$CAR (Avis Budget Group): A Prisoners' Dilemma of Two Hedge Funds

Extreme debt, a quiet concentration of control, and downside skewed toward public shareholders.

Executive Summary

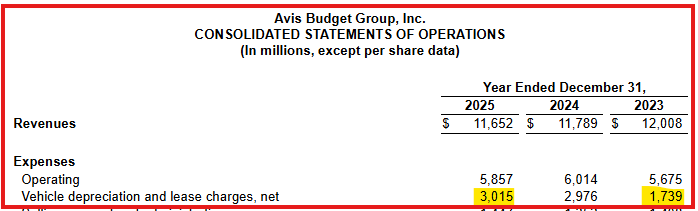

Avis Budget Group’s most recent filings show a business generating $11.65 billion in annual revenue while reporting a $889 million net loss attributable to shareholders in 2025. This all follows a $1.8 billion loss in 2024. These two years alone represent $2.71 billion in cumulative losses, occurring alongside rising interest expense, declining retained earnings, and continued balance sheet deterioration. The company now carries $25.3 billion in total indebtedness against negative stockholders’ equity of $3.1 billion, placing the capital structure in a deficit position where liabilities exceed any residual equity value. Recent price action has further demonstrated the extent to which positioning and float constraints can drive valuation independently of underlying fundamentals. The company generated only about $0.56 in operating earnings for every $1.00 of interest owed, highlighting that it no longer generates sufficient earnings to cover its interest burden.

What the numbers above fail to capture is the secondary architecture that transformed a fundamentally distressed business into the most structurally violent short squeeze since GameStop. Two institutional funds (SRS Investment Management and Pentwater Capital Management) accumulated combined economic exposure exceeding 100% of Avis Budget Group’s shares outstanding, SRS through nine years of debt-funded float engineering that installed its own partners as CEO and Executive Chairman, Pentwater through a systematic accumulation culminating in a full repositioning to unhedged long exposure in March 2026 via its Merger Arbitrage Master Fund. Together, they held the float hostage. The result was a prisoners’ dilemma that held the stock at prices six times its fundamental value until April 22, 2026, when the announcement of Q1 earnings on April 29 collapsed the remaining runway simultaneously for both funds, the leveraged long overhang liquidated in a single session, and the stock fell 40% in one day. What remains (a company with negative equity, 8x leverage, $6.8 billion in mandatory vehicle purchases due in twelve months, and a Moody’s downgrade window opening in August 2026) must now be priced on fundamentals alone.

Capital Structure and Financing Risk:

The company’s capital allocation over the past decade shows a sustained pattern of balance-sheet contraction through share repurchases, funded in part by debt issuance. Avis deployed approximately $10.75 billion into share buybacks, including $3.3 billion in 2022 alone, while simultaneously increasing corporate debt to $6.1 billion.

These transactions reduced stockholders’ equity while introducing fixed obligations that the business no longer has the earnings capacity to support.

The May 2025 issuance of $600 million in 8.375% Senior Notes (the highest coupon in its recent history) further increased financing costs while being used in part to refinance existing obligations rather than reduce leverage.

Earnings Quality and Metric Adjustments:

Management’s primary performance metric, adjusted EBITDA, has been redefined multiple times to exclude recurring costs. In 2024, $2.47 billion in fleet impairments were excluded, followed by an additional $518 million in 2025, alongside the introduction of new exclusion categories tied to vehicle disposal losses.

These adjustments remove material expenses that directly arise from the company’s core operating model, resulting in a performance metric that materially diverges from economic reality and does not reflect the full cost structure required to sustain the fleet.

Governance Structure and Ownership Concentration:

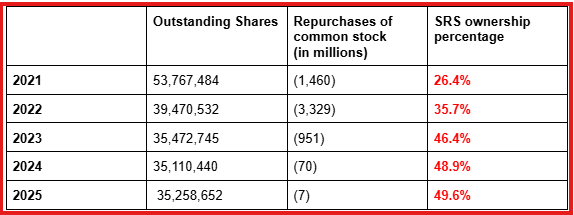

Over a multi-year period, SRS Investment Management increased its ownership position from approximately 20% to 45%, ultimately exceeding the size of the non-affiliate public float.

This increase occurred during a period in which the company executed substantial share repurchases using corporate capital

A shareholder derivative action filed against directors, officers, and a significant stockholder alleged governance failures in connection with these transactions and related disclosures.

While the case was dismissed on procedural grounds, the court acknowledged the shareholder’s influence as a governance consideration requiring oversight.

Liquidity Pressure and Structural Constraints:

The company continues to operate under fixed financial obligations that do not adjust with performance. At current levels, the business generates approximately $971 million in monthly revenue while incurring $74 million in net losses, excluding interest expense.

In addition, Avis faces $6.8 billion in mandatory vehicle purchase commitments over the next 12 months, which must be funded regardless of market conditions, residual values, or demand trends.

These obligations create a structure in which capital requirements persist even as operating performance declines.

Fugazi Research Analysis

Non-stop Losses with No End in Sight.

Avis Budget Group has reported net losses attributable to shareholders of $889 million in 2025 and $1.8 billion in 2024—two consecutive years of significant losses on a business generating $11.65 billion in annual revenue. The combined two-year loss of $2.71 billion occurred while the company paid no dividends, did not repurchase meaningful shares, and issued its most expensive debt in recent history. Those losses were driven by fleet impairments, disposal losses, and rising interest expense. In two years, the company has erased a substantial portion of its retained earnings, effectively consuming its equity base. Levi & Korsinsky, LLP is currently investigating Avis Budget Group for potential securities law violations, focusing on the gap between prior earnings expectations and the $748 million in adjusted EBITDA the company ultimately delivered. This further highlights the disconnect between reported performance and investor expectations.

Source: Avis Budget Group, Inc. Class Action Lawsuit – CAR | Levi & Korsinsky

Temporary Short Squeeze with Potential for Catastrophic Collapse.

SRS’s endgame is not a future event. The result is a float so compressed that the price discovery mechanism is entirely broken. At recent price levels, the stock is trading at an increasingly elevated multiple of a redefined EBITDA metric that management has already missed twice, sustained not by the business, but by a lack of available shares to allow the price to correct. This mathematical mistake has made the temporary short squeeze artificial; the structure supporting the move is inherently unstable and susceptible to rapid reversal. The retail shareholders trading at current levels are not partners in a recovery; they are gambling on hype and providing the liquidity for a structurally constrained exit.

Hijacked Float at the Expense of Minority Shareholders.

Over the course of nine years, SRS Investment Management executed one of the more structurally efficient control acquisitions executed in public markets—without a control premium and without the investors or the market noticing. While its ownership percentage climbed from 20% to 45%, and its entire disclosed share position grew to exceed the non-affiliate public float, SRS never really had to spend meaningful capital to buy its way in. The strategy was straightforward: infiltrate the company, authorize a decade of share buybacks using the company’s own funds, observe the float decrease, and expand their share at the cost of minority shareholders. These buyback programs were not capital allocation but a blatant float hijack executed in plain sight and with the company’s approval. SRS did not end up owning Avis; they engineered Avis Budget Group’s own financial structure to make the ownership free for them.

Insider Trading Concerns Lead to Litigation.

A shareholder derivative action filed against Avis Budget Group’s directors, officers, and a large minority stockholder alleged five counts: insider trading on material non-public information about vehicle delays in 2022 and 2023, approval of share buybacks that transferred control to this shareholder, a cooperation agreement that was improperly disclosed, breach of oversight duties, and unjust enrichment. The case was dismissed in December 2025, not on the merits of any allegation, but on procedural grounds of futility. However, the presiding judge’s own opinion confirmed that SRS’s influence was a documented governance concern requiring active judicial recognition, acknowledging that Avis’s directors had taken affirmative steps to restrain it. The procedural dismissal was not an exoneration.

Equity Depleted by Inflated Debt

The $10.75 billion in share buybacks that compressed Avis Budget Group’s float and mechanically transferred effective control to SRS Investment Management were not funded by operating cash flow but were significantly funded by newly acquired debt. Records and filings show that in 2022 (the most aggressive buyback year, which totaled $3.3 billion), Avis borrowed $750 million through a new floating-rate term loan. This pattern repeats across multiple years: issue corporate debt, deploy proceeds into buybacks, watch SRS’s ownership climb, and repeat. The $6.1 billion in corporate debt on Avis’s balance sheet is related to the $10.75 billion in treasury stock that destroyed the equity base and concentrated governance in SRS’s hands. The structure of these transactions concentrated ownership, while leaving minority shareholders exposed to the leverage and financing costs that followed.

Source: CAR Form 10-K year ended December 31, 2025,

Lenders Can’t Exit and Instead Keep Increasing Debt

Corporate interest expense rose 18% in a single year to $422 million as Avis issued $600 million of 8.375% Senior Notes in May 2025 (the highest in its recent public debt history and a direct signal of deteriorating credit perception, as a percentage-point increase is now the norm year over year). The May 2025 senior notes were issued to repay the 2025 floating-rate term loan and a portion of the 2027 notes. This means that Avis is borrowing at 8.375% to retire cheaper debt and calling it refinancing. Total debt stands at $25.3 billion. The lenders repricing this credit upward while simultaneously extending it are not acting out of confidence; they are managing exposure while extracting a higher return for the risk they cannot exit.

Conveniently Left Out Details to Mislead Investors

The company’s adjusted EBITDA (the primary performance metric presented to investors) has been redefined multiple times to exclude recurring costs. In 2024, $2.47 billion in fleet impairments were excluded. In 2025, an additional $518 million in impairments was excluded, alongside a new exclusion category called “other fleet charges,” which removed $390 million of costs related to vehicle disposals from adjusted performance. A metric that requires a new exclusion category each time a recurring cost becomes too large to absorb does not reflect operating performance; it obscures it.

Source: CAR Form 10-K year ended December 31, 2025,

CAR Financial Summary

For the full year ended December 31, 2025, revenue totaled $11.65 billion, while net loss attributable to shareholders for the same period totaled $889 million, representing a -7.6% net margin.

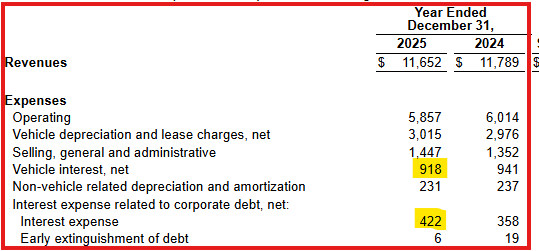

The $11.65 billion in revenue was generated against total expenses of $12.58 billion, meaning that Avis spent $1.08 for every $1.00 it collected. Vehicle depreciation and lease charges alone accounted for 25.9% of revenue, while corporate interest expense accounted for an additional 3.6%.

At current operating levels, the company generates approximately $971 million in monthly revenue while incurring $74 million in net losses. Corporate interest expense adds $35 million per month in fixed obligations that must be paid regardless of operating performance.

The company has accumulated a stockholders’ equity deficit of negative $3.1 billion, reflecting two consecutive years of nine-figure GAAP losses, compounded by $10.75 billion in treasury stock buybacks, funded primarily by debt issuances that now cost shareholders $422 million per year in interest expense.

Total indebtedness stands at $25.3 billion ($6.1 billion in corporate debt and $19.2 billion in asset-backed vehicle program debt) against a business that has not generated positive GAAP earnings in two consecutive fiscal years.

The company’s most recently issued senior notes carry a coupon of 8.375%, the highest in its recent history, and a direct market signal of deteriorating credit perception.

Two consecutive years of net losses attributable to shareholders totaling $2.71 billion occurred while the company paid no dividends and issued its most expensive debt in recent history.

Retained earnings have fallen from $3.9 billion in 2023 to $1.1 billion in 2025, a 72% erosion over 2 years. At the 2025 loss rate, the remaining retained earnings balance will be fully exhausted in just a year without a fundamental reversal in operating performance.

The Americas’ rental car industry, which accounts for 76% of Avis’s total revenue, has completely flatlined. The US political environment has pressured tourism volumes throughout 2025 and the beginning of 2026. Travel sentiment has softened amid market volatility and macroeconomic uncertainty. Tariffs on imported vehicles create direct cost pressure on the already $6.8 billion mandatory fleet repurchase commitment. This is not an industry in trend, but a normalized, low-growth, margin-compressed industry that doesn’t show signs of recovery.

As of the most recent public rating action in February 2025, Moody’s affirmed Avis Budget Group’s corporate family rating at Ba3 with a NEGATIVE outlook. Moody’s own stated downgrade triggers include debt/EBITDA sustained above 4x. With a corporate leverage currently running at approximately 8x adjusted EBITDA, Avis breaches that threshold by a factor of two. As of the date of this publication, it is confirmed that every condition Moody’s identified as a downgrade risk has materially worsened since the last public rating action.

The $25.3 billion in total indebtedness, against negative stockholders’ equity of $3.1 billion and a corporate gross debt of $6.1 billion, implies a leverage ratio of 8.1x adjusted EBITDA (more than three times the 2.5x first-lien covenant threshold that the company must not breach). The all-in coverage ratio at the current adjusted EBITDA against total corporate and vehicle interest expense of $1.34 billion annually is 0.56x, meaning the business generates 56 cents of adjusted earnings for every dollar of interest it owes. On a GAAP basis, the coverage is currently negative.

Source: CAR Form 10-K year ended December 31, 2025,

Source: MMCG Invest - “U.S. Car Rental Industry: 2025–2030 Market Analysis (Investment Perspective)

Source: Moody’s Ratings, as reported by Investing.com - “Avis ratings affirmed by Moody’s, outlook shifts to negative”

The Business Model (A Debt-Financed Cycle)

Avis Budget Group is not a traditional car rental company. It is a debt-financed asset cycle operating at an industrial scale. The model requires the company to deploy approximately $15.1 billion annually to acquire a rotating fleet of 684,000 vehicles, finance that fleet through $19.2 billion in asset-backed debt at a weighted average rate of 5.29%, generate rental revenue against that asset base, and dispose of the vehicles before depreciation destroys the residual value.

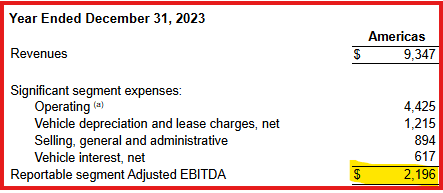

Vehicle depreciation and lease charges rose 73% in two years, from $1.739 billion in 2023 to $3.015 billion in 2025. America’s revenue per day declined 3%. America’s Adjusted EBITDA collapsed 75%, from $2.2 billion to $552 million.

The disposal losses were so large that management created an entirely new non-GAAP exclusion category, “other fleet charges,” to remove $390 million of vehicle disposal losses from the metric it asks investors to use.

The company has $6.8 billion in mandatory vehicle purchase commitments due over the next 12 months. Those commitments do not account for softer pricing, lower residual values, or a tariff environment that could make new vehicles materially pricier. The fleet must be funded regardless.

The 2021 to 2023 period produced results that made the model look structurally superior; it was nothing but an alignment of factors that allowed it to look better on the surface.

First, daily rental rates surged across the industry as fleet availability collapsed following the semiconductor shortage. With supply constrained worldwide, operators sustained elevated pricing for an extended period without meaningful competitive pushback.

Second, used vehicle prices reached historic highs. Avis was selling vehicles at a gain or with minimal depreciation, a dynamic that directly inflated reported margins and obscured the true cost structure of the fleet. In 2023, net gains on vehicle sales reached $656 million, a figure that contributed directly to that year’s $2.2 billion Americas Adjusted EBITDA.

Third, lower effective depreciation combined with elevated pricing produced return metrics that appeared to justify a structural re-rating of the business. Higher margins drove stronger cash flow, which reinforced the narrative.

But this convergence and added conditions never last. Avis Budget Group is not a distressed business waiting for a catalyst, but in reality, it is a cyclical business in the middle of a mean reversion, operating on a borderline liquidity balance sheet. The debt is still there and growing, the interest expense is still there, along with the mandatory fleet commitment. What is no longer there is the pricing power, the residual-value tailwind, and the capital efficiency that made it all look manageable.

Financing Costs are Now a Headwind

Avis’s Budget Group model is structurally inseparable from its debt. The company carries $19.2 billion in asset-backed vehicle program debt and $6.1 billion in corporate debt, a whopping $25.4 billion in total indebtedness against a business that generated negative GAAP earnings in each of the last two fiscal years.

Today, the cost of the debt is rising faster than the revenue it supports. Vehicle interest expense reached $918 million in 2025. Corporate interest expense rose 18% in a single year to $422 million. Total annual interest expense across corporate and vehicle programs stands at $1.34 billion. Against the adjusted EBITDA of $748 million, the all-in coverage ratio is 0.56x. The business generates 56 cents of adjusted earnings for every dollar of interest it owes.

The May 2025 issuance of $600 million in 8.375% Senior Notes (the highest coupon in Avis Budget Group’s recent public debt history) is a market verdict. When sophisticated institutional lenders price a company’s debt at 8.375%, they are communicating their view of the company’s credit risk.

Investment-grade BBB-rated companies were borrowing at approximately 5.0% to 5.2%. Avis paid approximately 200 to 250 basis points above the typical cost of capital for a BB-rated company, a spread that reflected not the general level of interest rates but the specific credit risk premium the market assigned to Avis at that time.

The Moody’s signal

Moody’s most recent public rating action on Avis Budget Group, taken in February 2025, affirmed the corporate family rating at Ba3 (three notches below investment grade) while simultaneously shifting the outlook from stable to negative. Moody’s explicitly published its downgrade triggers: “debt/EBITDA sustained above 4x and pre-tax income as a percentage of sales below 7.5%.”

Moody’s places follow-up actions on negative outlooks within approximately 12 to 18 months of the outlook change. The February 2025 action puts that window squarely at August 2026 to February 2027 (a period during which Avis must also refinance $645 million of 5.750% Senior Notes maturing in July 2027). Every condition Moody’s identified as a downgrade risk has materially worsened since February 2025.

Source: Moody’s Ratings, as reported by Investing.com - “Avis ratings affirmed by Moody’s, outlook shifts to negative”

SRS eats the Float

What appears to be a publicly traded company with 35.26 million shares outstanding is, in practice, a privately controlled enterprise with a publicly listed minority stub.

SRS Investment Management first appeared in Avis Budget Group’s shareholder register around 2010. By 2013, the company launched a share repurchase program. The sequence that followed was craftfully designed. Each buyback reduced the outstanding float; each float reduction increased SRS’s ownership percentage without SRS deploying meaningful additional capital. Each time SRS’s percentage crossed the prior threshold established in the most recent cooperation agreement, a new agreement was signed ratifying the higher number and setting a new cap.

Five agreements over nine years moved the cap from 20% to 45%. The outstanding shares went from approximately 60 million to 35.26 million.

The personnel installations ran in parallel.

In January 2016, Brian Choi (an SRS partner since October 2008) was placed on the Avis board under the first cooperation agreement.

In April 2018, Jagdeep Pahwa (President of SRS) joined the board after SRS’s attempt to nominate five directors simultaneously forced a new agreement.

In May 2020, Karthik Sarma (SRS’s founder and managing partner) joined as an independent director.

In February 2025, Brian Choi was appointed CEO.

In March 2025, Jagdeep Pahwa was elevated to the position of Executive Chairman.

Three of the most consequential positions at Avis Budget Group are held by individuals with direct or former SRS affiliation.

The buyback program funded this consolidation with corporate capital. Of the $10.75 billion in treasury stock on the balance sheet, a meaningful portion was not funded by operating cash flow but by newly issued corporate debt. In 2022, the most aggressive single-year buyback at $3.3 billion, Avis simultaneously borrowed $750 million through a new floating-rate term loan. The pattern repeated across multiple years: issue debt, repurchase shares, shrink the float, increase SRS’s ownership, and formalize each step higher through new cooperation agreements. The $6.1 billion in corporate debt, now costing approximately $422 million per year in interest expense, is not separate from the $10.75 billion in treasury stock. They are the same transaction viewed from opposite sides of the balance sheet. $10.75 billion in debt-funded buybacks concentrated ownership, while minority shareholders remain exposed to the leverage and over $400 million in annual interest costs that came with it.

Source: Fugazi Research analysis. Outstanding shares and repurchase data derived from Avis Budget Group, Inc. Definitive Proxy Statements (Form DEF 14A), fiscal years 2021 through 2025, filed with the U.S. Securities and Exchange Commission. SRS Investment Management ownership percentages were derived from Schedule 13D/A filings and DEF 14A beneficial ownership tables for the corresponding periods. All filings are available at SEC EDGAR.

SRS Investment Management has spent nine years building something that does not yet have a formal name, but its shape is unmistakable. A controlling position exceeding the entire non-affiliate public float. A board fixed at five or six members by their cooperation agreement. A transfer restriction clause ensures that any future buyer of their block must maintain the governance structure they designed, which is the organizational architecture of an owner preparing to formalize what is already functionally true: a private company in plain sight.

Ownership Concentration and the Illusion of Float

Avis’s trading behavior is shaped by a more fundamental constraint than most market participants recognize: a large portion of the company is already held in concentrated hands, and the float reported by data providers bears little resemblance to the shares actually available to trade.

Recent filings show approximately 35.3 million shares outstanding. Within that, Pentwater Capital disclosed ownership of approximately 7.8 million shares (roughly 22% of total shares outstanding). SRS Investment Management holds a disclosed direct share position of approximately 17.4 million shares, a figure that, on its own, exceeds the entire non-affiliate public float, as calculated from Avis Budget Group’s 10-K cover page disclosure.

That disclosure (the aggregate market value of common stock held by non-affiliates as of June 30, 2025, divided by the closing price of $169.050) implies a true non-affiliate float of approximately 16.76 million shares. SRS’s disclosed position alone exceeds that figure by approximately 674,000 shares. Pentwater’s 7.8 million shares represent an additional 46.7% of the same float. Between these two holders alone, identified long positions exceed the entire non-affiliate float by more than 8.5 million shares (before any other institutional holder is counted).

Market data providers, including Yahoo Finance, commonly report the public float at approximately 10 million shares. The 10-K disclosure, using the company’s own numbers at a specific date, confirms the real non-affiliate float is approximately 16.76 million, a figure that is itself already smaller than SRS’s disclosed position and already stale, having been calculated as of June 30, 2025. Any accumulation since that date, including SRS moving toward its newly ratified 45% ownership cap, has further compressed the real tradeable supply below even that figure.

This structure changes how the stock moves. When elevated short interest meets a float, this constraint (S3 Partners confirmed that less than 900,000 shares are available to borrow against 7.1 million shares short) means that buying pressure does not need to be large. It just needs to meet the liquidity constraint. When that happens, short sellers are forced to compete for a pool of shares that is functionally insufficient to absorb institutional covering at any rational price. The result is price action that becomes reflexive and disconnected from the underlying business.

However, this constraint is not permanent. On March 27, 2026, Avis established an at-the-market equity program for up to 5,000,000 shares. At recent squeeze-driven price levels, full utilization of this program would represent approximately 14% incremental share issuance and could raise over $2 billion of gross proceeds. The significance is structural: the same supply constraint that is currently amplifying prices can reverse if the company elects to issue shares into strength, introducing new liquidity directly into a market defined by its absence.

Ownership concentration explains how the stock trades at these levels. It does not explain why it should trade there. It does not explain why it should be done. If anything, it reinforces the central point of this report: structure and positioning, not sustainable earnings power, have determined recent price levels. When that structure stops tightening—when SRS reaches its 45% cap, when short covering exhausts itself, and when the float constraint that has been nine years in the making finally meets a seller of scale—price must stand on fundamentals again. And the fundamentals, as documented throughout this report, do not support current share prices.

The Prisoners’ Dilemma: Who Pulled the Pin and Why the Grenade Went Off Today

On April 22, 2026, CAR collapsed 40% in a single session, from an intraday high near $847 to a close of $443. The squeeze was not sustained solely by retail momentum or algorithmic feedback. It was sustained by a structural impossibility: two sophisticated institutional funds had independently accumulated combined economic exposure exceeding 100% of shares outstanding, with no coordination between them and no agreed exit mechanism. This created a textbook prisoners’ dilemma.

Neither fund was acting in concert. Explicit coordination between them would constitute illegal market manipulation. As a result, each operated in informational isolation regarding the other’s exit intentions. This is the precise condition that makes a prisoners’ dilemma structurally unstable: both parties have a dominant incentive to act first, but neither can observe the other’s move in real time. The prisoners’ dilemma framework was independently corroborated by two market analysts whose public commentary arrived at substantially the same structural conclusions through different investigative paths. This convergence strengthens the analytical foundation of our thesis.

The following analysis was provided to Fugazi Research by a senior options specialist and financial professional with direct experience in short-squeeze mechanics, whose public commentary on $CAR’s ownership structure and synthetic exposure has been widely circulated on financial social media. Speaking on background, the analyst provided additional technical detail that corroborated Fugazi Research’s original EDGAR-based findings through an entirely separate investigative path.

The following interview was conducted prior to the April 22, 2026, market session and prior to the Globe Newswire announcement confirming Q1 2026 earnings for April 29. All direct quotes below are drawn from the recorded interview. Where the analyst’s public statements overlap with interview content, they are noted as such. The source requested anonymity; accordingly, no identifying information is included in this supplement.

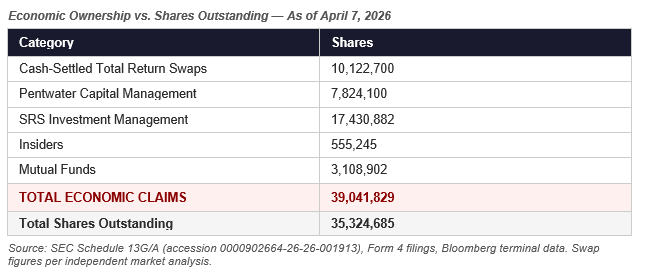

When asked to characterize the structural ownership dynamic driving the squeeze, the analyst provided a precise accounting of the combined economic exposure held by the two dominant funds. His framing centered on the distinction between common stock ownership and cash-settled total return swap exposure:

The analyst’s figure of 10,122,700 shares in cash-settled swap exposure matches the ownership decomposition table he published publicly, which showed total economic claims of 39,041,829 shares against 35,324,685 shares outstanding (a structural overhang of approximately 10.5%).

The analyst was asked directly whether the at-the-market equity facility established on March 27, 2026, represented a live relief valve for the squeeze. His response identified the MNPI constraint as the primary barrier, consistent with our analysis, though stopping short of the four additional hard stops documented in our original 424B5 forensic review.

The analyst provided important context on the official short interest data timeline, distinguishing between FINRA-reported figures and real-time estimates from data vendors. The analyst confirmed that by the time of the interview, the $CAR situation had developed a gamma squeeze component layered on top of the structural short squeeze, with options dealers acting as forced sellers due to delta hedging obligations.

The analyst was asked directly why SRS and Pentwater had not yet exited their positions, given the extraordinary price appreciation. His response identified the Section 16 insider trading constraint as a secondary barrier to exit, layered on top of the structural prisoners’ dilemma dynamic that both analysts had independently documented.

The analyst confirmed that by the time of the interview, the $CAR situation had developed a gamma squeeze component layered on top of the structural short squeeze, with options dealers acting as forced buyers through delta hedging obligations.

Valuation Ridiculous

At current price levels, Avis Budget Group trades at an implied equity valuation increasingly disconnected from its underlying earnings capacity. The business has generated negative GAAP earnings in each of the last two fiscal years, while eroding 72% of its retained earnings over the same period. This is not a case of the market discounting future growth. It is a case of price being driven by structural constraints in supply.

What is currently trading is not a valuation anchored in fundamentals, but the mechanical consequence of a compressed float interacting with elevated short interest and options-driven positioning. When a single shareholder holds a position exceeding the entire non-affiliate float, when additional large holders control a substantial portion of the remaining supply, and when borrowing availability is constrained, price becomes a function of positioning rather than earnings power.

At these levels, valuation is absurd. We do not mince words. It reflects who is forced to transact within a limited pool of shares.

What the Market Is Missing

The market is not misreading the numbers; it is misreading what created them. What looked like durable earnings power was a temporary alignment of favorable conditions, not a structural improvement. As those conditions fade, the reset is structural.

On April 21, 2026 (one day before the crash) Pentwater Capital Management LP and Matthew Halbower filed a Form 4 disclosing transactions dated April 17, 2026. The filing reveals the following:

The squeeze mechanics are not resolved. Low borrow availability and an elevated borrow rate on a 40% down day confirm that the structural supply constraint remains fully intact. What has changed is the composition of the long side (leveraged longs have been cleared, leaving only the two large structural holders and the synthetic swap exposure). The period between now and April 29 earnings represents the most information-dense window in this situation. Every EDGAR filing, every Form 4, and the April 29 shares outstanding figure will determine whether today was the end of Act One, or the intermission before a more consequential Act Two.

Conclusion

$CAR’s recent price action has already demonstrated the instability embedded in the structure. The same forces that drove the stock to extreme levels (constrained supply, forced buying, and positioning) began to reverse within a single session, producing a sharp intraday collapse from peak levels. This was not driven by a change in fundamentals, but by a shift in liquidity and positioning.

The underlying business has not changed. It remains a highly levered, cyclical model facing rising depreciation, elevated financing costs, and declining earnings power. What has changed is the structure supporting the price. As the pool of forced buyers narrows and incremental liquidity returns, the stock becomes increasingly exposed to the underlying economics it has temporarily detached from.

In levered cyclical models like Avis, risk is not defined by recent performance, but by how quickly underlying conditions can reverse. Today’s move is not an anomaly; it is a preview of how quickly price can adjust when the structural imbalance begins to unwind.

In our assessment, SRS’s probable endgame remains unchanged. The conditions for a take-private are already substantially in place: control without a premium paid, management aligned, and a float too small to resist. What remains is timing and price. As the stock moves further away from peak levels, the path toward a transaction becomes more feasible.

The story has carried it this far. The structure is starting to give. At recent price levels following a vertical expansion, the margin for error has effectively disappeared. Buying at these levels is where investors get hurt, after vertical expansion– just because the move has started to settle does not mean it is safe.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions-long, short, or otherwise-in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.