250 million (a 125-fold increase) in future dilution capacity. No company with $409,000 of unrestricted cash and a viable self-funded operating business would ordinarily require that level of issuance capacity. The reverse split compresses the share count to preserve the Nasdaq listing; the expanded authorization refills the barrel. The businesses are disposable. The dilution capacity remains.

Viewed through a traditional liquidation framework, the math is difficult to ignore. $2.4 million of low-quality assets would not travel far up a capital structure burdened by $60.8 million of liabilities before being exhausted, leaving common shareholders at the very end of the line, not so much with a claim as with a hope.

Perhaps the most revealing datapoint is that the only observable arm’s-length price the company has assigned to one of its own operating businesses was $1,000, which is the amount paid for everything that remained of Sadot Latam. The market continues to value the common stock far above that implied assessment, but investors should consider whether the company’s own transactions tell a more reliable story than its promotional narrative.

Sadot Group increasingly resembles a company that has outlived its operating businesses while attempting to preserve its public listing through successive strategic pivots. The stories will likely continue because, for a company in this position, the only thing worse than another implausible acquisition is the silence that precedes a delisting. Based on the company’s balance sheet, capital structure, and recent transactions, Fugazi Research believes SDOT common stock has no meaningful fundamental value and is unsuitable for investment.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions-long, short, or otherwise-in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.