$CDIO: A Heartbreaking Diagnosis for Investors

Near-zero revenue, relentless dilution, and a wannabe biotech story that raises serious questions.

Near-zero revenue, heavy dilution, and a wannabe biotech story that raises serious questions.

Fugazi Research Analysis

Cardio Diagnostics Holdings Inc (CDIO) is a 2022 de-SPAC that was born from a blank check company called Mana Capital Acquisition Corp (MAAQ), and an underwriter called Ladenburg Thalmann & Co. Both of them were led by Jonathan Intrater, a known serial SPAC sponsor whose track record includes a civil lawsuit alleging fraud in a private placement, and two completed SPAC’s that have, combined, destroyed 99% of investor capital.

As the SPAC’s merger deadline approached after a series of unsuccessful targets, MAAQ ultimately settled on Cardio Diagnostics (CDIO): a company that had generated only $901.00 in cumulative revenue over its entire operating history at the time of the merger.

Hidden, but central to this structure, is Mao Tong, a Hong Kong-based lawyer with a 20-year career at firms such as Squire Patton Boggs, which specialize in structuring Chinese capital into U.S. public markets by navigating disclosure requirements. Mao appears exactly once in CDIO’s entire SEC filing history as the owner of all the voting interests of Mana Capital LLC. In October 2022, the day after the de-SPAC closing, Mana Capital transferred its entire position to a shell vehicle called Juventus LLC and to other undisclosed recipients. From that date forward, no identifiable successor appears to have filed a beneficial ownership report with the SEC, leaving the ultimate holders of those shares unclear in the public record.

Mana Capital LLC, the holding vehicle controlled entirely by Mao Tong, acquired 1.55 million shares for a heavily discounted price of $25,000, which, if sold at lock-up expiry, would mean a +15,000% return on a company that only generated $901 in revenue up to its de-SPAC.

According to their most recent 10-Q, 100% of the company’s revenue comes from product tests for cardiovascular disease, totaling $11,270 for the period, compared to $29,264 in spending on office and computer equipment for the same period.

Also, in its latest 10-Q, CDIO reports an accumulated deficit of $27.8 million, meaning the company has consumed nearly $28 million of investor capital since inception while generating only tens of thousands of dollars in total revenue. At recent trading prices, that deficit is several times larger than the company’s entire market capitalization.

Since its de-SPAC in October 2022, CDIO has expanded its float by 476%. This aggressive and non-stop, dilutive cycle has left shareholders with a fraction of their initial investment and heavy accumulated losses per share.

Given

a) the opaque ownership transfers following the de-SPAC transaction,

b) the involvement of entities whose ultimate beneficiaries are unclear,

c) insignificant revenue,

d) a clear path to continued operating losses, and

e) increasing share issuance resulting in accelerating shareholder dilution

We consider CDIO’s shares to be completely uninvestable and of Zero value.

CDIO Financial Summary

For the nine months ended September 30, 2025, revenue totaled $11.3k, while net loss for the same period totaled $5.03 million, representing a -44,500% margin, meaning the company lost more than $445 to generate $1 of revenue.

That $11.3k in revenue also represents a massive 63% decline from the $30.4k generated during the same period in 2024, which the company attributed to the loss of a single customer (Family Medicine Specialists).

The cash burn rate currently stands at $4.36 million for the 9 months ended 2025, while cash reserves amount to $6.3 million for the same period, indicating a runway of just over a year of operations.

Cash from sales of common stock and warrants amounted to $3.5 million for the nine months ended September 30, 2025. Compared to the $11.3k of total revenue for the same time period, meaning that the company raised 309x more money from dilution than revenue.

As of November 12, 2025, the company has raised more than $15 million in capital through sales of common stock. Over time, it has had minimal sales of $65k since its inception, looking more like a failed science experiment than a true company.

Outstanding shares increased from approximately 9.5 million as of November 7, 2022, to 54.8 million as of March 11, 2026 (30:1 reverse split adjusted), a 476% increase, translating into 83% shareholder dilution since the company’s inception.

Despite generating only $11.3k in revenue for the nine months ended September 30, 2025, the CEO received a $300k annual salary, more than twenty-five times the company’s total revenue during that period.

Source: CDIO Form 10-Q quarterly period ended September 30, 2025

Source: CDIO Form 10-K annual period ended December 31, 2024

Executive Summary

Cardio Diagnostics Holdings (CDIO) markets itself as an AI-powered, precision cardiovascular diagnostics company positioned to revolutionize early heart disease detection. The financial statements, the capital markets history, and the ownership structure tell a very different story.

CDIO was born from desperation. Mana Capital Acquisition Corp (MAAQ), a blank check company, cycled through at least 12 failed merger candidates, including a beverage distributor, before landing on Cardio Diagnostics. At the time of the de-SPAC closing in October 2022, Cardio Diagnostics had generated a grand total of just $901.00 in revenue during its entire operational history. Central to this structure is Tong Mao, a Hong Kong-based lawyer specializing in structuring Chinese capital into US public markets by navigating disclosure requirements.

Despite years of development and commercialization claims, Cardio Diagnostics generated less than $35,000 of revenue in all of 2024 while losing over $8 million. In the first nine months of 2025, revenue totaled just $11,270. This figure amounts to a few thousand dollars per quarter from a company that has been commercially active since 2021. Total cumulative revenue since inception stands at approximately $65,000, while the company has raised more than $15 million in equity capital over the same period.

Management has repeatedly relied on selling stock to fund operations, executing a 1-for-30 reverse stock split in May 2025 solely to maintain its Nasdaq listing while keeping an active at-the-market (ATM) equity facility open with capacity sufficient to dilute existing shareholders substantially. Since the de-SPAC closing, the public float has expanded by approximately 476%.

CDIO fits a familiar and well-documented microcap pattern: a compelling AI narrative, virtually zero revenue, constant cash burn, founder shares transferred to unidentified recipients at zero cost on the day of the merger closing, a board member profiting from capital raises, and a capital structure built for more dilution.

The core business currently produces only a few thousand dollars per quarter while burning through nearly half a million dollars in cash every month. The result is a stock that trades more like a speculative, low-float momentum vehicle than a healthy operating business.

1. The Undisclosed SPAC Origin

How CDIO became a public company raises important questions. The issue is not simply that the company had generated less than $1,000 in total revenue at the time of the merger, or that it emerged as the final candidate after at least twelve failed SPAC targets. The more relevant question is who ultimately selected this company, why it was chosen, and who benefited from the transaction. At the center of that process are two key players.

Jonathan Intrater, a managing director at Ladenburg Thalmann & Co., served as CEO, Chairman, and sole officer of Mana Capital Acquisition Corp (MAAQ). At the same time, Ladenburg Thalmann acted as the SPAC’s underwriter, creating a dual role that was explicitly disclosed as a potential conflict of interest in MAAQ’s S-4 registration statement.

Above: Jonathan Intrater shown as CEO of MAAQ, and Managing Director at Ladenburg (the underwriter)

Source: Form S-4 MAAQ/Cardio Diagnostics, Inc. Merger October 7, 2022

Intrater previously served as a board member and Audit Committee Chairman of GreenVision Acquisition Corp, whose de-SPAC company, Helbiz Inc. (HLBZ), now trades at $0.22, a 97.83% decline from its original value, and has been delisted from Nasdaq as of February, 2024.

Above: Jonathan Intrater as Audit Committee Chairman and Director at GreenVision Acquisition Corp.

Source: Form S-1 GRNV/ Public offering November 14, 2019

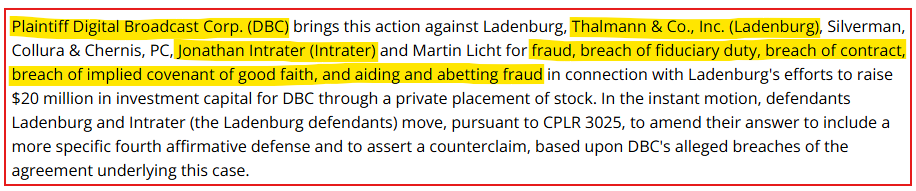

Prior to his SPAC activity, Intrater was named personally as a defendant in a civil lawsuit filed in the New York Supreme Court, alongside Ladenburg Thalmann & Co., alleging fraud, breach of fiduciary duty, aiding and abetting fraud, and breach of contract, all of these accusations arising from Ladenburg Thalmann’s efforts to raise $20 million in a private placement for Digital Broadcast Corporation. The case was ultimately appealed and dismissed on the grounds that the plaintiff (a development-stage company that had never generated any revenue) could not establish damages with certainty.

Above: Jonathan Intrater as defendant in Digital Broadcast Corp. v Ladenburg, Thalmann & Co.

Source: Digital Broadcast Corp. v Ladenburg, Thalmann & Co., Inc. 2008 NY Slip Op 50955

In summary, two completed de-SPACs, two companies that have destroyed the majority of investor capital, one civil lawsuit alleging fraud in a private placement, and a conflict of interest as the underwriter of the original blank-check companies. This is not a coincidence. It’s a pattern.

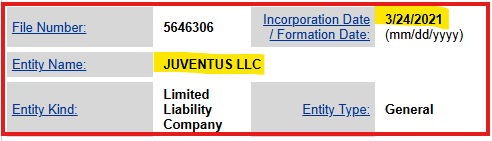

Mao Tong is the concealed but central player to this structure; his experience as a Hong Kong-based lawyer with a two-decade career at firms like Squire Patton Boggs makes him a specialist in structuring and deploying Chinese capital into US public markets by navigating through disclosure requirements. His role, however, is hidden; as early as the blank-check incorporation, Mao controlled the entire SPAC through a dual-layer ownership structure. Being the sole member and majority voter of Mana Capital LLC, and as the controlling individual for Juventus LLC, a Delaware limited liability company incorporated on March 24, 2021 (2 months before the SPAC itself was formed). Together, both entities held 1.62 million founder shares for a staggering price of $25,000.00 or $.015 per share.

Above: Juventus LLC’s incorporation date and registration in the state of Delaware.

Source: State of Delaware/ Department of State/ Division of Corporations

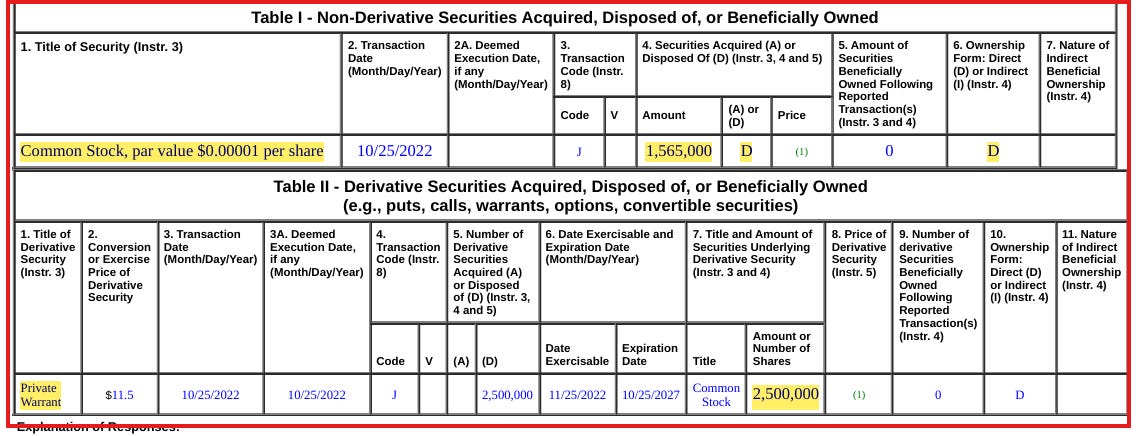

Mao appears exactly once in CDIO’s post-merger SEC filing history, in a single Form 4 filed on October 26, 2022, the day after the de-SPAC closing. On that date, Mana Capital LLC transferred its entire position (1.56 million shares and 2.5 million warrants) to Juventus LLC (the shell holder) to other undisclosed recipients at zero consideration. From that date forward, not a single identifiable successor has filed a beneficial ownership report with the SEC. Neither Mao Tong, Juventus LLC, nor any other identified recipient has appeared in any subsequent CDIO filing.

Above: Form 4 filed by Mana Capital LLC, disclosing the transfer of 1,565,000 shares and 2,500,000 warrants. The signature block identifies Tong Mao as the sole member of Juventus LLC, and Juventus LLC as the sole member of Mana Capital LLC.

Source: SEC, Form 4, Cardio Diagnostics Holdings, Inc., October 26, 2022

For a transfer of this size, moving to unidentified recipients on the day of closing, the complete absence of disclosure is not a lack of oversight. It is a premeditated structure, one that raises the following questions: who ultimately received those shares, where are these recipients located, and how much did they benefit from them?

2. The Bottom of the Barrel Candidate

According to the S-4 registration statement filed in connection with the merger, MAAQ reviewed more than 20 potential candidates for a business combination before settling with CDIO. The documented failures show a range of candidates from a pharma company, a beverage distributor, an electric vehicle charging company, and a real estate developer. Highlighting that the main SPAC did not have a true strategy or a legitimate business aim for acquisition, but rather they were window shopping for a company in which MAAQ was the main beneficiary, and a structure in which they could take advantage of the dire business conditions.

Above: MAAQ process of candidate review, highlighting 20 potential business candidates and choosing Cardio Diagnostics as the only available alternative.

Source: Form S-4 MAAQ/Cardio Diagnostics, Inc. Merger October 7, 2022

When MAAQ approached Cardio, Cardio itself had already been through a failed merger of its own. Jonathan Intrater was first contacted about Cardio on April 8, 2022. Nine days later, and after 2 deadline extensions in which MAAQ already paid more than +$200k for each, MAAQ and Cardio reached a preliminary agreement. At that moment, Cardio Diagnostics had generated $901 in total lifetime revenue. The merger was closed six months later, but the final candidate was Cardio, not a disruptive healthcare innovator, not a proven technology platform, but a development-stage company with less revenue than a lemonade stand.

Above: Cardio Diagnostics lifetime revenue before de-SPAC.

Source: Form S-4 MAAQ/Cardio Diagnostics, Inc. Merger October 7, 2022

3. The Fragility of the Business Revenue

Cardio Diagnostics promotes two primary products:

Epi+Gen CHD – a blood test designed to detect coronary heart disease

PrecisionCHD – a test intended to predict future cardiovascular risk

The company frequently highlights the enormous global market for cardiovascular diagnostics, and its main flagship products are both the Epi+Gen and the Precision CHD tests; however, the reality of the business is stark.

Since fiscal year 2023, revenue has totaled $63k, or roughly $20k per year, which is less than the company spent on computer equipment in 2025.

Source: CDIO Form 10-Q quarterly period ended September 30, 2025

Source: CDIO Form 10-K annual period ended December 31, 2024

At this stage, it is difficult to characterize CDIO as a commercial diagnostics company at all; instead, it looks more like a development-stage concept that happens to trade publicly.

4. Selling Stock as their true business model

The company’s survival has depended overwhelmingly on selling stock. In 2024 alone, Cardio Diagnostics raised approximately $12.5 million through common stock and warrant sales.

Source: CDIO Form 10-K annual period ended December 31, 2024

During the first nine months of 2025, it raised another $3.5 million through the sale of stock and common warrants, while the revenue for the same time period amounted to just at $11.3k, this extreme ratio disparity means that all 99.7% of the company’s cash flow for the period was from the proceeds of equity sales, and not from operations.

Source: CDIO Form 10-Q quarterly period ended September 30, 2025

In practical terms, this dynamic is typical in microcaps where the business model relies heavily on equity financing rather than commercial revenue.

Like many companies that came public through the SPAC boom, CDIO also carries a complex capital table, including warrants, stock options, and convertibles. While many of these securities currently sit far out of the money due to the reverse split, the broader structure reflects a company that has repeatedly relied on equity markets to finance operations.

However, the more immediate dilution risk comes from the company’s at-the-market (ATM) facility, which allows it to continuously sell newly issued shares into the public market during periods when the stock price is strong.

The Total ATM capacity was registered for $9.48 million, as of March 2026, $5,861,554 are still available for sale. This is particularly concerning given the company’s extremely small size. As of today, CDIO’s entire market capitalization is roughly $9 million, which means the company still has the legal ability to issue stock equivalent to nearly its entire market value, which represents a potentially enormous dilution overhang for shareholders.

5. Reverse Split Signals Structural Fragility

In June 2024, CDIO received a written notice from Nasdaq, indicating that the Company was no longer in compliance because the minimum bid price of the Company’s common stock had been below $1.00 per share for 30 consecutive business days.

CDIO was granted in December 2024, a 180-day extension to comply with such a requirement, it would face delisting. In June 2025, the company executed a 1-for-30 reverse stock split.

Source: CDIO Form 8-K SEC Notice of Delisting June 7, 2024

The stated purpose was solely to regain compliance with Nasdaq’s minimum bid price rule, zero value generated, and just price mechanics to hit a price target. In reality, especially in the small-cap universe, reverse splits do not create value; they are typically the result of prolonged share price declines and listing pressure.

Before the split, CDIO had around 50 million shares outstanding. The split simply consolidated those shares into approximately 1.6 million shares while leaving the underlying economics unchanged

Reverse splits in small caps often precede additional dilution cycles, as companies attempt to maintain listing status while continuing to raise capital.

Source: CDIO Form 10-K annual period ended December 31, 2024

6. The Conference Call Catalyst

The recent surge in CDIO’s share price appears to have been driven largely by the company’s investor conference call. On February 19, 2026, CDIO filed a Form 8-K, attaching a 26-slide investor presentation used in connection with a live conference call held the same day.

In the 8 consecutive trading days from the conference call, CDIO’s share price rose from $1.19 to $6.55, a 450% increase.

During the call, management discussed strategy and future opportunities, but the event did not coincide with any meaningful change in the company’s financial position. The presentation contained no revenue guidance; the company explicitly stated that it was making no projections and providing no guidance regarding its future financial condition.

Source: CDIO Form 8-K Exhibit 99.1 Investor Presentation dated February 19, 2026

Most of the content in the presentation consisted largely of publicly available information, like cardiovascular disease statistics, CDC data, World Health Organization studies, and studies from the American Heart Association. No proven revenue data was truly discussed, and no new breakthrough technology was presented.

Revenue remains minimal, and the underlying business has not materially changed. In small, low-float microcaps like CDIO, investor calls and promotional updates can sometimes trigger sharp price moves even when fundamentals remain largely the same.

7. A Narrative that Far Exceeds the Harsh Reality

The main narrative built around CDIO revolves around AI-driven diagnostics, epigenetic biomarkers, a massive cardiovascular disease market, and insurance reimbursement pathways; this is pure wishful thinking, as the numbers show a company that has yet to demonstrate even minimal commercial traction.

At present, the company’s revenue remains extremely small relative to its operating expenses. Quarterly filings year over year show only a few thousand dollars of revenue and continued multi-million dollar losses. For a company that is currently trading largely on future expectations and promotional press releases, operational results will continue to erode shareholders’ confidence.

At present, the gap between the promotional narrative and the company’s operating results is enormous. CDIO may describe itself as a next-generation precision diagnostics company, but in reality, it is a company that sells equity to fund operations and management expenses.

The following map serves as a warning sign for investors to recognize the pattern of a death spiral before the final stages of delisting and total loss occur. In this case, it is our opinion based on due diligence and analysis that CDIO’s current phase is phase #5, in which the pump already occurred, and it is now heading into downward acceleration.

Final Conclusion

Cardio Diagnostics presents itself as a company operating at the intersection of AI, genomics, and cardiovascular medicine. The financial results, the capital structure, and the ownership record tell a very different story.

Revenue remains minimal and declining. In the nine months ended September 30, 2025, the company generated $11,270 in total revenue while losing $5.03 million — a margin of negative 44,500%. Losses continue to accumulate against an $27.8 million deficit. The company has raised more than $15 million in equity capital since inception, while generating approximately $65,000 in cumulative revenue. By any commercial standard, the business has not demonstrated viability.

At the same time, CDIO trades with all the characteristics of a speculative low-float microcap — capable of dramatic short-term price spikes but highly dependent on trading momentum rather than business performance.

The structural questions raised in this report remain unanswered. On October 26, 2022, the day after the de-SPAC closing, Mana Capital LLC transferred 1,565,000 shares and 2,500,000 warrants to Juventus LLC and other undisclosed recipients. From that date forward, not a single identifiable successor has filed a beneficial ownership report with the SEC. The ultimate holders of those securities, their location, and the extent of any benefit they have derived from the subsequent trading activity in CDIO shares remain unknown. For a transfer of this size, executed on the day of closing, that absence of disclosure is not an administrative oversight. It is a structural choice and it remains unresolved.

Until Cardio Diagnostics demonstrates meaningful commercial adoption, the company appears far more dependent on capital markets than on the underlying success of its products.

For investors, the question is not whether cardiovascular diagnostics represents a large market opportunity. The question is whether CDIO can build a viable business before continued dilution erodes shareholder value. Based on the company’s financial history and operating results to date, that outcome appears highly unlikely.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions—long, short, or otherwise—in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.