$ASTC: Five Pivots, $262M Lost, and an Unaccountable CEO

From SPACEHAB heritage COVID breath tests, to moonshot buzzwords: backed by thin revenue, a handful of customers, and dependence on capital markets.

Executive Summary

Astrotech Corporation has spent a decade randomly (but at the same time strategically, according to its executives’ deep pockets) rotating from one business model to another. Since 2018, the company has repositioned itself five times, going from aerospace to industrial tech to COVID breath analysis to airport security to its current standpoint as a defense and aviation security play anchored to a pilot program of the Tracer 1000 explosives detector. Narrative in which they have hooked themselves just to attract speculative capital. All of the pivots since its inception have resulted in $262 million of destroyed shareholder value, $1 million of annualized revenue, and a balance sheet for just about 4 months of cash runway.

The man at the center of every pivot is Thomas Boone Pickens III, who simultaneously holds the titles of CEO, CTO, Chairman of the Board, and Principal Financial Officer, four roles in total that have absolutely no independent oversight, representing a massive governance red flag that, adding to his past history, raises true alarms. This is not the first time Pickens has been involved in a conflict of interest.

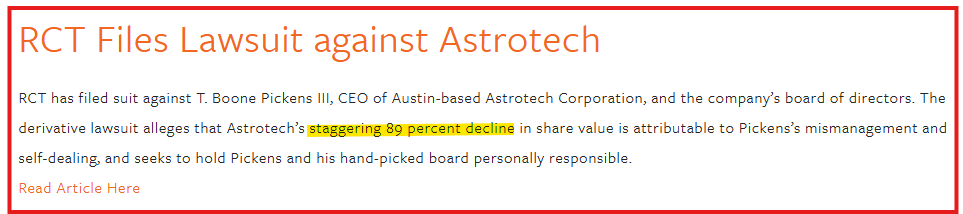

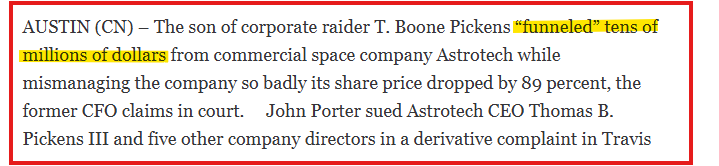

In 2013, a shareholder derivative suit alleged that Pickens “mismanagement and self-dealing” drove an 89% share price decline. His former CFO, John Porter, sued him separately, alleging he “funneled tens of millions of dollars” from Astrotech to subsidiaries via loans characterized as fraudulent transfers and billed over $100,000 in personal expenses to the company in violation of his own employment agreement. Both cases produced a documented behavioral pattern that the current 10-Q quietly shows; one CEO’s son-in-law received $211,000 in consulting fees for software services during the nine months ended March 31, 2026, equivalent to nearly 30% of total company revenue for the same period, approved by the company, which by coincidence he is judge, jury, and executioner.

The filings describe a capital consumption vehicle with 4 months of runway, a CEO who answers to no one, and years of accumulated losses that have consumed 95 cents of every dollar ever entrusted to this enterprise. Fugazi Research currently assesses ASTC shares value only momentum driven and fundamentally uninvestable at any level above zero, implying a 99% correction.

Fugazi Research Analysis

Astrotech has executed five distinct strategic pivots since 2018 (aerospace, industrial tech, COVID breath analysis, airport security, and defense) without achieving commercial success in any of them; each pivot has been fueled with speculative capital inflows. The accumulated deficit stands at $262 million as of March 31, 2026, against total paid-in capital of $274 million, meaning that the company has destroyed 95 cents of every dollar ever invested in this company.

Thomas Boone Pickens III serves simultaneously as Chief Executive Officer, Chief Technology Officer, Chairman of the Board, and Principal Financial Officer. Currently there is no Chief Financial Officer, and all financial certifications are signed by one individual who has no checks and balances over him.

In 2013, Reid Collins & Tsai filed a shareholder derivative action alleging Pickens’ “mismanagement and self-dealing” were directly responsible for an approximately 89% share price decline. Former Astrotech CFO John Porter subsequently filed suit alleging Pickens funneled tens of millions of dollars from the parent company to subsidiaries via loans characterized as fraudulent transfers and submitted over $100,000 in personal expenses for company reimbursement in violation of his employment agreement.

For the nine months ended March 31, 2026, the company paid $211,000 in consulting fees to an individual identified as the son-in-law of the Chief Executive Officer for software services. This amount equals roughly 30% of total company revenue for the same period.

For the three months ended March 31, 2026, one customer accounted for substantially all of the $99,000 in service revenue. Total Q3 revenue of $343,000 was generated across a handful of relationships with no evidence of a diversified or expanding customer base after three-plus years of commercialization effort.

The company operates six wholly owned subsidiaries ( ATI, 1st Detect, AgLAB, BreathTech, Pro-Control, and EN-SCAN). Of these, only one generates substantially all product revenue. Six operating entities, six cash-burning structures, and only one revenue-generating product.

Series D Preferred Stock (280,898 shares outstanding) converts to common stock on a 1-to-30 basis, producing 8,426,940 shares upon full conversion against 1,758,953 common shares currently outstanding. Meaning there is a full risk of dilution overhang that could expand the outstanding shares by a factor of 5.8x. The holder of Series D shares can convert at their sole discretion.

Based on the documented fact that Astrotech Corporation generates $1.05 million in annualized revenue against $14.9 million in annualized cash burn, has never produced a single dollar of positive cash flow from operations in its history, has destroyed 95 cents of every dollar ever invested through five consecutive failed strategic pivots, has a serious governance risk and conflict of interest, Fugazi Research considers ASTC’s shares uninvestable and of ZERO fundamental value.

Financial Summary

Total liquid assets as of March 31, 2026 amount to $6,582,000 (including cash and short term investments). Considering an annualized burn rate of $14,887,000, the true runway for the company is just about 4 months.

The company’s short-term investment portfolio went from $15,108,000 at June 30, 2025 to $3,903,000 at March 31, 2026 representing a 74.2% reduction in nine months. The company is not investing but liquidating its reserves to fund operations and presenting the proceeds as positive investing cash flow.

Nine-month revenue amounted to $787,000 compared to operating expenses of $11,152,000 for the same time period. The business only covers 7 cents of every dollar it spends.

Product revenue collapsed from $543,000 to $220,000 for the nine-month period (a 59.5% decline year-over-year).

$740,000 for stock based compensation for the nine month period. This non-cash expense equals 94% of total revenue for the same period. The company is compensating employees and directors at a rate nearly equal to what it earns from customers.

Accumulated deficit stands at $262 million vs $274 million of total invested capital, at this rate the company has destroyed 95.4 cents of every dollar ever invested in it.

Working capital declined from $19,524,000 at June 30, 2025 to $9,494,000 at March 31, 2026 a roughly 50% reduction in working capital over nine months driven entirely by investment liquidation, not operational improvement.

Series D dilution math: 280,898 preferred shares converting at 30-to-1 equaling roughly to 8,426,940 new common shares potential dilution, representing a 6x potential dilution overhang.

Source: Astrotech Corporation, Form 10-Q for the quarterly period ended March 31, 2026, filed May 14, 2026.

Source: Reid Collins & Tsai LLP, Shareholder Derivative Lawsuit Press Release, September 12, 2013

Source: Courthouse News Service, “Pickens Family Feuding Over Tell-All Blog,” parallel litigation context

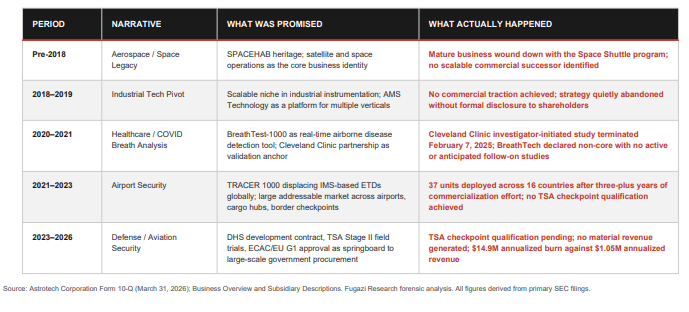

The Pivot Pattern: One Platform, Many Markets

Astrotech Corporation was incorporated in 1984 as SPACEHAB, a NASA contractor providing pressurized modules for Space Shuttle missions. That business (the only one in the company’s history that generated meaningful, recurring revenue) ended when the Space Shuttle program wound down. Since then, the company has repositioned its identity five times in eight years, only highlighting the lack of direction and the opportunistic nature of the top leadership, who has proven time after time to be more inclined to extract capital from speculative investments rather than rely on a single business or going full into a specific industry, but jumping around from narrative to narrative depending on the timeline and the hot theme of the moment.

Each pivot followed the same script, a new subsidiary formation or product announcement, a wave of press releases positioning the technology as addressing a massive addressable market, speculative capital inflows, and then quiet operational failure with no formal acknowledgment that the prior thesis had not worked, all pivots replacing each other time after time.

However, the financial signature of the pattern is equally consistent, the company has never generated positive operating cash flow in any fiscal year of its existence. The accumulated deficit grew from approximately $190 million in 2018 to $262 million as of March 31, 2026 ($72 million consumed across the last three pivots alone).

What sustains the operation between pivots is not revenue, it is equity issuance and reserve liquidation. The short-term investment portfolio declined from $15,108,000 at June 30, 2025 to $3,903,000 at March 31, 2026 representing by itself a 74% drawdown in nine months. When that reservoir empties, the only remaining financing mechanism is a Shelf Registration capped at $1,974,354 under Baby Shelf limitations, which at current stock prices can be tapped at any moment when the stock closes above $54, leaving the door open to another round of dilutive potential.

The Governance Structure

Astrotech Corporation has a complete governance absence. Thomas Boone Pickens III holds four titles simultaneously: Chief Executive Officer, Chief Technology Officer, Chairman of the Board, and Principal Financial Officer, as of their latest filing there is no Chief Financial Officer in the company, nor an independent board chair. The individual who sets strategic direction, controls the technology roadmap, chairs the meetings at which his own performance is evaluated, and signs the financial certifications of the company. Creating an environment in which there is no check and balances system, everything runs through one person, and that person reports to no one.

This structure has historical precedent at Astrotech specifically. In 2013, the plaintiffs’ firm Reid Collins & Tsai filed a shareholder derivative action alleging that Pickens’ “mismanagement and self-dealing” was directly responsible for an approximately 89% decline in the company’s share price. The suit sought to hold him and the board personally liable. Separately, former Astrotech CFO John Porter filed suit alleging Pickens had funneled tens of millions of dollars from the parent company to subsidiaries through loans Porter characterized as fraudulent transfers, and had submitted over $100,000 in personal expenses for company reimbursement in violation of his own employment agreement. Both instances produced a documented behavioral record that predates the current filing period by more than a decade.

Source: Reid Collins & Tsai LLP, Shareholder Derivative Lawsuit Press Release, September 12, 2013

What the governance structure has produced over its twenty four year existence is a $262 million financial hole in the in the form of accumulated losses, five failed strategic pivots, a CEO who acts as judge, jury and executioner, and a board that renews its own anti-takeover protection every December like clockwork. The board which by the way is chaired by the same man it is supposed to oversee.One man controls the strategy, the technology, the finances, and the board room, but the losses belong to shareholders.

Inside the Numbers

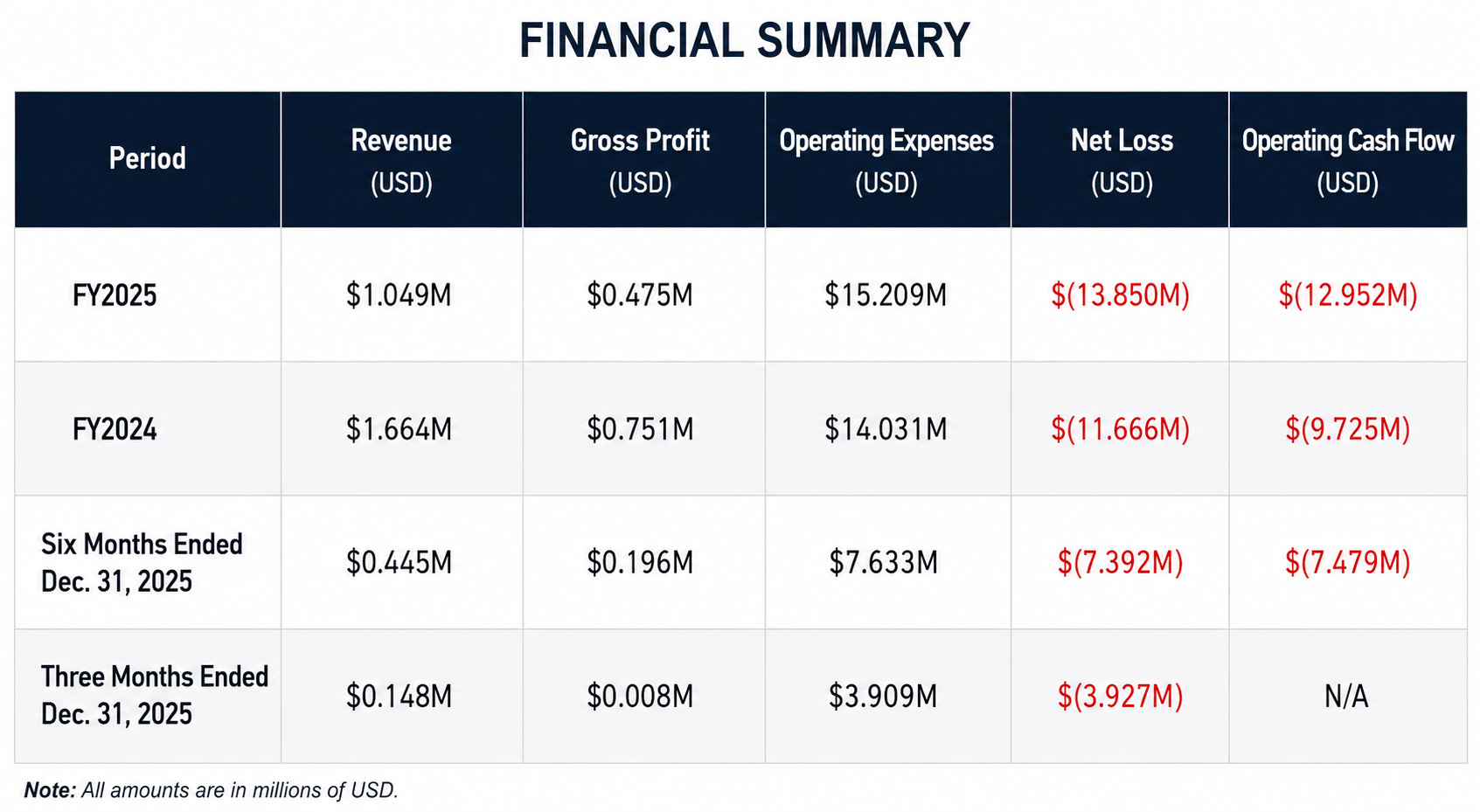

In FY 2025, Astrotech spent roughly $14.50 in operating expenses for every $1 dollar of revenue. For the three months ended December 31, 2025, the company produced $148,000 in revenue and $8,000 in gross profit while absorbing $3.909 million in operating expenses in the same quarter.

The cash position did not stay near $3.1 million because the business funded itself. For the six months ended December 31, 2025, Astrotech consumed $7.479 million in operating cash. The balance held steady because the company systematically liquidated its short-term investment portfolio (created by the way from previous equity raises) and presented the proceeds as investing activity. The investment portfolio that stood at $15.1 million at June 30, 2025 had been drawn down to $3.9 million by March 31, 2026, representing a $11.2 million drawdown in nine months. As of current numbers the portfolio is nearly gone,and when it empties, the operating cash burn will land directly on the cash balance with nothing left to offset it.

Operating cash outflow for the nine months ended March 31, 2026 was $11.165 million against total liquid assets of $6.582 million at quarter end. The company is burning more in nine months than it currently holds in total liquidity. Equity remains practically the only exit or alternative of the runway. The company is telling shareholders, in its own filing language, that survival depends on capital markets it does not control, at terms it cannot predict, through a Shelf Registration capped at $1,974,354 enough only to fund six weeks of operations.

The Product Reality: TRACER Economics Are Thin

The 2019 Form 10-K describes TRACER 1000 as the first certified mass-spectrometer-based explosives trace detector and says ECAC or TSA certification is necessary to sell into the airport market. The filing states that TRACER entered ECAC evaluation in 2018 and officially launched in June 2019. The same filing says TSA programs carried no assurance of approval.

In May 2026, it announced ECAC/EU G1 approval for aviation security. The problem is conversion. Years of certification, testing, deployments, and market claims have not produced financial scale. Fiscal 2025 revenue declined to $1.0 million because 1st Detect sold fewer devices compared to the prior year, according to the company’s own financial results release. The reality is that the product is a weak public-equity story. TRACER has not given Astrotech a self-funding business.

The Rotating Narrative Stack

After TRACER, Astrotech’s story becomes a sequence of new market opportunities built on the same underlying platform. Rather than developing entirely new technologies, the company repeatedly repositions its core detection capabilities toward different industries and use cases.

The pattern was already visible in the 2019 Form 10-K. At the time, management was promoting AG-LAB-1000 as a solution for agricultural testing, particularly within the pesticide, hemp, and cannabis markets. The product was marketed to growers, distributors, retailers, regulators, and law enforcement agencies as a way to rapidly detect pesticide contamination and reduce the risk of spoiled inventory.

By fiscal 2025, the same broad technology platform had been repacked into several new initiatives. BreathTech was described as developing BreathTest-1000, a breath-analysis tool to screen VOC metabolites that may indicate a compromised condition. Pro-Control was framed around industrial process control. EN-SCAN was framed around environmental testing and monitoring.

What stands out is how closely the company’s risk disclosures track these product narratives. Alongside the market opportunity, Astrotech repeatedly reminds investors that commercialization remains uncertain. The filings note that the company may never successfully develop BreathTest-1000 or its other products, that AgLAB remains heavily dependent on the hemp and cannabis industry, that cannabis-related equipment could create Controlled Substances Act (CSA) risks, and that AgLAB could eventually face regulation from agencies such as the FDA or ATF.

The strongest line sits in the company’s own risk section: “Our business units are in the development stage. They have earned limited revenues and it is uncertain whether they will earn any revenues in the future or whether any of them will ultimately be profitable.”

That single sentence captures the central reality behind every new product announcement. Regardless of how the narrative shifts (from agricultural testing to breath analysis, industrial controls, or environmental monitoring) the underlying challenge remains the same: no business whatsoever.

The 2026 Moon Pivot

On May 27, 2026, Astrotech announced that its Board approved a strategic lunar resource and infrastructure initiative.

The language was pure hype detached from the reality of the reputation of the company’s recent past. Astrotech is riding the coattails of the hot space industry, just as they’ve done with other hot industries throughout their history. Lunar resource development. Autonomous lunar industrial infrastructure. Moon-based advanced computing. Semiconductor manufacturing. Silicon-28. Helium-3. AI infrastructure. High-performance computing. Quantum fabrication. NASA Artemis. CLPS. Commercial lunar transportation systems. All space jargon to hype their stock as much as possible with the ultimate goal of a highly possible lucrative financing which they desperately need to remain in business.

The hype driven narratives are clear in their press releases. In there it says the initiative is intended to position Astrotech to “evaluate” emerging opportunities. Astrotech “expects to evaluate” infrastructure concepts. The initiative remains in an “early evaluation and development phase.” No customers, contracts, funded missions, partners or budgets are ever disclosed.

That is the key turn. After years of terrestrial instrumentation narratives, the company returned to space branding through lunar resources and quantum computing. The old space identity came back. The current income statement did not change with it. Astrotech once again trying to ride sector hype for a pump into a potential big raise.

Capital Structure: The Shelf Is Open

The January 2026 Form S-3 gives Astrotech a registered path to issue stock, preferred stock, debt securities, warrants, and units up to $30 million.

In practice, the company’s immediate financing capacity was much smaller. The same filing calculated public float at approximately $5.92 million, triggering the SEC’s baby-shelf limitation and restricting sales to roughly $1.97 million of securities during the applicable period.

As of January 26, 2026, Astrotech had approximately 1.76 million common shares outstanding against a pool of 250 million authorized shares.

The Series D Preferred Stock occupies a particularly influential position. According to the January 2026 S-3, Series D holders have liquidation preference over junior securities, and certain actions that would adversely affect the Series D class require approval from those holders. In other words, the capital structure contains multiple layers of claims and protections that extend beyond the common stock.

The company’s history also reflects repeated adjustments to that structure. The 2025 Form 10-K notes that a 1-for-30 reverse stock split became effective on November 22, 2022, with corresponding adjustments to common shares, warrants, options, and the conversion mechanics of the Series D Preferred Stock.

Taken together, this is not a simple dilution story driven by a single financing instrument. It is a capital structure built with multiple avenues for future massive dilutive financing and recapitalization.

That flexibility matters because the operating business continues to consume cash while pursuing commercialization across multiple development-stage initiatives. The products create the narrative, but the capital structure provides the runway. One generates the need for funding; the other preserves the ability to obtain it.

Pickens, Series D, and the Control Layer

Thomas B. Pickens III sits at the center of Astrotech’s modern filing record.

In 2019, Astrotech disclosed two capital raises involving Pickens and another long-term accredited investor. One transaction sold Series B convertible preferred stock to Pickens and common stock to the other investor. Another sold Series C preferred to the investor and Series D preferred to Pickens. The Series D preferred was convertible into common stock at the option of the holder.

The same 2019 Form 10-K disclosed a separate $1.5 million secured promissory note issued to Pickens at 11% interest, secured by collateral of the company and subsidiaries and guaranteed by subsidiaries.

By 2026, the Series D preferred still mattered. The S-3 states that 280,898 Series D Preferred shares remained issued and outstanding as of January 26, 2026.

The governance concentration is also visible. A February 2026 Form 8-K was signed by Pickens as Chief Executive Officer, Chief Technology Officer, Chairman of the Board, Principal Executive Officer, and Principal Financial Officer.

The compensation table adds another uncomfortable ratio. Pickens’ 2025 total compensation was $954,851. Fiscal 2025 revenue was $1.049 million. Net loss was $13.850 million.

Rights Plan: The Gate Around the Cap Table

Astrotech’s rights plan was adopted on December 21, 2022. The January 2026 S-3 states that the rights plan gave each shareholder one preferred share purchase right for each common share, with a purchase price of $58.00 per one one-thousandth preferred share. The plan was extended in December 2023, December 2024, and December 2025. The latest extension pushes expiration to December 20, 2026 unless extended again or redeemed earlier.

For a company with small revenue, a large authorized share base, remaining preferred securities, recurring losses, and a live shelf, the rights plan belongs in the report. It is part of the control architecture.

Conclusion

Astrotech is not a real company, it is a capital consumption machine disguised as the “hot theme of the moment business” that has operated continuously for over two decades without ever producing a self-funding business. The filing records throughout the years show a company that has burned $262 million in accumulated losses across five strategic pivots, never once generating positive operating cash flow, with a CEO who controls the strategy, the technology, the board room, and the finances simultaneously (same individual whose former CFO alleged in civil litigation that he funneled company funds through fraudulent transfers and billed personal expenses to the company he ran).

The May 2026 lunar announcement is not a strategic pivot but a mere press release. Lunar resource development, quantum fabrication, Silicon-28, Helium-3, autonomous lunar industrial infrastructure, none of these things come with a customer, a contract, a partner, or a budget. What it comes with is a company that had $445,000 in six-month revenue and a $7.4 million net loss at the time of the announcement, a Shelf Registration that funds six weeks of operations, and a CEO whose compensation of $954,851 in fiscal 2025 exceeded total company revenue by nearly every measure that matters.

The moon story is the company’s sixth pivot, and like the five before it, it arrives precisely when the market has something shinier to chase. The SpaceX IPO fever is the new theme the company can monkeybranch to, at the time oblivious retail capital is flooding into anything with a rocket or a radar attached to it. And now the moon, announced within days of the most anticipated space IPO in a generation, with zero customers, zero contracts, zero budget, and zero credibility left to spend. Fugazi Research considers ASTC common equity uninvestable at any price above zero.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions-long, short, or otherwise-in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.