$MTC: From Delisting Risk to a Half-Billion-Dollar Fantasy

A Chinese Microcap Waiting for the Rug Pull

Executive Summary

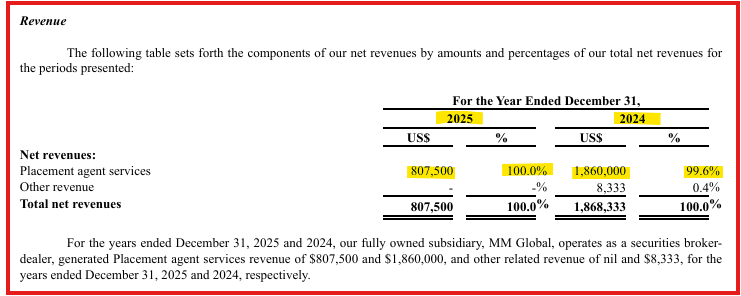

MMTEC is a holding company that, through its subsidiaries, operates a U.S.-registered broker-dealer and a Beijing-based financial technology platform purportedly serving Chinese institutional investors seeking access to overseas capital markets. The U.S. subsidiary, MM Global Securities, Inc., is a FINRA-registered broker-dealer licensed for equity trading and investment banking services. The Chinese subsidiary, Gujia (Beijing) Technology Co., Ltd., provides software and technical infrastructure to institutional clients. In reality, the combined entity generated $807,500 in total revenue in its most recent fiscal year (entirely from placement agent fees), against $3.98 million in operating expenses, and has never achieved profitability from operations to this day.

The company’s entire commercial existence relies on MM Global Securities, Inc., a FINRA-registered introducing broker previously sanctioned for $450,000 for failing to detect hundreds of instances of potential market manipulation on its own platform, and which, by itself, generates 100% of MMTEC’s $807,500 annual revenue. Without MM, MMTEC displays no U.S. revenue, operational presence, and justification for its Nasdaq listing.

MMTEC has a history of operating with the same script for years: tight float, a catalyst, a violent spike, and then a slow grind back to reality as convertible note holders resume converting into the elevated price. The November 2025 squeeze (a run from 31 cents to over $3.89 in a span of two market sessions), followed by a steady grind, was not an anomaly. At the time, the company was on the verge of getting delisted. Somehow, they managed to stay listed as the stock price rose and rose for no apparent reason, which is one of the motives for our report.

As of this report, MTC trades at a market capitalization of $495 million, suggesting a valuation wildly disconnected from fundamentals. Based on its most recent revenue, the stock is pricing in 605x sales, a multiple far exceeding even the most aggressive AI growth companies. We view MTC shares as extremely overvalued and poised for a potential 90-99% correction.

Fugazi Research Analysis

MMTEC is incorporated in the British Virgin Islands (BVI is notorious for shady companies), operates through subsidiaries in Hong Kong, Beijing, and New York, and holds its primary asset through a VIE structure in China. This incorporation imposes minimal fiduciary obligations, as U.S. investors hold shares in a BVI holding company with no direct ownership of any operating assets and no practical enforcement mechanism against management. Creating an entangled web of jurisdictions meant to confuse and mislead investors, and create potential roadblocks for regulators.

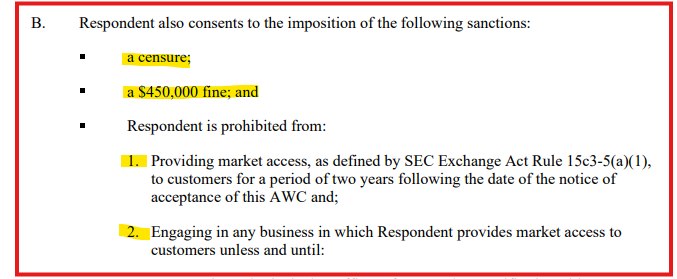

MM Global Securities is MMTEC’s sole revenue source, as 100% of MMTEC’s $807,500 in revenue consisted of placement agent fees earned exclusively through MM Global. This is the same broker-dealer that was censured by FINRA, fined $450,000, and prohibited from providing market access to customers for two years following a September 2022 AWC finding that it failed to detect hundreds of instances of potential market manipulation occurring on its own platform, in its own affiliate’s stock, by customers it could not identify.

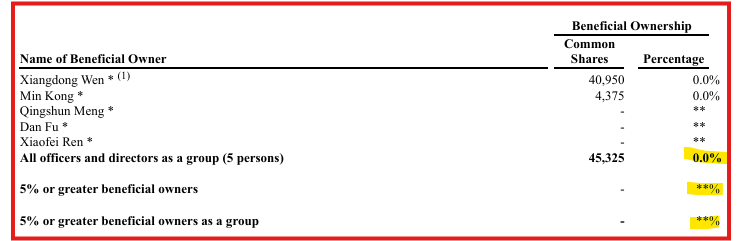

Total insider ownership across all officers and directors is 0.046% combined out of 99,587,811 shares outstanding. The CEO himself drew $141,527 in salary in FY2025 from a company that lost $56 million from continuing operations. This shows there is no alignment between management compensation and shareholder outcomes.

The March 31, 2023, convertible note (Note 2) carries a variable-rate conversion price set at 75% of the lowest closing price during the five trading days immediately preceding the conversion notice, subject to a $0.30 floor. This is a textbook death-spiral mechanic: the holder is economically incentivized to suppress the stock price over the five-day lookback window to cheapen the conversion price and receive more shares per dollar of debt converted

The 4.99% beneficial ownership cap embedded in Note 2 prevents the holder from exceeding 4.99% of outstanding shares at any one time, forcing conversion in tranches. This allows the holder to convert and sell continuously without triggering a Schedule 13D disclosure threshold.

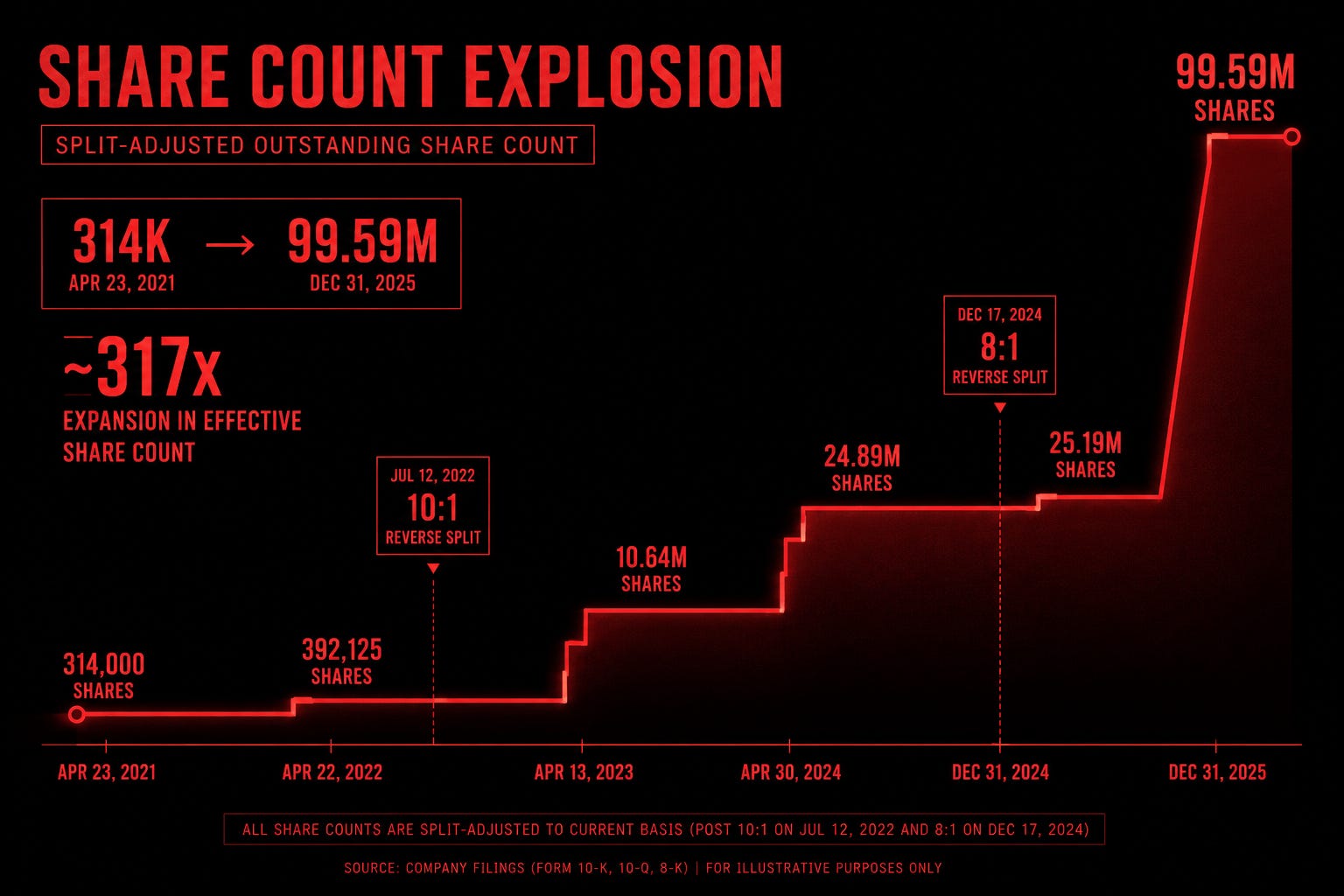

Two reverse splits, 10 to 1 in July 2022 and 8 to 1 in December 2024, artificially tightened the float on each reset. As of today, the cumulative split ratio is 1-for-80, and the company disclosed ongoing Nasdaq minimum bid compliance risk in the FY2025 20-F, signaling a third split is very probable.

In December 2023, MMTEC sold Alpha Mind to XChange for $153 million, with the entire purchase price paid in a promissory note. From this transaction, the company recognized a $53.8 million gain, which was the sole driver of its only profitable year as a public company. However, on April 12, 2025, MMTEC sold $52 million of value of the XChange Note to an unnamed third party for $5,000,000 (a realized loss of $46,988,242).

MTC has a documented history of violent, low-float squeezes with no operational catalyst. The November 2025 short squeeze (a move from $0.31 to $3.89 across two market sessions) occurred on no material news, no earnings release, and no SEC filing.

Based on the fact that the operating business generates $807,500 in annual revenue against $3.98 million in expenses, has never produced a dollar of cash from operations, has no growth catalysts, and 99.6 million shares outstanding after a single conversion event added 74.4 million shares at barely $.50, our analysis shows that this is a squeeze, not a business. Fugazi Research considers MMTEC shares uninvestable at any price above ZERO.

MMTEC Financial Summary

$807,500 in FY2025 revenue compared to $3.9 million in total operating expenses, which represents a 5× expense to revenue ratio. At this rate, the company spent $4.93 for every $1 dollar earned.

At a current market capitalization of approximately $489 million and trailing twelve-month revenue of $807,500, MTC trades at roughly 605 times revenue. For context, high-growth software companies with consistent annual revenue growth and expanding margins rarely sustain revenue multiples above 30 times.

Gross margin fell from 81.6% in 2024 to 21.6% in 2025, a 60% collapse in a single year.

Two consecutive credit losses recognized, totaling $114.1 million ($90.2 million in FY2024 and $23.9 million in FY2025), combined, exceed MMTEC’s total assets of $18.4 million by 6x.

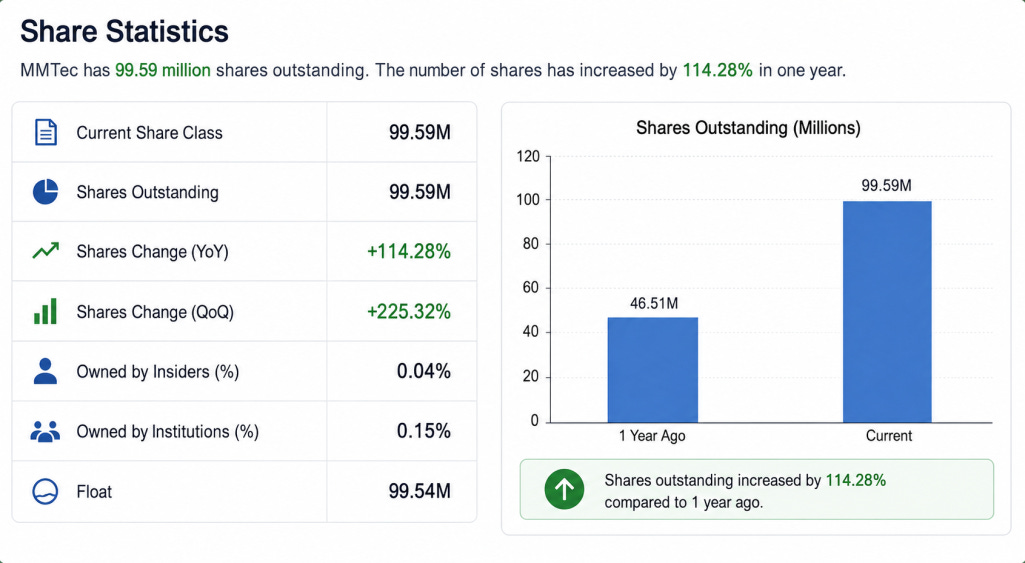

A serious dilution event occurred between December 2024 and December 2025, during which shares outstanding increased from 25,186,864 to 99,587,811, showing that 74,400,947 new shares were issued in a single year, representing a 295% increase in share count.

The cumulative reverse split ratio as of today is 80-to-1. Since the split-adjusted IPO price was $320 per share and the current price is approximately $4.85, IPO investors have lost approximately 99% in split-adjusted terms.

Insiders own 45,325 shares across all officers and directors (0.046% of 99,587,811 outstanding), which signals that executive and top management have zero conviction or stake in the company’s future, while relying solely on shareholders who buy the company’s stock to keep afloat, leaving the losses to outsiders.

Interest expense was $8.68 million for FY2025, compared to $2.4 million the previous year. This represents a 258.6% increase in interest expense driven by the interest on Note 2 prior to its conversion. On $807,500 in revenue, interest expense alone was 10x total revenue.

The accumulated deficit stands at $123,994,872, while total additional paid-in capital is $130,728,219. This means that the company has destroyed 94.9 cents of every dollar ever invested in it.

Taken together, these figures describe a company that has never generated cash from operations, has destroyed 94.9 cents of every dollar ever invested in it, trades at 605 times revenue on the back of a squeeze, and whose primary balance sheet asset is a promissory note its own management sold in the secondary market for 9.6 cents on the dollar.

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

The Playbook

MMTEC did not need a business to generate one of the most violent price dislocations in the China microcap space in late 2025. It needed a structure, which the filings show exactly what that structure looked like and how it was assembled.

By September 2025, the capital structure had been engineered into a configuration that required no fundamental catalyst to produce extreme price movement. The operating business generated $807,500 in annual revenue and lost $3.8 million from operations. The stock was trading below $0.50 and had been under the Nasdaq minimum bid price deficiency for months. On October 27, 2025, Nasdaq issued a formal delisting determination. MMTEC was, by every observable metric, a company on the verge of losing its listing.

What happened was that after the Nasdaq delisting determination, the stock created a predictable market dynamic. Short sellers accumulated positions expecting continued deterioration or delisting, which made the borrow crowded, and the stock became violently responsive to any single large buy order in a thin tape. On November 5, 2025, MTC moved from $0.31 to $3.89 across two market sessions. The move occurred on no material news, no SEC filing, and no operational development of any kind.

The December 2025 series of events confirmed this setup. MTC regained Nasdaq compliance, and through the filing, it was discovered that weeks before the November squeeze (September 2025), the company had already completed the conversion of $36.475 million in principal and $7.495 million in accrued interest into 74,400,947 new shares at $0.591. By the end of December 2025, shares outstanding now stood at 99,587,811.

The stock has continued to grind higher on volume that, since the November spike, has rarely exceeded 500,000 shares on any single trading day and on most days trades fewer than 20,000 shares. Which only means that the price is just being held by a thread.

Any material news, any regulatory development, any additional dilution event, any Nasdaq compliance notice, or simply the exhaustion of the momentum holding the price in place is sufficient to trigger a cascading sell-off with no structural floor to arrest it. The last time this chart looked like this, the stock lost more than 90% of its value in a straight line.

MM Global: The Only Thing Standing

MM Global Securities, Inc. is a FINRA-registered broker-dealer incorporated in Illinois and employs only three registered persons. It is also important to note that it has no disclosed clients, pipeline, or backlog.

In 2023, it contributed $45,837 in placement agent fees, representing 5.2% of MMTEC’s total revenue that year, with consulting services and software development accounting for the rest. In 2024, consulting and software went to zero, and MM Global’s placement fees accounted for 99.6% of MMTEC’s total revenue. In 2025, placement fees fell 56.7% to $807,500, and to date, that figure represents 100% of MMTEC’s total net revenue.

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

A $489 Million Ghost

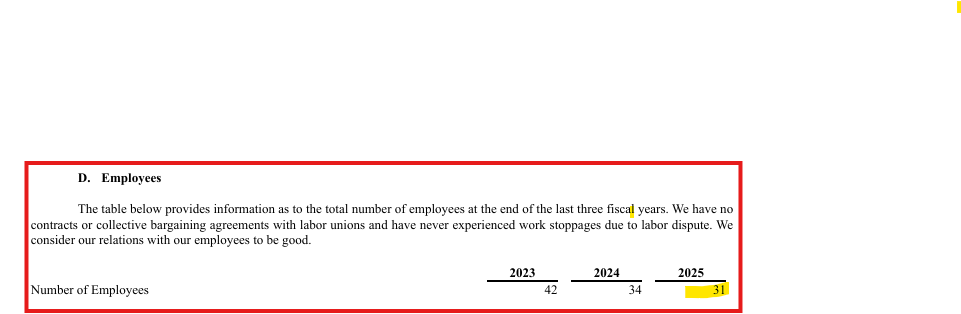

The company is in itself a phantom shell trading at $489 million in market capitalization (as of 05/16/2026) with zero analyst coverage, zero institutional ownership of record, 31 employees, and a primary business domiciled across BVI, Hong Kong, and Beijing (jurisdictions that offer U.S. investors no practical legal protection).

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

Up to this date, no Wall Street firm covers this stock, and there is no institutional fund holding it, which only shows that the price is not a reflection of research or true price discovery, but only a reflection of retail momentum on a name that has been through two documented squeeze cycles, two reverse splits, and a near-delisting.

MM Global: The Only Business, Already Sanctioned

MM Global Securities (MMTEC’s sole revenue-generating subsidiary) was censured by FINRA and fined $450,000 following a September 2022 AWC (Case No. 2019062623001) for three categories of violations:

Failing to establish an AML (Anti-Money-Laundering) compliance program capable of detecting suspicious trading activity, including wash trades, matched orders, spoofing, and layering.

Failing to implement its Customer Identification Program.

Failing to preserve communications of registered representatives in violation of Exchange Act Rule 17a-4.

In FINRA’s own words, the firm lacked reasonable written AML procedures for the surveillance of trading for suspicious activity. MM Global’s own written AML procedures claimed the firm would “make every effort to detect ongoing manipulation in the market,” while simultaneously containing no security applications whatsoever to identify any forms of manipulative trading.

The FINRA’s letter of AWC reveals that MM Global’s primary institutional customer during 2019 (identified as “Customer A”) was a foreign financial institution with over 150 individual traders from a high-risk money laundering jurisdiction, which accounted for nearly all of MM Global’s trading activity that year, and was affiliated with the founders of “Company A,” one of MM Global’s own affiliates.

Separately, in 2020, twelve MM Global customers located in China and Hong Kong placed coordinated sell orders in Company A’s stock on a single day (some within milliseconds of one another & suggesting coordinated trading activity). Most of these customers had been referred to MM Global by Company A itself. MM Global’s registered representatives conducted securities business related to Company A’s IPO via WeChat and personal email accounts, none of which were preserved.

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

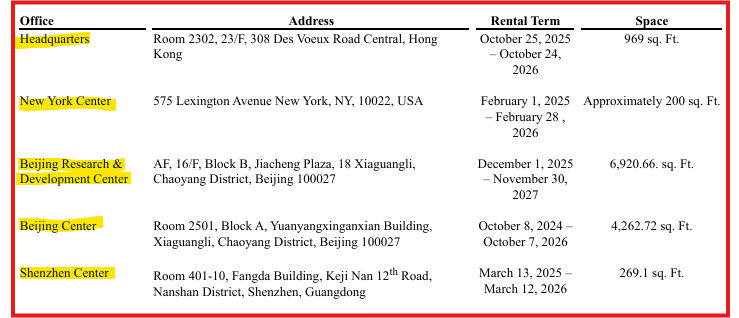

The AWC establishes that the coordinated trading activity in Company A’s stock originated from customers located in China and Hong Kong. Fugazi Research notes that MM Global’s disclosed corporate structure includes subsidiaries domiciled in Beijing and Hong Kong, and that MMTEC currently maintains over 11,000 square feet of undisclosed purpose office space across two Beijing locations. Additionally, a presence in Shenzhen, none of which are associated with any disclosed revenue-generating activity in their 20-F for 2025.

Based on the trading behavior since the November 2025 run-up, the price action raises serious concerns that speculative or potentially manipulative activity may be contributing to the stock’s continued elevation despite the absence of any meaningful operational improvement. Nothing in the underlying business appears to justify the move from sub-$0.25 levels to nearly $5 per share. The stock has seen minuscule volume since November, with most days only trading dozens of thousands of shares. This indicates that trading activity raises serious concerns that artificial or coordinated buying may be contributing to the stock’s continued rise, creating a trading environment that appears increasingly disconnected from legitimate business fundamentals. Similar trading dynamics have historically appeared across highly speculative China-linked microcaps, where price action became detached from underlying operating fundamentals

Inside the Numbers

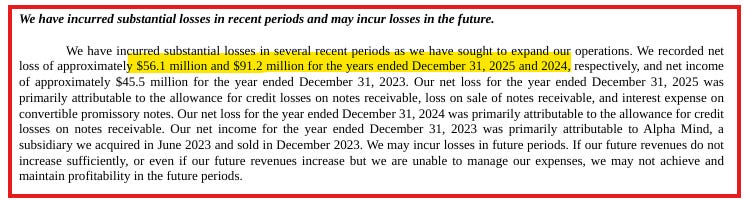

While Revenue fell from approximately $1.87 million during 2024 to just $807,500 during 2025, gross margin deteriorated from 81.6% to 21.6%, Net losses expanded from roughly $4.8 million to more than $56 million over the same period and customer concentration along with single source revenue also became extreme, with Form 20-F disclosing essentially all 2025 revenue came from a single customer relationship tied to placement-agent activity.

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

Gross profit showcases a 60 percentage-point destruction in a single year, driven entirely by increased costs associated with placement agent services at MM Global, the company’s only revenue-generating subsidiary. Gross profit fell from $1,525,250 to $174,500 over 12 months, even as revenue declined 56.7%.

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

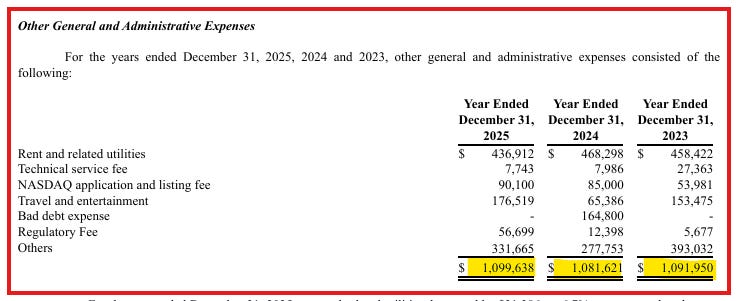

General & Administrative expenses totaled $1,099,638, including $436,912 in rent and utilities across five office locations, $90,100 in Nasdaq application and listing fees, $176,519 in travel and entertainment, and $56,699 in regulatory fees. The company spent $90,100 to maintain its Nasdaq listing and $436,912 on office space, while generating $807,500 in total revenue.

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

Operating loss deteriorated 24.2% despite revenue declining, headcount costs remaining flat, and management cutting compensation. The operating loss is moving in the wrong direction across every metric: revenue down 56.7%, gross profit down 88.6%, and operating loss up 24.2%.

Nothing in the income statement resembles the profile of a rapidly scaling fintech platform; the company’s market behavior, however, is increasingly detached from those operating realities as the capital structure became larger and more active than the underlying business itself.

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

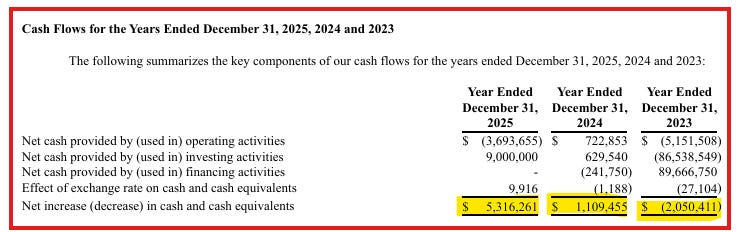

The $9,000,000 in investing cash inflows represents $4,000,000 in XChange note principal repayments and $5,000,000 from the fire sale of $51.99 million face value of the XChange note at a 90.4% loss.

The balance sheet tells a similar story: cash increased during 2025, but not because operations improved (the company remained cash-flow negative); the increase came primarily from financing activity, debt restructuring, and capital-structure changes.

Non-Compliance and Share Count Explosion

The share count history is a dilution extraction record. On April 23, 2021, MMTEC had 25,120,000 shares issued and outstanding, equivalent to 314,000 shares on a split-adjusted basis applying the company’s cumulative 1-for-80 reverse split ratio.

By December 31, 2025, that figure stood at 99,587,811 shares. On a split-adjusted basis, the share count increased 316 times over four years, this should alarm every shareholder in existence as every dollar of value held by a 2021 shareholder has been divided by 316 through a combination of toxic convertible note issuances, original issue discounts, and interrupted twice by reverse splits designed not to return value to shareholders but to reset the minimum bid price clock and enable the next round of dilution. This sequence is a notorious strategy to enrich insiders and orchestrators while leaving investors with worthless shares, as they keep running the stock price to the ground and reverse-split, diluting in a never-ending cycle at the peril of unsuspecting retail investors.

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

What makes the current setup more dangerous is what sits behind the price. In November 2025, MMTEC completed a single-note conversion that issued 74,400,947 new shares at $0.591 (a 295% increase in share count in a single transaction), with shares outstanding rising from 25.2 million to 99.6 million overnight. That supply is now sitting directly above a stock that has just run from sub 50 cents to a high of $9.10 and is being held up by thin volume and no true catalyst. The wall of supply created by the November conversion hasn’t moved yet. This is a company with $807,500 in annual revenue trading at a market cap that the underlying business cannot begin to justify, and the last time this chart looked like this, it lost 93% in a straight line in May 2024.

The Nasdaq Clock

By late 2025, MMTec was operating under significant Nasdaq compliance pressure tied to prolonged minimum bid-price deficiencies. The company ultimately disclosed a delisting determination during October 2025, reinforcing what the market already understood: the stock was running on borrowed time unless something changed structurally.

Compliance windows create unusual conditions in small-cap stocks by compressing incentives into a short period. Short sellers begin positioning for eventual deterioration or delisting, while management teams often rely on reverse splits or capital-market activity to preserve exchange status. The stock itself becomes highly reflexive as positioning, liquidity, and compliance timelines begin to interact.

MTC entered that environment carrying an already fragile capital structure.

This is where many China-linked microcaps become dangerous. Once a stock develops crowded short positioning under a compliance clock, it no longer trades purely on business fundamentals. It begins trading on mechanics: borrow availability, halt bands, SSR restrictions, liquidity gaps, and forced covering behavior. This is what happened on November 5th, when MTC had an almost 1000% run and held up amid erratic short-squeeze behavior while trading hundreds of millions of shares. Short sellers were betting on the delisting and were caught offside. The float at that time of the short, overcrowded squeeze was 25 million. Later in December, MTC regained compliance and immediately diluted its stock to almost 100 million, while its stock price kept floating higher and higher with no demand whatsoever. Since the less than 7-day period of November 5th-10th, MTC has not traded more than 500,000 shares for any single day. Most of these days, it trades barely 20,000 shares. For the stock price to keep going higher and higher on such little volume raises a massive red flag of wash trading stock manipulation from overseas, which is highly probable due to the company’s history regarding this behavior and the fact that it has been fined by FINRA in the past.

The 20‑F explicitly states that the company has incurred substantial losses and may remain loss‑making if revenue does not scale, which is framed as a material risk to the business.

https://www.sec.gov/Archives/edgar/data/1742518/000121390026039499/ea0284046-20f_mmtecinc.htm

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

The China Microcap Pattern

MTC belongs to a category of offshore Nasdaq issuers that became widely scrutinized after The China Hustle documentary brought attention to U.S.-listed China microcaps: offshore holding companies, limited operating visibility, recurring reverse splits, financing-heavy capital structures, and trading behavior disconnected from the scale of the underlying business. These days, the Nasdaq is ripe with China scam stocks, ranging from blatant pump-and-dumps orchestrated by fake characters who infiltrate WhatsApp groups and social media, looking for unsuspecting, lonely victims to swindle into buying stock and eventually dumping it. Unfortunately, these events are very common these days and are tracked by StopNasdaqChinaFraud.com. MMTec displays all the characteristics of being manipulated overseas as a China Hustle-style pump-and-dump scam stock.

Still, the similarities are difficult to ignore. MMTec operates through a multi-jurisdiction structure involving offshore entities, Hong Kong operations, and PRC-linked activities while simultaneously relying on U.S. capital markets for liquidity and exchange access. The company’s operating scale remained extremely limited even as the stock experienced periods of violent speculative activity tied more closely to positioning and float dynamics than to financial performance.

The 20‑F notes that the company is a British Virgin Islands (BVI) holding company and not a U.S. domestic issuer, so it follows BVI law and Nasdaq foreign‑issuer exemptions, which typically allow less stringent governance (e.g., on shareholder rights and board practices).

MMTec is categorized as a non‑accelerated foreign filer; its auditor has not provided a Section 404(b) attestation of internal control over financial reporting, which is permitted but leaves investors more reliant on management’s self‑assessment. The CEO, Xiangdong Wen, also serves as Chairman of the Board, combining executive and oversight roles and reducing the need for independent oversight at the top. This confusing, entangled structure, which is a common theme with overseas scam stocks, is straightforward with MMTec. Combined with their previous run-ins with FINRA, the stock’s upward movement on extremely low volume makes it appear highly suspicious of illegal wash trading, an activity they have been suspected of in the recent past.

Source: MMTEC, Inc. Form 20-F, fiscal year ended December 31, 2025. Filed April 2, 2026.

Typical Wash Trading Scenario:

In low-volume stocks, wash trading is a manipulative tactic in which traders or coordinated groups repeatedly buy and sell the same shares across controlled accounts, creating artificial volume and price movement with virtually no real change in ownership or economic exposure. Much like a frantic game of hot potato, small batches of shares are rapidly passed back and forth at progressively higher prices, simulating buying interest and upward momentum despite almost no genuine outside participation. This illusion draws in unsuspecting investors until the manipulators suddenly dump their holdings in a “rug pull,” causing the price to collapse and leaving retail buyers with heavy losses.

Conclusion

MMTec is not trading on business fundamentals, as there are barely any left to justify the valuation. The company generated just $807,500 in annual revenue while losing tens of millions of dollars, massively diluting shareholders, and relying on financing activity and note restructurings to survive. Beneath the ticker is a business that has never demonstrated sustainable operations, scalable growth, or anything close to what a nearly half-billion-dollar valuation would normally imply.

What drove MTC higher was not execution or institutional demand. It was structured: a tight float, Nasdaq compliance pressure, aggressive convertible mechanics, crowded short positioning, and an illiquid tape that could move violently on very little real volume. The late-2025 squeeze created the appearance of strength, but the filings describe something very different beneath the surface: collapsing margins, recurring losses, an exploding share count, and a balance sheet increasingly dominated by financing activity rather than actual business performance.

This is the recurring pattern seen across speculative China-linked microcaps. Momentum temporarily disconnects the stock from reality; traders chase volatility rather than fundamentals; and the price action itself becomes the story. But eventually liquidity fades, and the underlying business reasserts itself. When that happens, these types of structures historically do not unwind slowly.

MTC now has nearly 100 million shares outstanding, a history of reverse splits, toxic dilution, ongoing Nasdaq risks, and a valuation completely detached from the scale of the underlying operation. Fugazi Research believes MTC’s underlying business doesn’t justify its current valuation and that the stock will ultimately collapse back below $1 in a violent rug-pull before going to zero, just like many worthless Chinese scam stocks.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions-long, short, or otherwise-in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.