$CAST: A Streaming Illusion Hiding a Financial Nightmare

How a Self-serving CEO turned the company into his personal cash cow

Executive Summary

FreeCast, Inc. has become another speculative microcap momentum vehicle whose stock price has detached from the business’s financial reality. On paper, the company wants to project an image to investors and present itself as looking to the future of streaming. The company talks about streaming aggregation, advertising technology, telecom partnerships, sports distribution, platform services, and a massive addressable market. On paper, it sounds like a company operating at a massive scale, a “massive” scale that translates to $600k of revenue a year in a highly competitive sector in which the company provides absolutely NO moat, NO differential factor, and NO advantage over its competitors.

CAST recently traded between approximately $0.64 and an intraday high of $12.20 over just a few trading days. At that high, the market briefly valued FreeCast at several hundred million dollars. With the entire market suddenly obsessed with SpaceX and Starlink, FreeCast became one of the first companies to capitalize on the frenzy. A June 18th press release referencing Starlink was enough to ignite a speculative frenzy; the same day, more than 100 million shares changed hands as the stock doubled.

Buried beneath the headlines sits a detail many investors probably never considered. Unlike a traditional IPO, FreeCast entered Nasdaq through a direct listing, a structure that creates ZERO lockup periods, allowing for immediate liquidity and dilution for existing shareholders, while bringing no meaningful operating capital into the business itself. Whilst traders chased headlines, FreeCast continued operating with just $119,302 of cash, over $10 million in cumulative losses, and a $50 million equity facility quietly waiting in the background.

The complete filings tell the whole story, for the latest quarter ending March 31st, 2026, FreeCast generated just $92,909 in revenue while losing more than $4.5 million. That’s nearly $49 lost for every dollar brought in. Its latest nine-month revenue totaled just $350,859, which is less than the annual sales of your favorite local restaurant. FreeCast’s recent SEC filings flag “substantial doubt” about the company’s ability to continue as a going concern, given minimal cash, recurring losses, and dependence on new capital raises.

We believe the market is currently valuing potential headlines and trading mechanics, while being completely disconnected from fundamentals. The filings show something very different: a capital-starved company that has relied on related-party funding, converted debt, preferred stock, warrant amendments, and an equity purchase agreement to keep the story alive and maintain market access. CAST is streaming a dream, the filings are streaming reality. We view CAST shares as extremely overvalued and fundamentally of ZERO value.

Fugazi Research Analysis

FreeCast trades at a 579x P/S ratio, that’s a multiple you’d expect to see on a company doubling revenue every quarter with a clear path to dominating its category, not one whose revenue just fell 15% year-over-year, whose own filings carry a going-concern qualification, and whose cash balance wouldn’t cover a week of payroll without the CEO writing himself another check. Strip away the Starlink headline, and the market is paying $579 for every $1 of sales in a company that’s never once turned a profit.

The Starlink Business agreement itself (the reason why the stock started trading higher), per available disclosure, is a non-exclusive reseller arrangement with no disclosed minimum purchase commitment, contract value, or revenue target. Despite the market reaction, it was a transformative catalyst for a company that had disclosed substantial doubt about its ability to continue operating for the next 12 months.

FreeCast’s continued operation is financed almost entirely by its own controlling shareholder. CEO William Mobley and his majority-owned entity, Nextelligence, supplied the substantial majority of the company’s external financing over the trailing nine months via a revolving convertible note.

The terms of the insider financing moved in the lender’s own favor immediately after quarter-end. The Nextelligence revolving note converted from a fixed $8.00 conversion price to a floating price tied to the prior day’s closing price, and Nextelligence began converting at that lower, self-set price within days of the change, a related party renegotiating the terms of its own debt, in its own favor, with itself effectively on both sides of the transaction.

A $120,000,000 liquidation preference sits ahead of all common stockholders via the Series A Preferred Stock, held by Nextelligence. The preference is explicitly benefiting Nextligence, meaning Mobley’s holding company would be paid out ahead of public Class A and Class B holders in the event of an acquisition.

Voting control is structurally locked to one person, as Class B common stock carries 15 votes per share and, by the company’s articles of incorporation, can only be issued to or held by CEO Mobley. That structure alone delivers roughly 88% of total voting power to the CEO, independent of his economic ownership stake.

FreeCast’s “revenue” isn’t really revenue from customers; it’s Mobley billing himself. Celebrity Cigars, where he’s the sole director and his son works, accounted for over a third of quarterly sales. When Celebrity Cigars and Test Drive Live couldn’t cover what they owed FreeCast, Nextelligence (Mobley’s other company) quietly paid it off for them, then booked the payoff as a brand-new loan FreeCast now owes back to Nextelligence. So the CEO’s holding company pays his other companies’ bills to a third company he also controls, and FreeCast comes out the other end deeper in debt to him for the favor, a blatant circular money play.

The $50,000,000 equity line of credit, priced at 95% of five-day VWAP, became drawable on May 6, 2026, just ahead of a string of promotional announcements (an expanded DIRECTV partnership on June 11, a Starlink Business reseller agreement on June 18) that drove the stock up sharply on thin disclosed deal economics.

Investor appetite for FreeCast stock, even on insider-favorable terms, has recently proven to be extremely thin. When the board repriced 6.7 million warrants to a deep in-the-money strike just weeks before the Starlink rally, the overwhelming majority still expired unexercised, a real-world demand test that the subsequent narrative-driven spike doesn’t appear consistent with.

Freecast is a balance-sheet-insolvent company kept alive almost entirely by its own CEO’s debt, voting-controlled by that same CEO at a structural 88%, with $120 million of insider preferred stock standing ahead of every public shareholder in any exit. The Starlink and DIRECTV headlines didn’t change the balance sheet; they are mere PR’s manufactured to lure hype shareholders into buying a stock with no fundamental value. For this reason, Fugazi Research considers Freecast uninvestable at any price above ZERO.

Financial Summary

Cash of $119,302 against nine-month cash used in operating activities of $8,083,926 (average $898,214 per month), implies less than a week of cash runway at the current burn rate, absent additional financing.

FreeCast trades at a price-to-sales ratio of approximately 579x. For context, software companies with sustained revenue growth and expanding margins rarely sustain multiples above 30x.

Working capital deficit of $7,285,937 (current assets of $622,847 against current liabilities of $7,908,784).

Of $7,670,043 raised through financing activities in the nine months ended March 31, 2026, $4,970,043 (64.8%) was sourced from CEO William Mobley or his controlled entity, Nextelligence; $2,700,000 (35.2%) came from third-party Class A stock purchases.

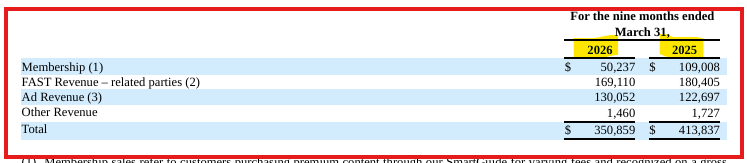

Nine-month revenue declined 15.2% year-over-year, from $413,837 to $350,859; subscription revenue declined 54% over the same period.

With a nine-month net loss of $10,180,305 against total revenue of $350,859, the company lost $29 for every $1.00 it earned.

Accumulated deficit of $205,415,506 exceeds total additional paid-in capital of $198,414,784 by $7,000,722 (103.5% of all capital ever raised by the company has been lost.)

Revenue per subscriber, excluding FAST and ad revenue, declined from $0.12 to $0.05 over the trailing nine months (a 58.3% decrease).

Interest expense of $194,969 for the nine months equals 55.6% of total revenue (up 23.8% year-over-year), driven entirely by interest accruing on debt owed to the CEO’s own entity

The company issued 6,743,587 warrants to 137 accredited investors at $4.25 per share. When 96.3% expired unexercised, the board repriced the strike to $1.33 and extended the deadline. After the reprice, 96.3% still expired unexercised. Two investors exercised, generating $332,500 in proceeds.

Source: FreeCast, Inc. Form 10-Q, quarterly period ended March 31, 2026. Filed May 15, 2026.

Source: FreeCast Inc. Form 8-K, filed May 28, 2026.

The Unsubstantial Starlink “Reseller” Agreement

On June 18, 2026, FreeCast issued a press release announcing a reseller agreement, which is actually more like a third-party affiliate for Starlink Business services (It’s the equivalent of a small travel agency getting approved to book Delta flights), sending CAST shares up as much as 170% intraday on volume of approximately 61 million shares. The entire document contains no disclosed contract value, no minimum purchase commitment, no exclusivity provision, no revenue target, and no signed customer. What it does contain is eleven bullet points of markets FreeCast “intends to target,” eleven bullet points of solutions customers “may gain access to,” and eleven bullet points of revenue streams the combined offering “may enable.”

When our team signed up for a FreeCast profile, the emails went directly to spam, and it’s unclear how to sign up for their services. If someone wanted to get Starlink, why would they choose FreeCast as their source? Nothing on their website insinuates that anyone can order StarLink services.

Additionally, SpaceX/Starlink has not announced anything whatsoever about FreeCast being affiliated with them. No binding commitment from SpaceX to FreeCast beyond reseller status is disclosed. Starlink Business reseller agreements are available to qualifying commercial partners on a broad basis; this is not a joint venture, a technology integration, or an exclusive distribution arrangement. It is permission to resell a third-party product. FreeCast is just using this non-event to spark hype on the stock price. This contributed to the company’s market cap surpassing $400 million at its current peak, which will inevitably come crashing down once reality sets in.

The $400 million Disconnect

On June 18, 2026, FreeCast’s implied market capitalization crossed $400 million on the back of the hype-ridden Starlink reseller press release. To understand how disconnected that number is from the underlying business, consider what $400 million is actually being assigned to.

Above: The corporate headquarters of a $400 million “industry innovator,” looking more like an executive office on the back of your local Best Western.

FreeCast’s total assets as of March 31, 2026, were $1,121,579. Its cash position was $119,302. Its accumulated deficit was $205,415,506. The company’s own auditors filed a going concern qualification before the stock moved. At the peak intraday price, the market was valuing FreeCast at roughly 356 times its total assets, and approximately 3,367 times its cash on hand, an insane disconnection from its true valuation, which only highlighted that the price was running on fumes.

There is exactly one analyst covering CAST. That analyst is Maxim Group’s Allen Klee, who maintained a Buy rating with a $6.00 price target in May 2026. Notably, Maxim Partners received 125,000 shares of FreeCast Class A common stock, valued at $1,000,000, as compensation for advising on the company’s direct listing.

The Direct Listing Did Not Fix the Balance Sheet

FreeCast’s March 2026 Nasdaq listing was not a traditional IPO; it was a direct listing. Investopedia points out that “Companies choose a direct listing over a traditional IPO to mostly avoid hefty underwriter fees and bypass 180-day insider lock-up restrictions.”

This is important to note because Nextelligence Inc. owns over 25 million of the 41.5 million outstanding shares. Because the company is a direct listing as of March 10th, 2026, Nextelligence Inc. has no lockup restrictions and could dump its shares at any time. If CAST were a traditional IPO, there would be a 180-day lockup at a minimum, and the supply could not dump before then. In this situation, with CAST being a direct-listing stock, the 25 million Nextelligence Inc. shares could be dumped at any time. (Mobley sold 87,500 shares at $4/share; 200,000 shares at $6/share; and 218,750 shares at $8/share).

Source: AskEdgar CAST dilution tab

In a typical IPO, a company sells newly issued shares and raises cash. In FreeCast’s direct listing, the prospectus registered shares for resale by existing shareholders. FreeCast stated that it would not receive proceeds from the sale of shares by registered shareholders.

This is critical because FreeCast entered the public market with an already-stressed balance sheet. The company had only $433,363 of cash as of December 31, 2025. It had $4.8 million of total liabilities. It had an accumulated deficit of $200.9 million. Its own filings raised substantial doubt about its ability to continue as a going concern.

The latest Form 10-Q shows that the balance sheet stress did not improve after the listing. As of March 31, 2026, FreeCast had only $119,302 of cash, $8.12 million of total liabilities, a $205.4 million accumulated deficit, and a $6.99 million stockholders’ deficit.

A direct listing creates public trading, but it does not automatically create operating liquidity. Most of the public is unaware of the toxic nature of CAST’s direct listing. Most retail investors and traders do not even know the difference between an IPO and a direct listing. As CAST is trading over 3000% from its initial runup from .50, most traders and investors caught up in the hype, sounding press releases about StarkLink, etc., do not even know that a massive amount of shares can be dumped on them at any moment since CAST is a direct listing stock with no lockups. Investors may be treating CAST as if a Nasdaq listing itself validates the business, which it does not. The Nasdaq listing status provides the company with a public currency, increases trading visibility, and may help it access capital. However, the underlying financial condition remains unchanged unless capital is actually raised.

FreeCast’s direct listing appears to have done two things particularly well. First, it created a public trading vehicle. Second, it provided existing holders with a path to liquidity. It did not meaningfully change the company’s operating economics, which is important to note after a parabolic move in a stock’s price. A company with minimal revenue, limited cash, and a newly created public market can see violent price swings. However, volatility does not equal fundamental value.

Related-Party Transactions Are Central to the Story

FreeCast’s related-party arrangements are not incidental to the business. They are the business. The company’s core technology, its primary financing, and a material portion of its reported revenue all flow through entities owned or controlled by the same person: William A. Mobley, Jr., FreeCast’s founder, CEO, Chairman, and the beneficial owner of 93.1% of the company’s outstanding shares.

Nextelligence (corporation wholly owned and controlled by Mobley) holds the revolving convertible promissory note (bearing 12% annual interest, convertible into Class A shares at Nextelligence’s sole discretion) that has functioned as FreeCast’s primary and only lifeline. Mobley, through Nextelligence, lends money to FreeCast at 12% interest. When the stock rises, whether from a Starlink press release, a DIRECTV announcement, or any other catalyst, Nextelligence can convert debt into equity at or near the elevated price, receiving shares worth more than the debt extinguished. Those shares, once issued, can be sold into the market.

Mobley benefits as a lender through interest accrual, as a converter through share issuance at favorable prices, and as a majority shareholder through any valuation narrative that supports a higher stock price. All while eliminating all checks and balances to the transaction, as he controls the entire structure through 93.1% beneficial ownership of a company whose board cannot meaningfully check any transaction he proposes, because he controls the votes required to approve it.

Calling it what it is, Mobley built a company, made himself the landlord, the banker, and the majority shareholder all at once, and then started charging his own company 12% interest to stay alive. Every dollar FreeCast borrows from Nextelligence puts money in Mobley’s pocket twice… once as interest while the debt sits on the books, and again when he converts that same debt into shares at whatever price he negotiates with himself.

The Revenue Base Is Almost Nonexistent

FreeCast’s business description reads like a company operating across every large addressable market simultaneously (streaming aggregation, advertising technology, FAST channels, telecom partnerships, broadband operators, multifamily housing, and sports distribution). In reality, the company’s whole business model is hanging for on dear life.

For the three months ended December 31, 2025, FreeCast reported total revenue of $62,090. For the six months ended December 31, 2025, total revenue was $257,950. That is the entire commercial output of a company that was briefly valued at over $400 million by the market. But the story doesn’t end there, the company is currently on a spiral of shrinking subscription revenue, in all of its fronts. Subscription revenue declined 51% for the six-month period, FAST revenue declined 29%, and Ad Revenue declined.

Above: Revenue recognition disclosing shrinking numbers in all fronts.

If FreeCast were a private company approaching institutional investors with these metrics, it would not be discussing a $400 million valuation. It would be discussing survival terms, conversion discounts, and whether the existing capital structure could be restructured into something a rational investor would touch. However, in the public market, momentum traders briefly assigned it disproportionate valuation on the back of press releases with no disclosed contract value, no minimum commitments, and no signed customers, something worth of a company which thatdefinitely crash when fundamentals arrive.

The Controlled-Company Structure Weakens Minority Shareholder Protection

FreeCast has two classes of common stock. Class A common stock carries one vote per share. Class B common stock carries 15 votes per share. Class B shares may only be issued to and held by William A. Mobley, Jr. and certain permitted entities owned and controlled by him.

The company also disclosed that it qualifies as a controlled company under Nasdaq rules because William Mobley holds a majority of the combined voting power. Controlled-company status allows FreeCast to rely on exemptions from certain Nasdaq corporate governance requirements. Public shareholders buying Class A stock after a speculative run may have economic exposure, but they do not have meaningful governance influence. In practice, FreeCast remains under the control of its founder.

Controlled-company structures are not inherently improper. Many large companies have dual-class stock. But when combined with related-party transactions, going-concern language, minimal revenue, and a parabolic move in a microcap stock, we believe the governance structure warrants greater scrutiny.

Investors are not buying a clean, institutionally governed public company with a long operating history and mature financial controls. They are buying a newly publicly controlled company in which the founder’s voting power, related-party financing, and technology relationships are central to the story.

The $50 Million Equity Purchase Agreement Is the Real Financing Backstop

FreeCast entered into an equity purchase agreement with Amiens Technology Investments, LLC in December 2025. Under the agreement, FreeCast has the right to sell up to $50 million of Class A common stock over a period of up to 36 months following the direct listing. This is the financing machine investors should focus on.

CAST’s filings state that the company entered into the equity purchase agreement to provide a flexible source of potential liquidity. The company also disclosed that issuances under the agreement may result in substantial dilution, and the investor resales may cause the stock price to decline. This is exactly the risk.

The company has a going-concern warning. The company has minimal cash and has large operating losses relative to revenue. They’ve stated that they expect to seek additional funding through debt or equity financing.

The equity line provides a potential path to raise cash, but not without dilution. This is why the stock’s recent run is so important- the rising share price can make equity financing more attractive. It can also create the conditions for the company to issue stock into the market liquidity.

The existence of the equity line is significant because the company’s financial condition makes future equity highly plausible. The real risk for retail investors chasing the move is that today’s momentum can easily become tomorrow’s exit liquidity.

The Warrant Amendment Was Not a Sign of Strength

In April 2026, FreeCast issued warrants to 137 accredited investors to purchase up to 6,743,587 Class A shares at $4.25 per share. In May 2026, the board amended the warrants by reducing the exercise price to $1.33 per share and extending the expiration date.

Only two investors exercised, and FreeCast issued 250,000 shares, receiving $332,500 of proceeds. The remaining 6,493,587 warrant shares expired unexercised and returned to authorized but unissued status. Some investors may have interpreted the expiration of warrants as a positive because it removed a near-term overhang. We believe that misses the more important point, which is broken down as follows:

The company lowered the exercise price from $4.25 to $1.33 to encourage exercise, yet only a tiny portion of the potential warrant shares were exercised. That suggests limited willingness among warrant holders to put additional capital into the company, even at the reduced price.

The expiration of warrants may reduce one specific near-term source of dilution. However, it does not solve the company’s capital problem. FreeCast still has a going concern warning, minimal revenue, and an equity purchase agreement, with a constant need for capital.

We believe the warrant amendment should be viewed as evidence of funding stress, not evidence of financial strength.

The DIRECTV and FPUnet Headlines Sound Larger Than the Filings

FreeCast’s recent news cycle included agreements with DIRECTV Multifamily and FPUnet Communications to make CAST’s platform available to more than 30,000 homes in the Fort Pierce region.

The DIRECTV announcement states that FreeCast is authorized to market and sell DIRECTV streaming services in multifamily housing. No financial terms were disclosed. The FPUnet announcement describes FreeCast’s platform being made “available” to subscribers across a service footprint. The reported economics are not visible in the filings.

These announcements sound commercially relevant, but investors should distinguish between the ability to offer service and actual reported revenue. A distribution agreement is not synonymous with high-margin recurring revenue. A platform simply being made available is not the same as real consumer adoption.

We believe these types of announcements are useful for momentum, but insufficient for valuation. The stock market may reward headlines in the short term. Eventually, the numbers have to show up.

CAST has yet to show that these announcements are translating into meaningful revenue.

The Regional Sports Narrative Looks Like Another Story: Searching for a Business

One of FreeCast’s latest pitches to investors is its Regional Streaming Sports Channel initiative, an effort to position the company as a solution for the ongoing collapse of traditional regional sports networks.

At first glance, the story sounds compelling. Regional sports networks are under pressure. Teams are searching for new distribution models. Consumers are increasingly moving away from cable bundles. Those trends are real.

The problem is that FreeCast appears to be marketing itself as a participant in a market it has not yet demonstrated any meaningful ability to penetrate.

Sports distribution is not a business that rewards ambition alone. It requires rights agreements, production infrastructure, distribution scale, advertiser relationships, customer acquisition, and most importantly, capital. Lots of it. Sports media is one of the most competitive and expensive industries in the world, attracting competition from billion-dollar broadcasters, technology giants, streaming platforms, and telecommunications companies.

FreeCast generated just $350,859 of revenue during the first nine months of fiscal 2026. That figure is difficult to reconcile with management’s apparent desire to become a meaningful player in the sports media ecosystem.

The company frequently speaks about opportunities, partnerships, markets, and future potential. What remains notably absent are signed rights agreements, meaningful recurring revenue, or any evidence that sports organizations are choosing FreeCast over larger, better-capitalized competitors.

Investors should remember that there is a significant difference between identifying an industry trend and building a business capable of monetizing it. Every struggling microcap eventually finds a large narrative to latch onto. Artificial intelligence. Crypto. Space. Quantum computing. Streaming. Sports. The theme itself may be legitimate, but that does not mean the company promoting it has earned a place within it.

From our perspective, FreeCast’s sports initiative looks less like a business segment and more like another attempt to attach the company to an attractive headline. Until investors see actual economics, actual contracts, and actual revenue, we believe the regional sports narrative belongs in the same category as the rest of FreeCast’s promotional material: ambitious, speculative, and unsupported by the company’s financial reality.

The Series A Preferred Stock Creates Another Layer Above Common Equity

FreeCast has 4,000,000 shares of Series A Preferred Stock outstanding. The Series A Preferred has no voting or conversion rights, but it carries economic preferences that common shareholders should understand. If the company generates more than $50 million of revenue in a fiscal year, the Series A holder is entitled to receive an annual cash dividend equal to 10% of revenue above $50 million until aggregate dividend payments reach a maximum threshold. The Series A Preferred also has a liquidation preference of $30 per share.

The company disclosed that Nextelligence forfeited and canceled 20,000,000 Class A shares in exchange for 4,000,000 Series A Preferred shares. This structure is important because common stock investors are not the only economic claimants on future upside. This upside is most likely nothing but a pipe dream, and if FreeCast does not achieve that scale, common shareholders are still exposed to dilution, operating losses, and financing risk.

In other words, public common shareholders appear to face the downside of the current funding needs while insiders and related parties retain significant structural claims.

The Valuation Requires a Business That Does Not Yet Exist

When CAST opened up at $12.20 per share on 6/18/2026, it briefly traded as if FreeCast were already a meaningful public streaming technology company. Hours before the open, the company issued a press release about its Starlink reseller deal, sending its shares up as high as $16.20 in the premarket. The stock began to sell off right at the open, indicating the Starlink news was more of a sell-the-news, liquidity event, highly likely marking the beginning of the end to the big run-up from $.50 to $16.20.

Since CAST is a direct-listing stock, Nextelligence Inc., which owns 25 million shares, could begin dumping as much of its position as it would like, since it has no lockups preventing it from waiting the usual 180 days. The volume of Starlink news likely triggered a liquidity event, with more selling imminent.

The filings reveal what this company really is: A massive opportunity and vehicle for insiders to get rich. FreeCast’s latest six-month revenue was $257,950. Its latest six-month operating loss was $5.6 million. Its cash was $433,363. Its accumulated deficit was $200.9 million. Its stockholders’ deficit was $3.5 million.

To justify even a fraction of the recent valuation, FreeCast must rapidly convert partnerships and platform announcements into material revenue. It must stabilize advertising monetization. It must fund operations without crushing dilution. It must prove that related-party revenue is not masking weak third-party demand. It must scale into markets where far larger companies are already competing.

The bullish case requires several things to go right at once. The bearish case requires only that the filings continue to matter.

We believe the most likely path is continued dilution, continued volatility, and eventual repricing toward a valuation that reflects the company’s actual revenue base and financing needs.

Conclusion

FreeCast’s recent rally has created the appearance of a rapidly emerging streaming technology company. The filings tell a very different story. Beneath the Starlink headlines, DIRECTV announcements, regional sports ambitions, and broadband partnerships sits a company that generated just $350,859 of revenue over the last nine months while losing more than $10 million. The company ended the latest quarter with only $119,302 of cash, a working capital deficit exceeding $7 million, and auditors expressing substantial doubt about its ability to continue as a going concern. Despite briefly achieving a market capitalization exceeding $400 million, FreeCast has yet to demonstrate meaningful commercial adoption, meaningful operating scale, or any credible path to profitability.

What makes FreeCast particularly concerning is that nearly every road eventually leads back to William Mobley. The company’s primary lender is Mobley through Nextelligence. The preferred stockholder ahead of common shareholders is Mobley through Nextelligence. The controlling shareholder is Mobley. Mobley controls approximately 88% of the voting power. A material portion of reported revenue is tied to entities controlled by Mobley. Even the technology underpinning the business originates from an entity controlled by Mobley. Public shareholders are not investing alongside an aligned founder whose interests rise and fall with theirs. They are investing beneath a structure in which one individual appears positioned to benefit, regardless of whether common shareholders ever realize a return.

As the stock price rises, that structure becomes even more advantageous for insiders. Debt can be converted into equity. Equity can be sold into market enthusiasm. The company has access to a $50 million equity facility. Nextelligence faces no traditional IPO lockup restrictions. Mobley himself faces no traditional IPO lockup restrictions. Unlike public shareholders, who buy into the narrative, insiders can identify rather than depend on it. The recent surge in CAST has not solved the company’s financial problems. It has simply created a more attractive environment for capital raises, debt conversions, and insider liquidity.

Investors should remember that FreeCast did not go public through a traditional IPO. It entered the market through a direct listing. The same structure that avoided underwriter fees and lockup restrictions also created an immediate path to liquidity for existing holders. While retail investors chase headlines and momentum, more than 25 million shares controlled by Nextelligence remain eligible for sale. The company itself continues to require financing. The equity line remains available. The need for capital has not disappeared simply because the stock price moved higher.

The Starlink reseller agreement did not solve the revenue problem. The DIRECTV partnership did not solve the revenue problem. The sports streaming narrative did not solve the revenue problem. The balance sheet remains impaired. The company remains deeply unprofitable. The cash position remains critical. The need for additional capital remains unavoidable. What changed was not the business. What changed was the story.

Ultimately, we believe investors are assigning hundreds of millions of dollars in value to a business that has failed to prove demand, scalability, profitability, or its ability to survive without continuous access to outside financing. The market is valuing FreeCast based on what management claims the company could become, while the financial statements reveal what it actually is.

History is full of microcap companies that briefly became stories before ultimately becoming financings. Based on FreeCast’s financial condition, insider-controlled structure, dependence on external capital, and long history of value destruction, we believe the company is far more likely to continue enriching insiders than creating value for public shareholders. Fugazi Research believes CAST’s recent valuation bears no resemblance to economic reality and that the stock is fundamentally worth ZERO.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions, long, short, or otherwise, in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.

Every public company deserves to be evaluated on facts—not headlines.

This article largely repeats the claims of a short-selling research firm whose business model is to profit if a stock declines. Investors should recognize that short reports are not independent audits; they present one side of the investment thesis.

At the same time, investors should also consider the other side of the story:

FreeCast has announced strategic agreements involving DIRECTV, Starlink Business, WIRE3, and other commercial initiatives that could materially expand its platform and distribution opportunities.

The company has recently secured new capital intended to strengthen its balance sheet and fund growth initiatives.

Independent analyst coverage has included Buy ratings and price targets that differ significantly from the conclusions reached by short sellers.

Investing requires weighing both risks and opportunities. The market should debate the facts—not sensational headlines.

Read the SEC filings. Read the company’s announcements. Read the short report. Then make your own informed decision.

That’s what an efficient market is supposed to do.

Sensational headlines, and Clickbait a lot of this report has already been proven false according to the latest releases they’ve been fully funded.