RDW: Selling Space Fantasies. Printing Shares.

Redwire is selling investors exciting space fantasies, but its filings tell a different story: Redwire’s business spans defense drones, space infrastructure, ATM reloads and even growing strawberries

Executive Summary

Redwire (RDW) has become one of Wall Street’s most compelling space and defense stories. The company operates in attractive markets (orbital infrastructure, defense technology, autonomous systems, and national security) and its contracts, products, and customers are real. That narrative has helped drive significant investor enthusiasm. Our concern is not with the industries Redwire serves, but with how the business has been financed and operated.

Since late 2025, Redwire has relied heavily on the equity markets to fund its operations, authorizing more than $1.1 billion of at-the-market (”ATM”) equity issuance while common shares outstanding have nearly tripled in roughly fifteen months. Operating cash flow remains negative, and recent increases in cash have been driven by equity issuance rather than internally generated cash flow.

At the same time, the company’s governance and financial reporting raise additional concerns. KPMG issued an adverse opinion on Redwire’s internal control over financial reporting for fiscal 2025, concluding that the company did not maintain effective internal controls. The acquisition of Edge Autonomy (which represented approximately one-third of Redwire’s 2025 revenue) was excluded from that assessment because of acquisition timing, leaving investors with limited assurance over a significant portion of the business.

Redwire’s operating history also raises questions about execution. Revenue has expanded primarily through acquisitions, but profitability has remained elusive. The company has never generated sustained positive free cash flow under its current structure, accumulated deficits continue to grow, and shareholder dilution has become an increasingly important source of liquidity.

This report examines three central issues. First, whether Redwire’s operating business is capable of funding itself without continued reliance on equity issuance. Second, how the Edge Autonomy acquisition reshaped the company’s capital structure and created significant additional share supply. Third, whether Redwire’s governance, financial controls, and board oversight are adequate given the company’s operating and financing history.

Based on our review of SEC filings, court records, audit reports, and other publicly available information, we believe the market is placing a premium valuation on a business whose underlying economics and governance profile do not justify that premium. In our opinion, Redwire’s equity remains materially overvalued relative to the risks disclosed in its own public filings.

Fugazi Research Analysis

Redwire is an integrated space and defense company that has failed to demonstrate a viability on either business. The space segment swung from $3.2 million in operating income in Q1 2025 to a -$4 million operating loss in Q1 2026 on flat revenue, while the Defense Tech segment generated a -$46.9 million operating loss in its first quarter.

Redwire entered its first ATM facility in November 2025 for $250 million through four institutional agents; it was effectively exhausted in only five months. On May 6, 2026, management replaced it with a $350 million facility, and on June 9, 2026, management terminated it and entered a third ATM for $500 million through ten agents, making a total of $1.1 billion authorized ATM capacity across all three tranches since November 2025.

Operating cash flow in Q1 2026 was negative $6.7 million, Investing activities consumed an additional $6 million. The company’s $50 million cash increase for the quarter was sourced entirely from $63.5 million in net ATM equity proceeds.

Common shares outstanding went from 67 Million on December 31, 2024 to almost 200 Million on March 31, 2026, representing a staggering 197% share count increase in 15 months with no floor in sight, as an additional 16,079,001 shares sit in the convertible preferred stack convertible at $3.05 (more than 60% below the current stock price). At the Q1 2026 weighted average ATM sale price of $9.38, fully deploying the current $500 million facility requires the issuance of approximately 53.3 million additional shares, which would represent a further 27% dilution on shares already outstanding.

Management backed out of $46.7 million in equity compensation, $11.3 million in D&A, $2.9 million in debt costs, $2.0 million in capital market advisory fees, and $0.4 million in litigation expenses. Adjusted EBITDA remained negative at -$9.2 million , meaning that the business generates negative economic value before it finances itself.

A derivative lawsuit filed in 2022 settled in 2025 for zero monetary recovery. The complaint alleged defendants failed to maintain adequate internal controls and issued materially false or misleading statements. Defendant insurers paid $912,500 in attorneys’ fees, while the individual defendants (CEO Peter Cannito and seven board members) deny all allegations and admit no liability.

The settlement extracted nonexistent governance structures that should have existed at the SPAC closing in 2021. Settlement required the company to create a risk Committee, a Disclosure Committee, a Chief Compliance Officer position, enhanced audit committee procedures, and a strengthened whistleblower policy.

Fugazi Research considers RDW shares extremely overvalued, of no fundamental value, and purely speculative.

Financial Summary

Common shares outstanding increased from 67,002,370 on December 31, 2024 to 198,918,728 on March 31, 2026, a 197% share count explosion in a period of 15 months.

Three ATM facilities totaling $1.1 billion in authorized capacity have been opened since November 2025, the most recent for $500 million on June 9, 2026. Additional shares sit in the form of convertible preferred stock, which if overall triggered can enable a further 27% dilution on top of shares already outstanding.

Edge Autonomy contributed $36.41 million in revenue and a net loss of -$54.9 million in Q1 2026. This is the asset for which Redwire paid $1.02 billion, recognized $722.99 million in goodwill, and issued 49.8 million shares at $19.08, while the stock price has plummeted 55% since share issuance.

Redwire reported a net loss of -$76.5 million in Q1 2026, after stripping $46.7 million in equity compensation, $11.3 million in D&A, $2.9 million in debt costs, $2.0 million in capital market advisory fees, and $0.4 million in litigation expenses, Adjusted EBITDA remained negative at -$9.2 million.

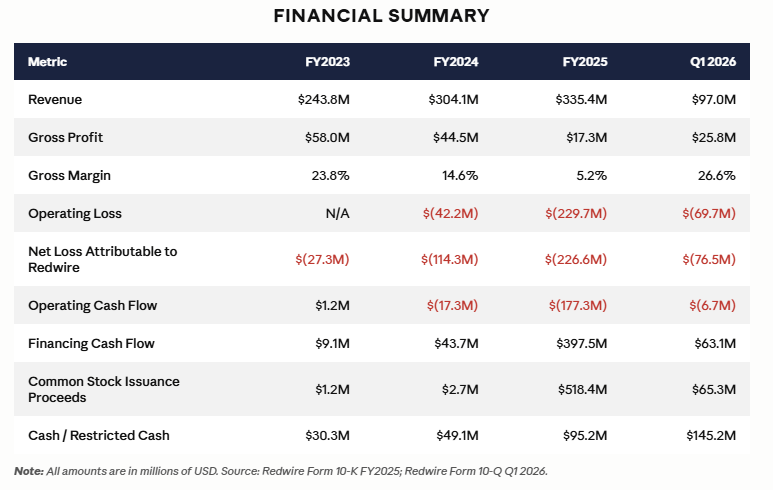

True free cash flow in Q1 2026 was negative -$12.7 million. Annualized, this implies a burn rate of approximately $51 million per year, against a cash balance that was itself funded entirely by $63.5 million in ATM equity proceeds in the same quarter.

The accumulated deficit of $698.3 million as of March 31, 2026 represents 188% of last 12 months of revenue of $370.96 million, meaning the company has destroyed nearly two full years of its own revenue base in cumulative losses since inception. The deficit increased $76.5 million in Q1 2026 alone, $149.5 million in the trailing twelve months, and is on pace to cross $900 million before December 31, 2026.

Last twelve months revenue of $370.96 million per the book-to-bill KPI table implies a current revenue multiple of 4.6× at $8.50 per share. Considering the fact that this business has negative Adjusted EBITDA, unresolved material weaknesses across every operating unit, and 197% share count dilution in 15 months.

Source: Redwire Corporation Form 10-Q, Period Ended March 31, 2026.

Source: Redwire Corporation Form 8-K, Filed June 9, 2026.

Interview with a Space Industry Expert: Redwire’s Business Structure and Viability

The following statements represent a space expert’s opinion based on their more than two decades of working in the space industry.

Fugazi Research: Redwire often gets highlighted for its growing backlog and the potential for margin expansion in the space and defense sector. But when you step back and look at it as an investment, what’s your actual take on the company? What concerns you most about their business structure and financial viability?

Space Expert: “As an investment, everything is just wrong with Redwire. Going back over several years and listening to their earnings calls and you hear the same script: record backlog, improving margins, operational leverage coming. But that narrative breaks when you look at the important number--profitability. Redwire management burns cash with widening net losses, and maintains EBIT margins at near -77%, one of the worst in the industry. More importantly, their balance sheet is a joke: 776M in goodwill and 326.7M in intangibles, representing 73% of their 1.51B in total assets. Only 410M is tangible—cash, receivables, real property. They’re basically a roll-up that paid massive premiums for acquisitions, and we’re already seeing Edge Autonomy hemorrhage almost 55M in losses. At 73% goodwill, Redwire is in the worst quartile in the defense, even versus aggressive roll-ups that cap out at 60-70%. If revenue growth slows or margins don’t inflect, that balance sheet gets decimated.”

Fugazi Research: “Redwire management often points to their nearly $500 million backlog as proof of strong demand and future growth. How much weight do you actually give that backlog number when evaluating the company? And what’s your view on their repeated delays in reaching profitability?”

Space Expert: “The 498M backlog they keep touting is meaningless if you don’t generate positive unit economics converting it. Management keeps pushing profitability down the road (now to 2028) while diluting shareholders every single year. That’s a bet that aerospace customers will suddenly become profitable for them without the margin improvement trajectory we should already be seeing from a mature company.”

Fugazi Research: Redwire went public in late 2020 around $10 a share and is still trading near that level nearly six years later. What do you see as the main reason the stock has gone nowhere, especially when the broader space sector has real contracts and several profitable players?”

Space Expert: “This company was created in Nov 2020 at 10 dollars a share. Nearly 6 years later, it’s hovering just above 10 dollars a share. The problem isn’t the industry or the customers--space is real, customers are real, contracts are real, and there are several profitable space companies. The problem is that Redwire is continuously issuing stock for survival capital without fixing their business. And it has to be noted that management issued over 46M in equity-based compensation last quarter alone (for what, I’m not sure). The backlog question is masking the dilution question--how many new shares will it take for Redwire to reach profitability, and how much will that cost current shareholders?”

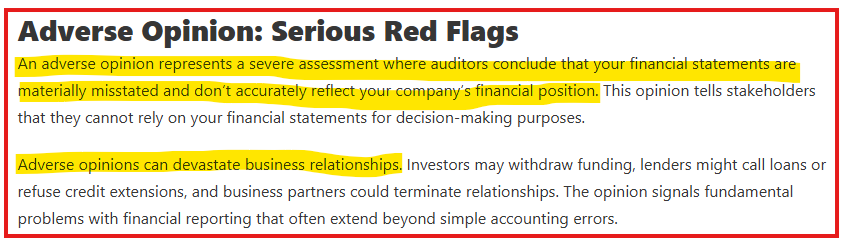

The KPMG Adverse Opinion

KPMG LLP, Redwire’s independent registered public accounting firm, issued an adverse opinion on the effectiveness of Redwire’s internal control over financial reporting as of December 31, 2025 (the most severe of the four conclusions an auditor can render on internal controls). An adverse opinion does not mean controls are weak or need improvement. It means the auditor concluded that Redwire did not maintain effective internal control over financial reporting.

The company has a history of poor financial controls that has led to shareholder lawsuits. Most recently, Redwire’s auditor (KPMG) issued an “adverse opinion” on Redwire’s internal financial controls, the most severe of the four opinions an auditor can provide. This means the company can not provide reliable financial reporting. Importantly, even this audit excluded the acquisition of Edge Autonomy, even though the acquisition occurred mid-year and that it represented one third of Redwire’s revenue for 2025. This same issue is the core of previous shareholder lawsuits, and could represent the basis of future shareholder lawsuits.

The adverse opinion covers material weaknesses across U.S. operations and European operations, the same deficiencies management disclosed as active and unremediated in the Q1 2026 10-Q filed May 7, 2026. KPMG’s conclusion and management’s own disclosures are saying the same thing: this company cannot provide reliable financial reporting, and has not been able to for years.

FY2025 free cash flow was negative -$200.6 million, the company consumed $177.3 million in operating cash against $335.4 million in revenue, a cash consumption rate of 52.8 cents for every dollar of revenue generated. This is the financial performance that KPMG’s adverse opinion was issued against. The control failure is not a disclosure technicality. It is the audit trail of a business that burned through more than half its revenue in cash from operations in a single year.

With likely more than 60% of total backlog coming from US government contracts at a time when the likelihood of another government shutdown is uncomfortably high, Redwire’s already anemic financials will likely face exceptional pressure in the 2nd half of CY2026. Should this occur, Redwire will likely tap its massive ATM .

Source: Redwire Corporation Form 10-Q, Period Ended March 31, 2026. Item 4 — Controls and Procedures.

The Acquisition Was the Exit

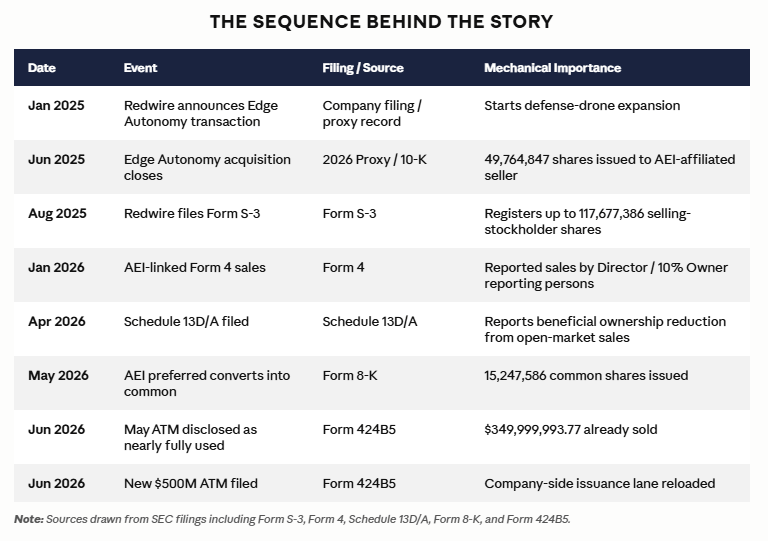

The Edge Autonomy acquisition created two things simultaneously: a defense-drone narrative compelling enough to move retail sentiment, and a stock block (49,764,847 shares issued directly to an AEI-affiliated seller at close). The S-3 followed four months later, registering up to 117,677,386 selling-stockholder shares for resale while the story was still fresh. AEI-linked entities began Form 4 open-market sales in January 2026. By May, the preferred had converted into common (15,247,586 additional shares sold into the market at $13 to $15.80 on a $3.05 conversion cost). Another layer of the original position liquidated into public hands at a 4× to 5× return, while retail investors were buying the space and defense narrative.

Meanwhile, Redwire’s own ATM quietly exhausted $350 million in proceeds and was immediately replaced with a new $500 million facility filed the same day the prior one was terminated. Two parallel tracks running simultaneously: the insider resale lane unwinding the acquisition-era position, and the company ATM funding operations that cannot self-finance.

Source: Redwire Corporation Form S-3, Filed August 7, 2025.

Source: Redwire Corporation Form 424B5, Filed June 9, 2026.

Source: Redwire Corporation Form 4 Filings, AE Red Holdings LLC / Edge Autonomy Ultimate Holdings LP, January–May 2026.

The ATM Playbook

Redwire entered 2025 as a space infrastructure company with chronic negative operating cash flow. The Edge Autonomy acquisition added defense drones and autonomous systems, a stronger narrative than traditional space hardware, and one that commands premium market attention when tied to national security. The acquisition was paid mostly in stock: $160 million in cash and $765 million in common stock, resulting in 49,764,847 shares issued to the AEI-affiliated rollover seller.

The investor rights agreement required Redwire to file a resale registration covering securities held by selling stockholders. The August 2025 Form S-3 registered up to 117,677,386 common shares for selling stockholders and up to 2,000,000 warrants. Redwire would receive none of those proceeds. The company-side lane ran through ATM issuance ($518.4 million in common stock issuance proceeds in FY2025 alone).

As of the release of this report, on June 9, 2026, Redwire filed a new $500 million ATM prospectus and disclosed in the same filing that $350 million had already been sold under the May 2026 equity distribution agreement. The May ATM was terminated the same day the new one was filed. Now shares may be sold indiscriminately, through market makers, in block transactions, and in privately negotiated transactions. Agents collect commissions of up to 3% of gross sales price. Proceeds may be used for working capital, debt repayment, acquisitions, and research and development. At the prospectus’ assumed offering price of $18.57, the full $500 million facility adds 26,925,148 shares, bringing total shares outstanding to 265,750,493. Massively bloating the outstanding shares.

And if history is any guide, a meaningful portion of those proceeds will likely fund the next acquisition. That prospect raises an obvious question. The last acquisition was an AE Industrial Partners portfolio company acquired at a valuation many investors viewed as excessive. Today, Redwire carries approximately $776 million of goodwill on its balance sheet, yet management has not recognized an impairment. Given AE Industrial Partners’ control of the board, its role in appointing the CEO, and its repeated pattern of converting preferred securities and selling into acquisition-driven rallies, investors should ask a simple question: Who is the next acquisition really designed to benefit, Redwire’s common shareholders, or the sponsor that controls the company?

Source: Redwire Corporation Form S-3, Filed August 7, 2025.

Source: Redwire Corporation Form 10-K, Fiscal Year Ended December 31, 2025. Filed February 27, 2026.

Source: Redwire Corporation Form 424B5, Filed June 9, 2026.

The AEI Exit Lane

AEI’s involvement in Redwire appears across multiple SEC filings, including the proxy statement, Form S-3, Form 4, Schedule 13D/A, and Form 8-K. Redwire’s 2026 proxy statement identifies the Edge Autonomy seller as an AEI-affiliated “Rollover Seller,” which received 49,764,847 Redwire shares as part of the deal. In August 2025, Redwire filed a Form S-3 to register shares for sale by existing stockholders. The filing showed that AE Industrial Partners and its affiliates owned 115.2 million shares before the offering and planned to sell 79.5 million shares plus 2 million warrants. After the sale, they would still hold approximately 35.6 million shares. Importantly, Redwire would not receive any proceeds from these sales and the money would go directly to the selling stockholders.

The filings show that AEI-related entities sold a large number of Redwire shares in mid-January 2026. On January 13 and 14, AE Red Holdings and other related parties reported selling a total of approximately 14.3 million shares. After these sales, they still owned 61.5 million shares. In April 2026, they filed an updated Schedule 13D/A, which disclosed further reductions in their ownership through additional open-market sales. Following these transactions, the group’s beneficial ownership stood at 41.5 million shares, or 19.8% of Redwire.

On May 20, 2026, Redwire announced that AEI converted all of its remaining preferred shares into common stock. Specifically, AEI converted 46,505.13 preferred shares into 15,247,586 common shares. After the conversion, no preferred shares remained outstanding. This move effectively completes AEI’s exit from Redwire.

AEI’s ties to Redwire appear in several SEC filings. The 2026 proxy statement shows that the Edge Autonomy seller is an AEI-affiliated party, which received nearly 50 million Redwire shares as part of the deal. In August 2025, Redwire filed a registration statement allowing existing shareholders to sell their shares. AE Industrial Partners and its affiliates planned to sell roughly 79.5 million shares and 2 million warrants. Even after those sales, they would still own about 35.6 million shares. Importantly, Redwire would not receive any proceeds from these sales as the money would go directly to the selling shareholders.

The Space-Strawberry Thesis

On June 4, 2026, three days after Jefferies downgraded the stock, and the same week AEI was selling hundreds of millions of dollars of common stock into the rally, Redwire issued a press release announcing a contract to grow wild strawberries in space. The stock went up 19%. This is the valuation framework Redwire’s investors are operating under.

Growing strawberries in space does not generate revenue. A strawberry grown in orbit is worth exactly as much to a Redwire common shareholder as a strawberry grown in a garden in Jacksonville, Florida… which is to say, nothing.

There is no dollar figure attached to this transaction in any public documents. The most telling detail about Redwire’s so-called “greenhouse partnership” is that the technology was co-developed with Tupperware Brands, a company that filed for Chapter 11 bankruptcy in September 2024. Redwire’s world-first commercial space greenhouse is, in the most technically accurate description possible, a Tupperware container bolted to the International Space Station.

Redwire partnership with Tupperware (TUP, no longer listed on Nasdaq)

The counterparty on this “landmark & breakthrough” commercial announcement is Astrobiome Space, a Luxembourg based startup that makes “super-postbiotics” and proprietary microbial extracts called “Champion Strains.” Astrobiome Space has no disclosed revenue, no disclosed contract history, and no disclosed valuation. Redwire did not disclose the contract value either. The stock price has bled out from roughly $22 to now $11 in just two weeks after that announcement which confirms the bearish assessment of the undisclosed contract details.

At the end of the day, Redwire is a company with $698 million in accumulated deficit, an adverse KPMG opinion, $776 million in goodwill never tested for impairment, a board controlled by a sponsor that converted its preferred at $3.05 and sold into the high 10’s, and a stock that went up 19% the day it announced a no-value contract to grow strawberries in a Tupperware container for a Luxembourg probiotic startup that makes something called Champion Strains. In a sector that runs on pure hype and wishful thinking, this “contract” definitely wins as the most ridiculous type of PR we have come across.

Governance Issues and Class Action Lawsuits

Another concern are shareholder investigations launched by prominent plaintiff firms, including Kaskela Law, Grabar Law, and Robbins LLP, which exposes a pattern of alleged deception and systemic corporate malfeasance at Redwire. The complaints charge Redwire and its senior executives with actively fabricating a narrative of robust governance and integrity while deliberately concealing severe, pervasive breakdowns in the company’s internal control over financial reporting (ICFR). This deceptive campaign culminated between late 2021 and 2022, when management was forced to abruptly postpone earnings, confess to “potential accounting issues” at a subunit, and ultimately admit to even deeper, unaddressed ICFR failures.

The roots of this systemic deception trace back to the company’s pre-merger phase, where firms like Brodsky & Smith and Hagens Berman alleged that Redwire, and its leadership, issued false and misleading statements leading up to and following its September 2021 SPAC merger with Genesis Park Acquisition Corp. To win investor confidence, management allegedly touted a dedication to conducting business with efficiency, fairness, and integrity. In reality, leadership was actively hiding structural flaws in how they tracked revenue, specifically at their business subunit, LoadPath. Legal complaints detailed that LoadPath completely lacked standard internal accounting control procedures, allowing leadership to engage in improper revenue recognition to artificially inflate revenue and present a false image of rapid, robust growth following the public listing.

Despite knowing about these pervasive material weaknesses in their ICFR, executives desperately sought to hide them from the public. Because of these unaddressed control gaps, plaintiff firms asserted that all of management’s positive forward-looking statements regarding Redwire’s operations, business prospects, and integration success completely lacked a reasonable factual basis. According to a Bloomberg Law report, investors successfully advanced a relatively novel legal theory demonstrating that senior leaders willfully fostered a corporate environment where ethical financial standards were disregarded to shield executive interests and keep stock values artificially high. This systematic deception abruptly unraveled on November 10, 2021, when an internal whistleblower report forced management to delay their Q3 earnings. This disclosure, followed by subsequent admissions of further ICFR failures, caused a devastating multi-day stock plunge that destroyed significant shareholder value.

These damning episodes reveal a toxic “tone at the top” and a deceptive disclosure culture, laying bare allegations that senior leadership knowingly masked critical control failures to mislead investors and protect their own interests. Ultimately, these extensive legal battles culminated in Redwire agreeing to pay an 8 million dollar class-action settlement to resolve the claims of hidden accounting irregularities and failed internal controls.

This is material, and a mere four years later, KPMG, one of the most respected auditing firms in the world, issued a scathing opinion of Redwire’s financial controls, which is the core issue that resulted in the earlier litigation issues. As such, the chances of future shareholder legal action is far from zero.

Top Analyst Downgrading concurs with our sentiment

The Jefferies downgrade on June 1st, 2026 is the most useful third party information in this report as it agrees with our thesis. As Jeffries now believes that the stock has run too far to keep going and which has now become a valuation concern.

While the downgrade went from BUY to HOLD, this is rarely a good signal, as it signals investors that the stock has run out of fuel, as it now has no fundamentals, no story behind to run with, and which smart money will now usually get out, while leaving FOMO chasers with heavy losses. The downgrade marked the beginning of the end of the rally which double-topped almost exactly at previous all-time highs at $26 from the 2025 January run. Analyst downgrades in a sector mania such as space, where investors are excited to buy without much discernment is a terrible sign. The stock has been in freefall ever since.

Schwab Thinkorswim Chart showing RDW January 2025, June 2026 double top

This can be corroborated as Multiple Form 144 filings showed that a major holder or RDW insider was preparing to sell restricted shares . As AEI converted the entire stack of preferred shares into more than 15 million of common stock while selling every single share into the open market at prices ranging between $13 to $16.

The Fugazi Verdict

We believe the evidence presented throughout this report points to a company whose governance, incentives, and capital allocation decisions have consistently favored its controlling sponsor over its common shareholders. As long as those incentives remain unchanged, investors should expect the same pattern to continue. The question is not whether another acquisition, another capital raise, or another promotional narrative will emerge. The question is who will ultimately bear the cost when those strategies can no longer sustain the valuation? In our view, that burden is likely to fall on Redwire’s common shareholders.

At the end of the day Redwire is the same company with the broken internal controls that triggered a securities class action in 2021 and which remain unsolved up to date. The same governance failures that were settled for zero monetary recovery that should have been in the first place is the company that now tries to sell new narratives, hype new PR’s all while maintaining a massive deficit. The same sponsor that structured the SPAC, controlled the board, sold the Edge Autonomy acquisition to Redwire at a valuation its own goodwill balance may never justify is the same sponsor that retains board control, nomination rights, and the contractual ability to force a sale process at a time of its own choosing. Now the stock is trading at a very premium multiple to a business that has never generated positive cash flow, has a horrible auditor opinion on its own internal controls, and has funded all of its public existence by pure shareholder dilution. The filings show a company in which no intelligent investor would put his/her hard earned money in, but a pure capital extraction vehicle doomed from the beginning. For this reason Fugazi research considers RDW shares merely speculative and of no fundamental value.

Disclosure

Fugazi Research is an independent financial investigative publisher funded by reader donations, whose mission is to identify and publicly expose corporate fraud and market misconduct. All research contributors are volunteers. The organization is funded exclusively through reader donations and free subscriptions. Fugazi Research does not manage investor capital, does not operate as a hedge fund or trading vehicle, and does not provide personalized investment advice.

All content published by Fugazi Research (including reports, commentary, social media posts, interviews, and any other communication) represents the editorial opinions of its contributors as of the date of publication. Our work is based on publicly available information, independent research, interviews, document review, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change without notice. We do not undertake any obligation to update or revise published content to reflect subsequent events, market developments, or new information, except where factual errors require correction. When we issue corrections, we do so prominently and transparently.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. Our publications should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult qualified financial, legal, and tax advisors before making any investment decision. The publication of research about a company (whether positive or negative) is not a recommendation to trade that company’s securities.

Fugazi Research LLC does not hold positions (long, short, or otherwise) in any securities covered by its publications. The organization does not trade. The organization does not coordinate trading activity among its contributors. No contributor is compensated based on the trading outcomes of any published research.

Individual contributors may independently hold personal positions in securities covered by Fugazi Research publications. Such positions, if any, are the personal decisions of those individuals, are not disclosed to or coordinated with Fugazi Research LLC, and do not influence the editorial decisions or conclusions of our research.

To protect the integrity of our research and the individuals who contribute to it, Fugazi Research maintains the following editorial standard: contributors who author or materially contribute to a report are expected to refrain from establishing, increasing, reducing, or closing any personal position in the covered security beginning when the report enters preparation and ending 48 hours after publication. This standard exists to protect individual contributors from personal legal exposure and to preserve the credibility of Fugazi Research’s editorial independence. It is voluntary and self-enforced. Fugazi Research LLC does not monitor the personal trading accounts of its contributors. Contributors who are uncertain whether a specific situation is covered by this standard should seek independent legal counsel before trading.

Fugazi Research does not accept compensation from any company, individual, or entity in exchange for coverage, positive or negative. We do not publish research at the direction of, or for the financial benefit of, any third party with a trading position in the securities we cover. Reader donations support the operational costs of the publication and do not influence editorial decisions or create any expectation of favorable or unfavorable coverage. If Fugazi Research ever enters into any arrangement that could constitute a conflict of interest with respect to a covered security, that relationship will be disclosed prominently in the relevant publication prior to or at the time of release.

We make every reasonable effort to ensure the accuracy of the information we publish. Our research relies on publicly available documents, regulatory filings, court records, interviews, and independent analysis. We believe the information we present is accurate and reliable as of the date of publication. However, it is provided without any representation or warranty, express or implied, as to accuracy, completeness, or timeliness. Fugazi Research welcomes factual corrections. Companies or individuals who believe a specific factual claim in our research is inaccurate are invited to submit documented corrections for editorial review. We will publish corrections prominently where warranted.

Our research may include forward-looking statements, estimates, projections, price targets, or opinions that involve known and unknown risks, uncertainties, and assumptions. Any price targets or projections set forth in our research reflect our analytical conclusions at the time of publication and are not representations that covered securities will reach such prices. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results.

Reader donations support the costs of publishing independent financial research. Donations do not constitute investment in any fund, trading vehicle, or profit-sharing arrangement. Donors receive no financial return from Fugazi Research’s publications or from any trading activity by any party. Donations are made solely to support the editorial mission of Fugazi Research and carry no expectation of financial benefit of any kind.

By accessing or using Fugazi Research’s materials, you acknowledge that Fugazi Research LLC, its manager, contributors, and affiliates shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk. Nothing in this disclaimer limits any rights or remedies available under applicable law that may not be lawfully disclaimed.

All content published by Fugazi Research is the intellectual property of Fugazi Research LLC and may not be reproduced, distributed, or commercially exploited without prior written consent. Sharing of our research for non-commercial informational purposes is permitted with attribution to Fugazi Research.

This disclaimer is governed by the laws of the United States. Nothing herein modifies or limits any rights or remedies available to the SEC, DOJ, or any other regulatory authority under applicable federal or state securities laws.