$CUE: Reverse Splits, PIPE Dilution, and the Illusion of Recovery

One-time revenue. Permanent dilution.

Executive Summary

CUE Biopharma is a clinical-stage company that has never sold a single commercial product, has never received an FDA approval, and has never generated a dollar of revenue from anything other than licensing rights to assets it developed but could not advance on its own.

Other than its lead oncology program, CUE-101 (which has been in phase 1b for years without a path to commercialization), its most significant endeavors and revenue sources have been terminated since 2025. Its flagship LG Chem partnership produced zero revenue in 2025, and its most recent transaction, which is an $18.9 million licensing arrangement with ImmunoScape, required CUE to accept a 40% equity stake in ImmunoScape as partial consideration, a stake that the company wrote down to zero within the same reporting period it was received.

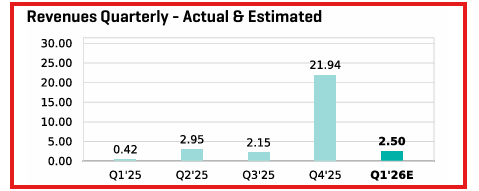

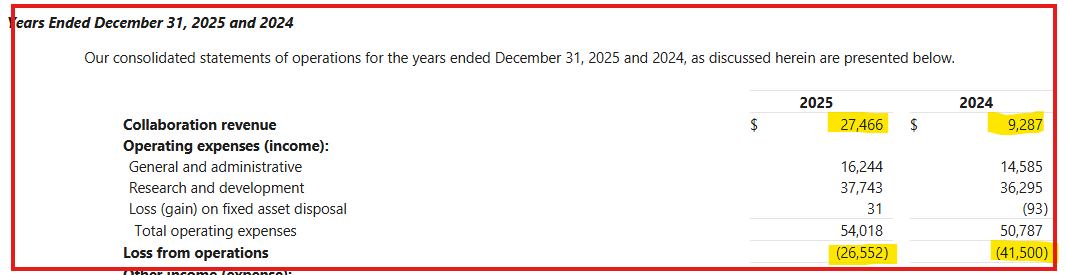

CUE’s Q4 2025 revenue of $21.94 million was not evidence of a recovering business. It was the upfront licensing payment from ImmunoScape that inflated the annual revenue figure to $27.47 million, creating an illusion of recovery. CFRA’s consensus projects 2026 revenue of $1 million. The company has run this scheme before: in 2021, revenue spiked to $14.94 million from collaboration deals, then collapsed by 91.6% to $1.25 million in 2022.

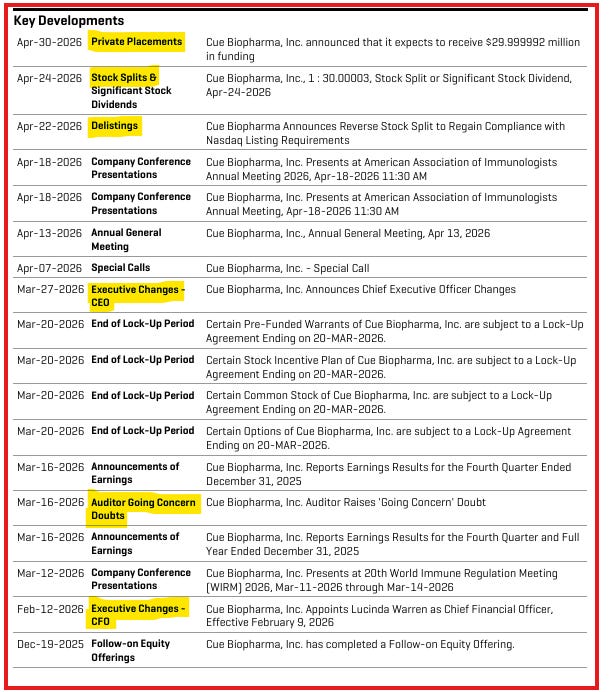

As of December 31, 2025, CUE had only $27.1 million in cash, and an auditor confirmed that it was a going concern. After accounting for the PIPE net proceeds of $28 million and the $15 million upfront payment to Ascendant Health Sciences, the company’s real cash position is about $40 million. Given their current cash burn rate of $35 million to $40 million per year, the runway is closer to 12 to 16 months, making the next capital raise structurally imminent.

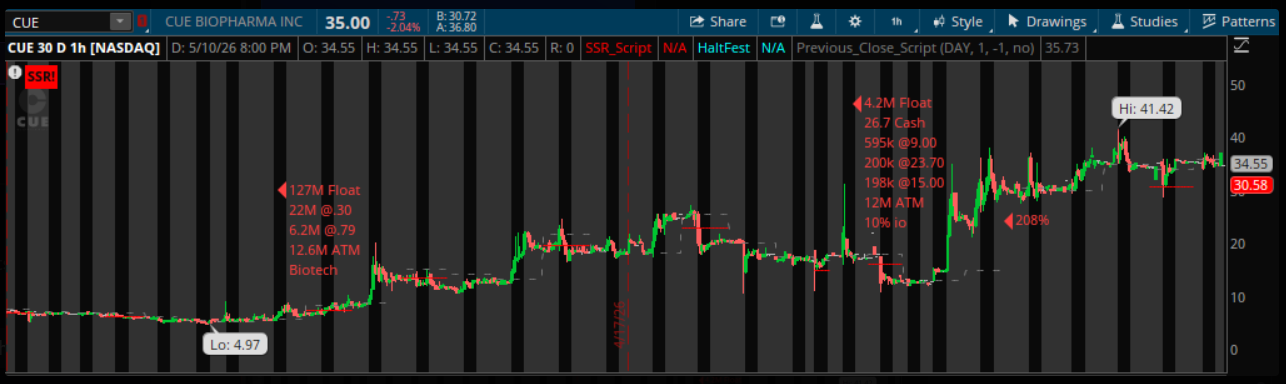

CUE executed an aggressive reverse split, which compressed the float from approximately 97.7 million shares to roughly 3.26 million, in an attempt to restore visibility, regain Nasdaq compliance, and create manufactured momentum. All of these events were followed by a new CEO appointment, a $30 million PIPE deal, and the acquisition of a freshly licensed drug asset from a Cayman Islands company on April 30, 2026. What is even more insidious is that the 3 million post-reverse-split share count was already primed to be diluted by another 4 million shares included in the pipe deal, a 235% expansion in outstanding shares in less than a month. Worth noting is the fact that the PIPE instruments alone covered more than the entire post-split common share base.

The company still has several dilution mechanisms, which it will fully exploit as required by the structure, leaving shareholders with an increasingly diluted position in a company that has accumulated $368.5 million in losses without ever selling a single approved product.

Fugazi Research Analysis

Since its Nasdaq listing, CUE has remained dependent on licensing transactions and repeated equity issuance rather than a self-sustaining commercial business.

The FY2025 revenue increase was overwhelmingly driven by a one-time licensing recognition event rather than recurring commercial activity.

Since its Nasdaq listing in 2022, CUE has raised capital entirely through equity issuance and licensing sales, never through product sales. Between September 2024 and December 2025, the company executed three direct offerings at successive prices of $0.79, $0.50, and $0.28 per share, each offering being cheaper than the last. All while simultaneously maintaining an $80 million ATM facility with Jefferies Securities under which it sold shares for $2.5 million in net proceeds during 2025.

On April 30, 2026, CUE announced a $30 million PIPE alongside a new CEO, a new drug license, and a narrative package designed to justify the post-split price. What the press release did not headline was the fact that $15 million of those gross proceeds left the company immediately as the upfront payment to Ascendant Health Sciences, reducing the real net cash inflow to approximately $13 million after placement agent fees and expenses.

The April 30 PIPE was structured as pre-funded warrants covering 2,727,272 post-split shares at a $0.001 exercise price and accompanying common warrants covering 1,363,636 shares at an $11.00 exercise price (currently in the money as of May 06, 2026), which represents a combined 4,090,908 shares that exceeds the entire estimated post-split common base of 3,255,360 shares before a single instrument is exercised.

The 30-to-1 reverse split executed on April 23, 2026, compressed a share count of 97.7 million shares, which, in itself, was more than double the 47.2 million shares outstanding at December 2023, into a base of approximately 3.26 million shares outstanding.

The April 30 Form 8-K put Shao Lee Lin in the spotlight. The same filing also appointed her as president, CEO, principal executive officer, principal financial officer, and principal accounting officer (all financial controls simultaneously), while granting her 327,537 restricted stock units that were fully vested on her first day of employment.

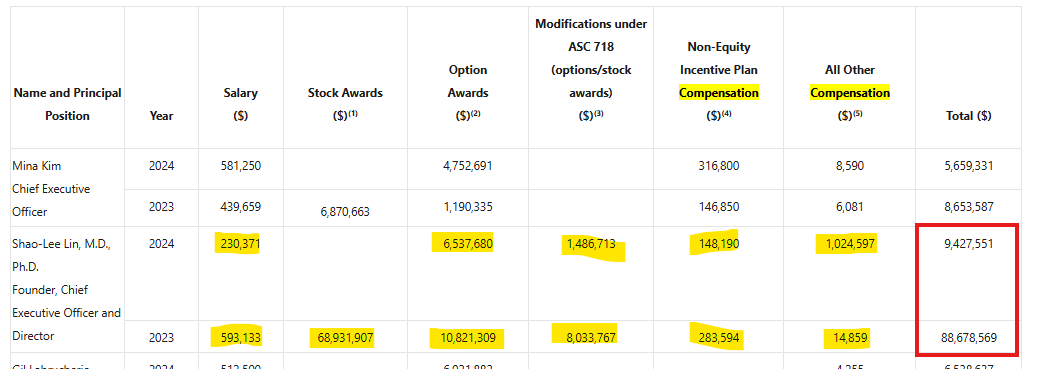

Shao Lee Lin’s prior public-company CEO record is documented in the same filing: she founded ACELYRIN, Inc., led its $540 million IPO in May 2023, and departed in May 2024, fourteen months after ACELYRIN’s lead program failed its primary endpoint and the stock fell 61.61% over two trading sessions. Her reported compensation at ACELYRIN over 2023 and 2024 totaled $98.1 million, while the company’s market cap stood at $322.6 million as of June 2024. To put that into perspective, her compensation was more than that of the CEOs of trillion-dollar market cap companies, Jen-Hsun Huang (50M) and Tim Cook (74M).

There has even been a lawsuit, supposedly, during the time between May 4 and September 11, 2023, Acelyrin and its executives misled investors by overstating the efficacy and commercial prospects of their lead drug candidate, Izokibep, particularly for treating Hidradenitis Suppurativa (HS). The company allegedly promoted strong early clinical results and claimed the drug’s high potency and small molecular size would produce differentiated, superior outcomes, while failing to disclose that the drug was less effective than represented in the placebo-controlled Phase 2b/3 trial. When the company announced on September 11, 2023, that the trial failed to meet its primary endpoint, Acelyrin’s stock price fell more than 60%, allegedly revealing that prior statements had been materially false or misleading in violation of federal securities laws.

The filing record shows a clinical-stage company that has never commercially succeeded at anything it has tried, a reverse split executed to solve a compliance problem rather than a business problem, a massive overhanging dilution, and a CEO whose only prior public-company leadership ended in a clinical failure and securities litigation, all covered by a headline transaction whose obligations exceed the company’s own market capitalization. We consider CUE shares to be significantly overvalued at current prices.

CUE Financial Summary

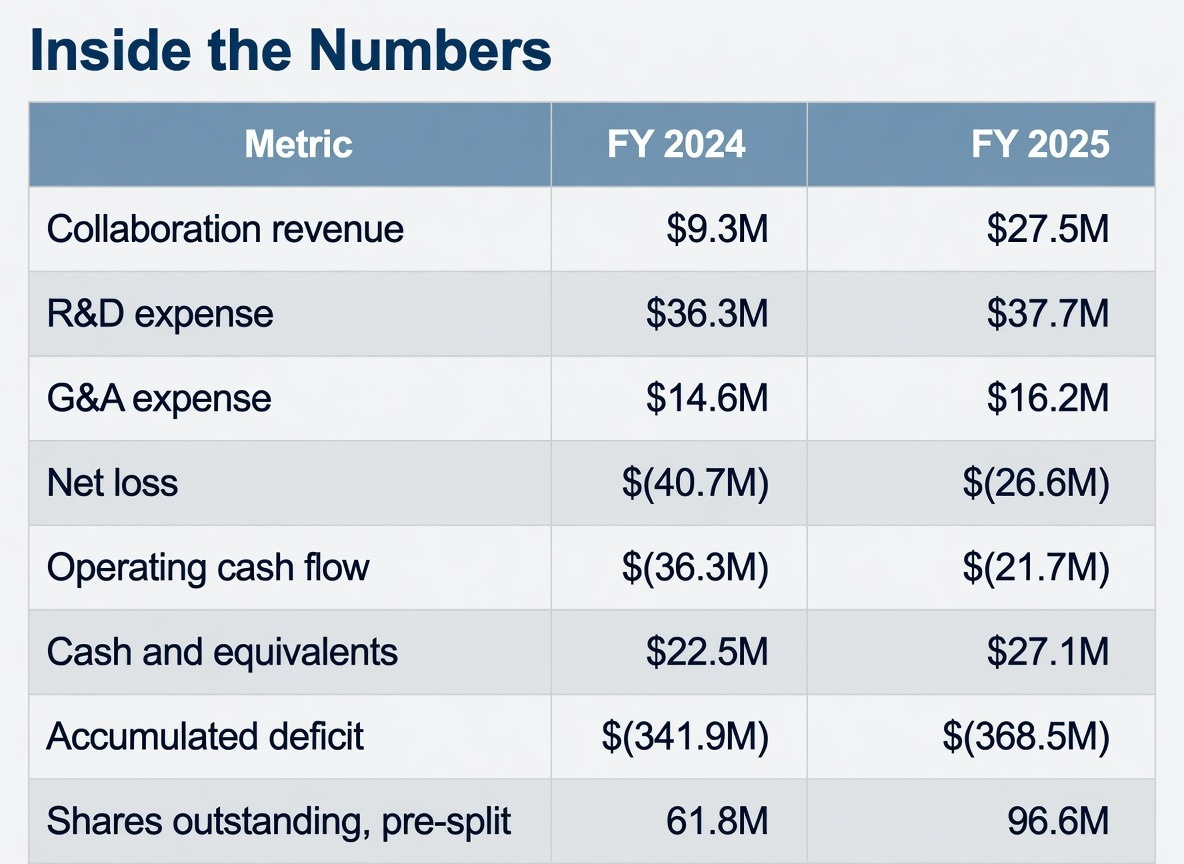

CUE’s accumulated deficit stands at $368.5 million against $394.8 million in total paid-in capital since inception, meaning the company has destroyed $0.93 cents of every dollar ever put into it across its entire operating history, without producing a single approved product or a dollar of commercial revenue to show for it.

With $53.9 million in total operating expenses against $27.5 million in reported FY2025 revenue, CUE spent approximately $1.96 for every $1.00 it earned.

Net loss from operations for FY2025 was $26.6 million, against reported revenue of $27.5 million, resulting in a loss margin of 97%. The company has never reported a profitable year, a profitable quarter, or a period of positive operating cash flow in its public filings.

Without the $26.3 million in financing activity executed during FY2025 (three equity offerings and an ATM program) the company would have entered 2026 with less than $1 million on hand. The FY2025 closing cash balance of $27.1 million is a financing artifact, not an operating achievement.

Since its Nasdaq listing in 2022, CUE has raised capital through equity issuances each fiscal year, including registered direct offerings, warrant issuances, and ATM programs. The April 30, 2026, PIPE extended that pattern with $28 million in net proceeds against an immediate $15 million cash outflow committed to Ascendant in the same transaction.

With 29 employees and $53.9 million in total operating expenses, CUE spends approximately $1.86 million per employee annually to operate a business with $5.0 million in forward contracted revenue.

General and administrative expenses grew 11% in FY2025, from $14.6 million to $16.2 million, in the same fiscal year that the company lost both its Chief Executive Officer and its Chief Medical Officer to departures requiring severance payments, and disclosed going concern language confirmed by its auditors.

On April 30, 2026, the company granted incoming CEO Shao-Lee Lin a compensation package with a combined day-one cost of approximately $6.3 million, against $5 million in total forward contracted revenue. This was awarded to the same executive whose prior public company, ACELYRIN, reported $98.1 million in her compensation across 2023 and 2024 before its lead program failed and the stock fell 61.61% in two sessions.

Source: Cue Biopharma, Inc. Form 8-K, Filed April 30, 2026.

Source: Cue Biopharma, Inc. Form 10-K, fiscal year ended December 31, 2025.

Source: CFRA Quantitative Stock Report, Cue Biopharma, Inc., May 3, 2026. Data provided by S&P Global Market Intelligence.

The Playbook

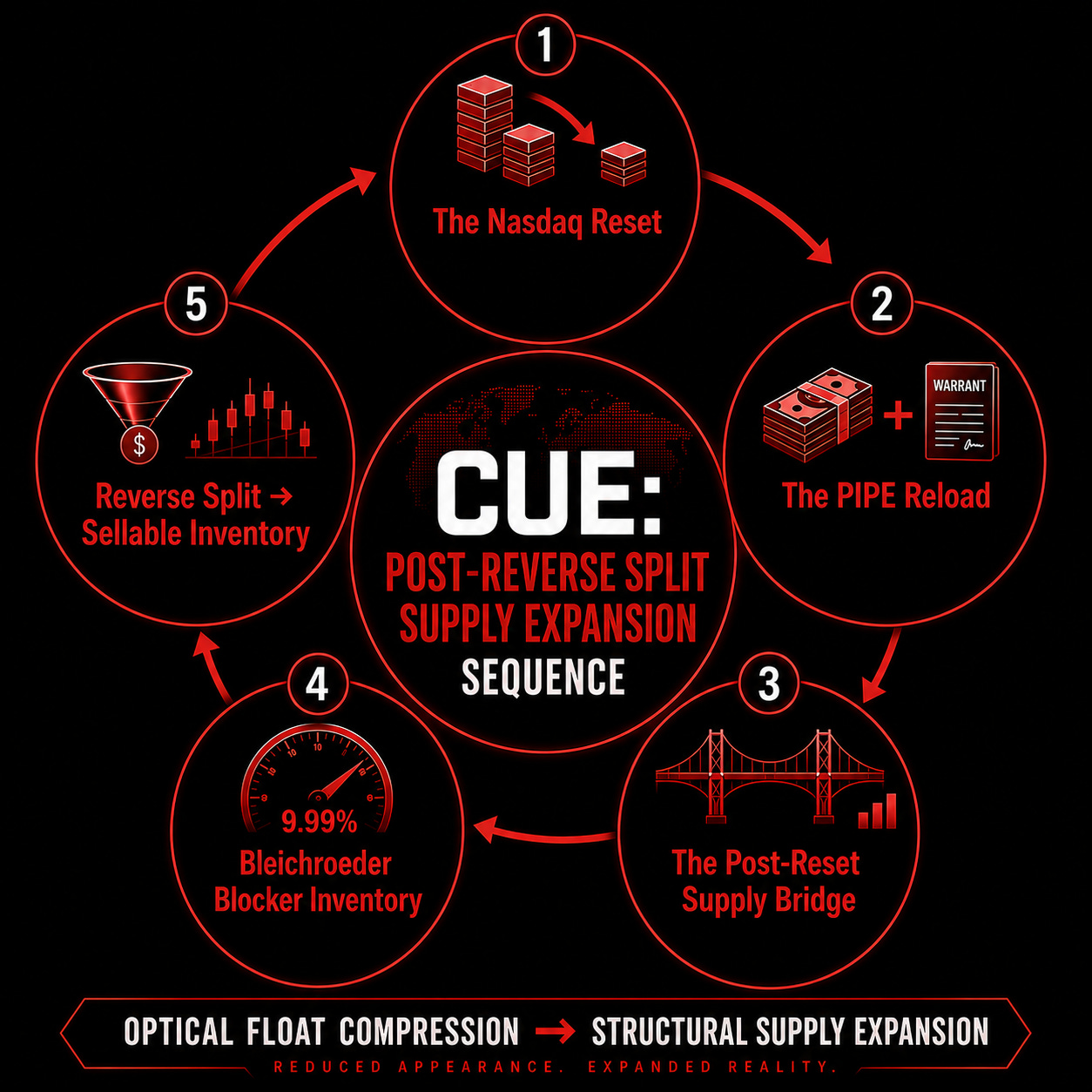

Between March 16 and April 30, 2026 (a 45 day period) the following events occurred at Cue Biopharma in this exact order: auditors confirmed going concern, four simultaneous lock-up agreements expired, the acting CEO announces her resignation, a Nasdaq delisting warning was issued, a 30 to 1 reverse split was executed, a new CEO was installed, a $30 million private placement was announced, and a drug license from a Cayman Islands company arrived as partial consideration.

Make no mistake, these were engineered events; the sequence was not the product of coincidence. It was part of the plan, which is a common toxic dilution cycle method, to enrich certain people involved with the company. Every piece arrived exactly when the structure required it, the reverse split to reset the float when it needed compressing, the narrative when the reset needed covering, and the capital when the narrative needed credibility.

Source: CFRA Quantitative Stock Report, Cue Biopharma, Inc. May 3, 2026. Data provided by S&P Global Market Intelligence.

CUE’s Form 10-K already showed the setup before the Apr. 30 financing window opened. The company had no product sales revenue, no FDA-approved commercial product, negative operating cash flow, a going-concern warning, and a share count that had expanded to 97.7M shares before the reverse split.

The first move was accounting optics. The FY2025 revenue increase came primarily from non-recurring licensing recognition tied to the ImmunoScape transaction, not commercial demand. The apparent improvement in operations preceded another financing reset.

The second move was Nasdaq optics. On Apr. 23, 2026, CUE executed a 1-for-30 reverse split under its Form 8-K. The split reduced the visible common share base from 97.7M to roughly 3.26M. Authorized common shares remained unchanged. The denominator was compressed. The issuance runway remained open.

The third move came eight days later. On Apr. 30, CUE filed a Form 8-K covering a new CEO, the Ascendant license, a $30M PIPE, pre-funded warrants, common warrants, Rule 5635 stockholder approval gates, lock-up releases, top-up rights, and resale registration obligations. One filing window rebuilt the share-supply stack that the reverse split had just compressed.

CFRA’s quarterly revenue data shows that from Q1 through Q3 2025, revenue averaged $1.84 million per quarter. Q4 2025 spiked to $21.94 million on the ImmunoScape upfront recognition event; Q1 2026 is expected to be $2.50 million, which would represent an 88.6% quarterly collapse from the peak.

Source: CFRA Quantitative Stock Report, Cue Biopharma, Inc. May 3, 2026. Data provided by S&P Global Market Intelligence.

The PIPE offering alone covered 4.09M shares equivalent. That is larger than the estimated post-split common base. Ascendant received another 551,724 pre-funded warrants as license consideration. The Form S-8 then registered 3.0M shares under the 2026 Inducement Stock Incentive Plan.

CUE reduced the visible common base to roughly 3.26M shares. The Apr. 30 Form 8-K and Form S-8 added or registered roughly 7.64M additional shares-equivalent before Ascendant top-up shares, Lin’s top-up option, older warrants, the S-3 shelf, or ATM capacity.

Registration rights create the exit path. The PIPE Registration Rights Agreement requires CUE to file a resale registration statement within 30 days after closing. The Ascendant agreement requires CUE to register resale of the Ascendant warrant shares within 45 days after issuance. Private paper becomes registered paper on a filing schedule.

The ownership table adds another layer. The DEF 14A shows Bleichroeder affiliates with 9.99% beneficial ownership, while the footnote excludes 6.746M additional warrant shares due to beneficial ownership blockers. The cap limits reported ownership. It does not eliminate the inventory.

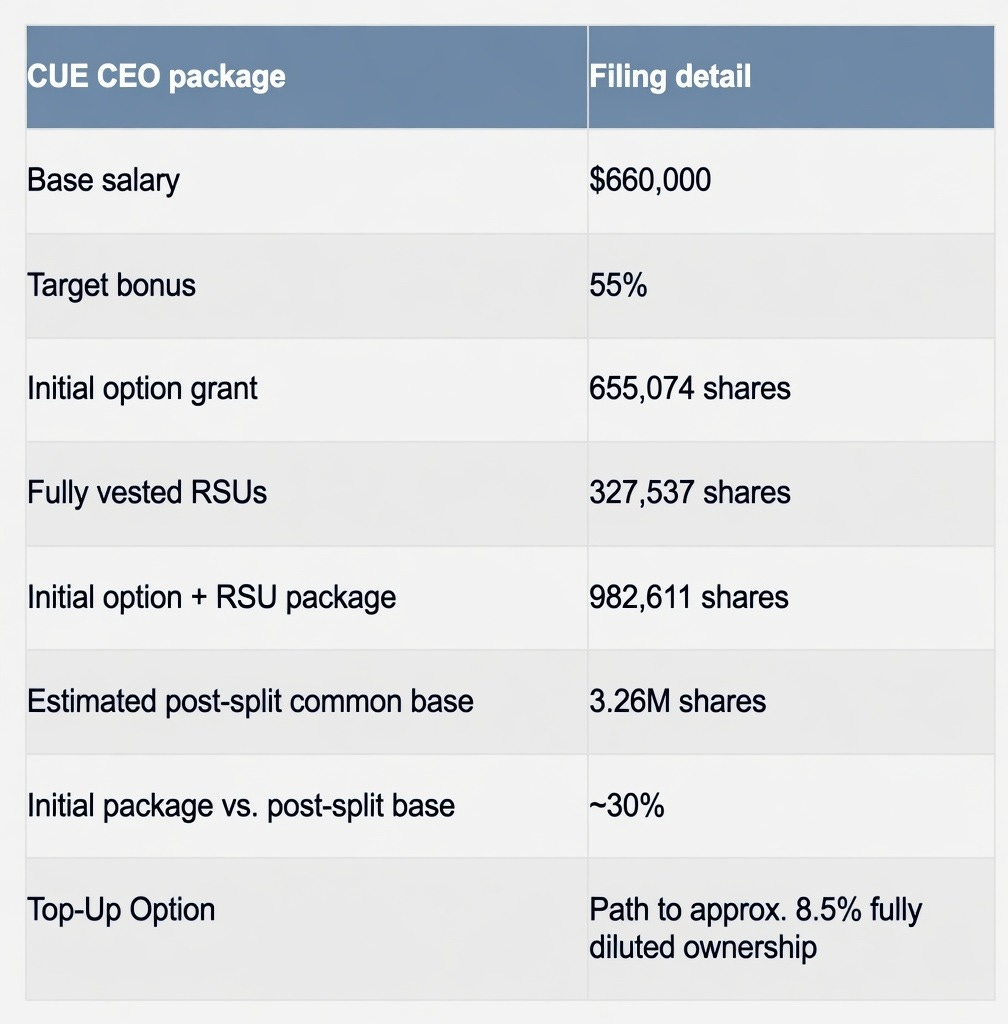

Management economics were added to the same reset. CEO Shao-Lee Lin received options and RSUs covering 982,611 shares, representing roughly 30% of the estimated post-split common base, plus a top-up path to approximately 8.5% fully diluted ownership upon specified milestones. The Form S-8 registered the inducement pool the same day the Form 8-K disclosed the financing stack.

The sequence is the signal, here:

license revenue first → reverse split second → PIPE and licensor warrants third → resale registration → inducement equity alongside it.

Source: Cue Biopharma, Inc. Form 10-K, fiscal year ended December 31, 2025.

Source: Cue Biopharma, Inc. Form 10-K, fiscal year ended December 31, 2025.

CUE’s largest reported quarter came after the company licensed CUE-100 series oncology rights to ImmunoScape. The Form 10-K states that the ImmunoScape transaction price included $15.0M in upfront payments and $3.9M in fair value for a 40% equity interest in ImmunoScape. The Form 10-K also states that the revenue was recognized at a point in time when the licenses were granted.

That is the key accounting event.

The Q4 revenue spike was due to the monetization of pipeline rights. It was not evidence of approved product demand. The Form 10-K still shows a business dependent on licensing monetization and external financing despite the temporary revenue spike. The cash-flow statement did not confirm a turnaround. CUE generated $27.5M of FY 2025 collaboration revenue and still used $21.7M of cash in operating activities. The Form 10-K also disclosed substantial doubt about the company’s ability to continue as a going concern.

The share count moved in the other direction. CUE ended FY 2024 with 61.8M shares outstanding and FY 2025 with 96.6M shares outstanding. By Mar. 13, 2026, the Form 10-K cover page showed 97.7M shares outstanding before the 1-for-30 reverse split. The numbers show the structure: a license-accounting revenue spike, negative operating cash flow, an expanding accumulated deficit, and pre-split share count growth. The Form 10-K revenue line did not remove the financing need. The reverse split was smoke and mirrors as the stock price before the split was less than .50 a share with incoming dilution set to drag it down even lower.

The CEO Reset: Shao-Lee Lin’s Public-Market Precedent

CUE’s Apr. 30 Form 8-K placed Shao-Lee Lin at the center of the post-reverse-split reset. The same filing appointed Lin as President, Chief Executive Officer, board member, principal executive officer, principal financial officer, and principal accounting officer. It also gave her PIPE participation, inducement equity, and a top-up path tied to fully diluted ownership.

Source: Cue Biopharma, Inc. Form 8-K, Filed April 30, 2026.

On April 30, 2026, the company simultaneously structured one of the most generous executive compensation packages in its history for an incoming CEO joining a going concern business with 29 employees and no commercial revenue. Shao-Lee Lin received a $660,000 base salary, a 55% target bonus, and 327,537 restricted stock units fully vested on her first day of employment (representing approximately $4.3 million in immediate equity value at the April 30 closing price). Her initial equity package of 982,611 shares across RSUs and options represents approximately 30.2% of the entire post-split common share base, with a contractual top-up path to 8.5% of fully diluted shares following specified milestones. The outgoing interim CEO, Lucinda Warren, received a separation package totaling $584,010. Combined, the executive transition cost CUE approximately $7.9 million (157% of the company’s total forward-contracted revenue) in the same filing window that management described as a transformative financing event.

Source: Cue Biopharma, Inc. Form S-8, Filed April 30, 2026.

The timing is the point. The CEO package arrived in the same filing window as the Ascendant license, the $30M PIPE, pre-funded warrants, common warrants, Rule 5635 approval gates, resale registration obligations, lock-up releases, and top-up rights. Lin’s prior public-company CEO record is relevant because CUE’s own Form 8-K identifies her as ACELYRIN’s founding CEO and director from July 2020 to May 2024. ACELYRIN priced its IPO at $18.00/share, sold 30.0M shares, and raised $540M in gross proceeds. ACELYRIN Form 424B4, May 5, 2023

The ACELYRIN IPO-to-readout sequence became a securities litigation event. The class action complaint names ACELYRIN, Shao-Lee Lin, Mardi Dier, and Gil Labrucherie as defendants. The complaint alleges false or misleading statements tied to Izokibep’s clinical and commercial prospects during the May 4, 2023, to Sept. 11, 2023, class period. It also states that ACELYRIN sold 30.0M IPO shares at $18.00/share and received $502.2M after underwriting discounts and commissions. The complaint alleges that ACELYRIN announced on Sept. 11, 2023, that Izokibep failed to meet statistical significance on the primary HiSCR75 endpoint in the Phase 2b/3 trial for hidradenitis suppurativa. The complaint states that ACELYRIN’s stock fell $17.19/share, or 61.61%, over the following two trading sessions, closing at $10.71/share on Sept. 13, 2023.

Lin’s compensation remained material through the ACELYRIN reset. ACELYRIN reported $88.7M of total compensation for Lin in 2023 and $9.4M in 2024. The same Form 10-K reported aggregate non-affiliate market value of approximately $322.6M as of June 30, 2024. ACELYRIN Form 10-K, FY 2024

Anatomy of the Mirage

CUE entered April 2026 with a Nasdaq minimum-bid problem, going-concern language, no product-sales revenue, and a pre-split share count of nearly 97.7M shares. The Form 8-K sequence shows the mechanics of the reset.

The Apr. 23 Form 8-K compressed that base through a 1-for-30 reverse split. The Apr. 30 Form 8-K then loaded the post-split structure with PIPE warrants, Ascendant warrants, resale rights, Rule 5635 approval gates, top-up mechanics, and inducement equity.

The post-split share count was stale within eight days.

The PIPE reload

On Apr. 30, 2026, CUE reloaded with upcoming near-term dilution with a PIPE. The PIPE instruments alone cover more shares than the estimated post-split common base.

Registration rights: the exit path

The April 30 PIPE came with a resale registration statement covering the shares underlying the PIPE pre-funded warrants and common warrants within 30 days after closing. This means that there will be incoming downward selling pressure from a new, significant supply soon.

Ascendant’s ownership protection

CUE licensed Ascendant-221 / UB-221 from Ascendant Health Sciences Ltd., a Cayman limited company. The Form 8-K gives CUE rights outside mainland China, Hong Kong, Macau, and Taiwan, while Ascendant retains defined rights in those territories. CUE agreed to pay $15.0M upfront, up to $676.5M in potential milestones, and tiered royalties on future net sales.

Existing common holders face dilution from the transaction, while Ascendant receives a contractual mechanism designed to preserve ownership and value thresholds.

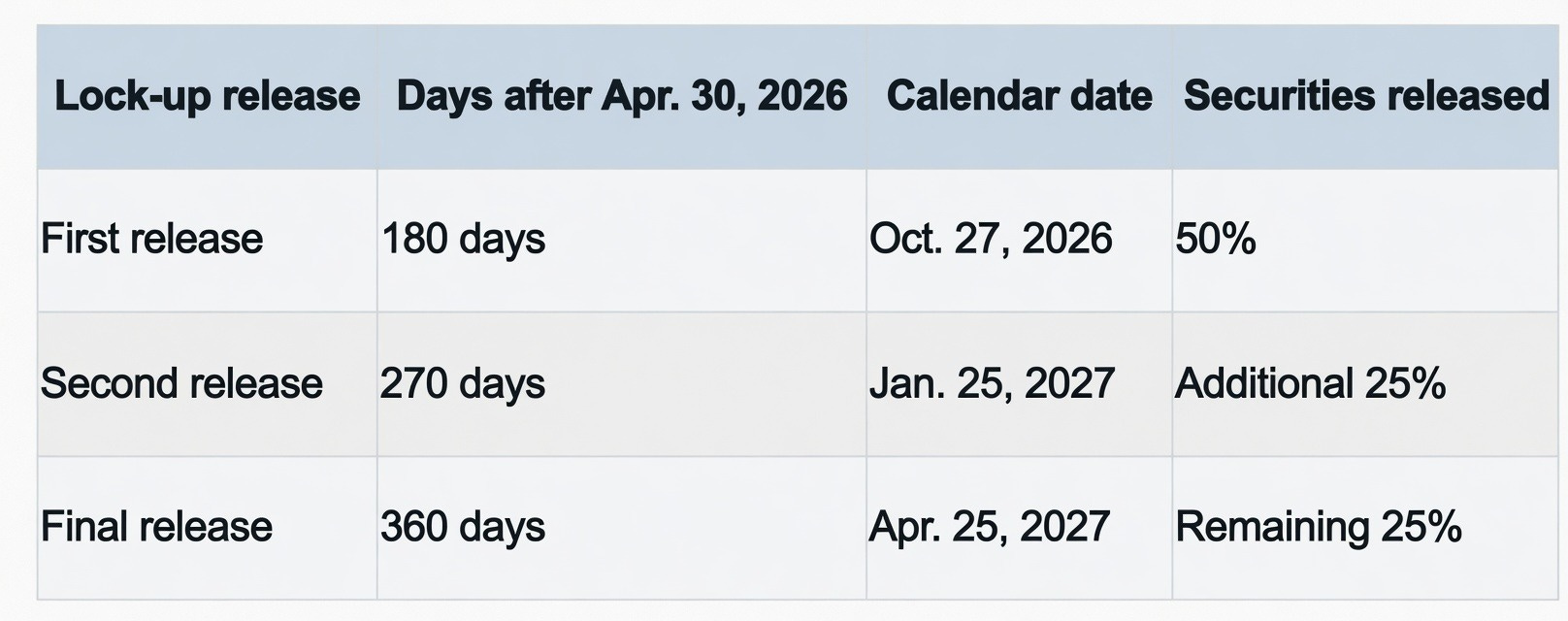

The lock-up release schedule

Ascendant’s lock-up restricts transfer of subject securities, but the release schedule is already set in the Form 8-K, which will trigger immediate market supply.

Assuming Apr. 30, 2026, as the reference date, the lock-up releases on this calendar:

The S-8 layer

On April 30, 2026, CUE filed a Form S-8 registering 3.0M shares under its 2026 Inducement Stock Incentive Plan. The filing fee table values the registered shares at $43.98M. In reality, CUE registered a new equity pool equal to roughly 92% of the visible post-split common base.

The CEO-specific economics are addressed separately. The S-8 shows how quickly the post-split denominator reopened.

The post-reset supply bridge

The reverse split made the share count look smaller, while in reality, the April 30 filings made the structure larger. The estimated post-split common base was approximately 3.26M shares. The Apr. 30 Form 8-K and Form S-8 added or registered approximately 7.64M additional share equivalents.

Bleichroeder and the blocker inventory

The DEF 14A identifies affiliates of Bleichroeder LP as a five-percent holder. The beneficial ownership table discloses 4,997,240 common shares and 5,265,630 shares underlying warrants as beneficially owned, with ownership capped at 9.99%.

At CUE, the 9.99% cap marks the point where ownership disclosure ends and warrant inventory continues.

The Reverse Split that became sellable inventory

CUE’s Form 10-K describes an at-the-market program with Jefferies under an $80M open market sale agreement. The pattern is capital access through repeated equity-linked issuance: ATM shares, underwritten stock, pre-funded warrants, and common warrants.

Conclusion

CUE entered April 2026 with no commercial product revenue, negative operating cash flow, going-concern language, and a capital structure already stretched by years of repeated issuance. The company then executed a 1-for-30 reverse split, temporarily compressing nearly 98 million shares to roughly 3.26 million shares outstanding, creating the appearance of scarcity while leaving the underlying financing framework intact.

Within days, that compressed structure was rebuilt with PIPE warrants, pre-funded warrants, inducement equity, resale registration obligations, top-up protections, and additional issuance pathways. The visible float was reduced, but the underlying supply stack expanded almost immediately. In our view, the reverse split did not repair the business; it reset the financing mechanism.

The company’s apparent FY2025 improvement was also built on non-recurring licensing and accounting recognition, rather than on sustainable commercial demand. Q4 revenue created the illusion of a recovery, while forward estimates already point to a return to collapse. CUE still has no evidence of a durable commercial business capable of funding itself without repeated access to external capital.

The April 30 filings also introduced structural protections for counterparties that common shareholders do not share. Through top-up rights, resale registration obligations, change-of-control protections, and warrant-heavy financing mechanics, the structure increasingly protects the paper above and around common equity while leaving ordinary shareholders exposed to dilution, supply, and downside.

Ultimately, we believe the filings describe a company engineering temporary stability through capital structure mechanics rather than solving the underlying economic reality of the business. As registration windows open and additional supply reaches the market, shareholders may discover that the post-split scarcity narrative was temporary, while the dilution infrastructure behind it was permanent. In our view, the warning is clear: CUE does not need a failed clinical outcome to damage shareholders; the capital structure is already built to do that on its own.

At these levels, CUE shares are pricing a narrative that the filing record does not support. Prior to the reverse split, CUE was non-compliant and trading at almost pennies on the dollar. We consider CUE shares to be significantly overvalued and on the verge of a drastic 95% correction back to sub-$1 per share, once fully diluted.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions-long, short, or otherwise-in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.

ATMs = 🚩