$AKAN: A Half-Baked Cannabis Company Where Shareholders Get Smoked

6.7 million resale shares sit behind a 500,000-share count.

Executive Summary

Akanda has been trading the same way for years (sharp, narrative-driven spikes followed by steady, grinding fades). The business has never caught up, and it hasn’t needed to. Each cycle resets with a new angle, a tighter float, and just enough momentum to pull buyers in before the underlying structure reasserts itself. The latest telecom pivot doesn’t break that pattern. It looks like the next version.

What’s different now is the starting point. The legacy cannabis business is gone, the replacement asset is small, and the balance sheet is materially worse. Cash is down to roughly $1.3 million, debt has expanded to approximately $26 million, and the company continues to operate under going concern language. The structure is tighter, the margin for error is gone, and the amount of supply sitting behind the current float is larger than at any point in the company’s history, with over 6.7 million shares registered for resale (reverse split adjusted) against roughly 534.4 thousand shares outstanding, according to the company’s April 2026 6-K filing.

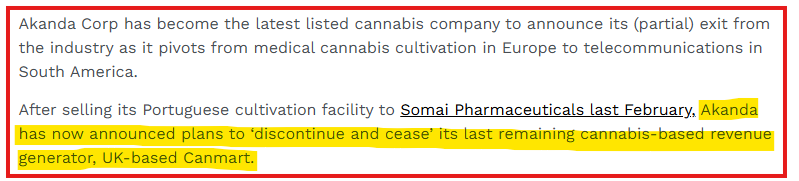

It is worth pausing on what Akanda actually is: a Canadian cannabis distributor that shut down its only revenue-generating subsidiary in March 2025, as disclosed in its annual report; has never harvested a single unit of product from its British Columbia cultivation facility; and has now pivoted into Mexican telecommunications infrastructure following its August 2025 acquisition of First Towers & Fiber Corp., a sector with no operational, regulatory, or strategic overlap with anything the company has previously operated.

The setup is more fragile than at any prior point in the company’s history. Less cash, more debt, a larger overhang, a replacement business that is real but immaterial, and a financing structure that is designed to convert into selling pressure. The story may trade, but the structure will not hold.

Source: Akanda Corp. Form F-1/A2, Filed March 20, 2026.

Source: Akanda Corp. Form F-1, Filed March 20, 2026.

Fugazi Research Analysis

Akanda Corp (AKAN) is a 2022 Nasdaq-listed company that has never achieved true commercial scale, generated meaningful revenue, or achieved any path to profitability. In April 2025, Akan lost Canmart Ltd., its sole operating subsidiary and its only source of revenue in the previous year. Which, in theory and based on our analysis, would bring the already small revenue ($836,664 in FY 2024) to zero without its subsidiary.

On May 1, 2026, the company cited an inability to compile required disclosures without unreasonable effort or expense. However, they included a preliminary financial summary which disclosed a full year 2025 revenue of approximately $258,075 against operating expenses of approximately $4,827,720, which represents an operating loss ratio of 18 dollars spent for every 1 dollar earned.

On March 26, 2026, Akanda issued a press release announcing a $2 million contract for fiber infrastructure in Mexico. However, the spread is across a 10-year term, and the contract generates approximately $200,000 per year in contracted revenue against an operating burn rate of more than $4 million annually.

Since its Nasdaq listing in March 2022, Akanda has raised capital entirely through equity issuance and debt, never through operations. In 2024 alone, the company executed seven or more registered direct offerings and underwritten public deals, raising approximately $11.5 million at share prices ranging from $32.48 to $2.00.

Christopher Cooper is central to the First Towers transaction. The Form F-1/A states that Cooper was a director of Akanda and a co-founder, shareholder, executive, and director of First Towers. The same filing states that he recused himself as an Akanda board member for purposes of the transaction and was removed from Akanda’s audit committee.

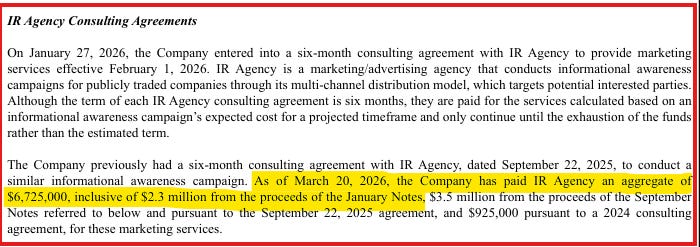

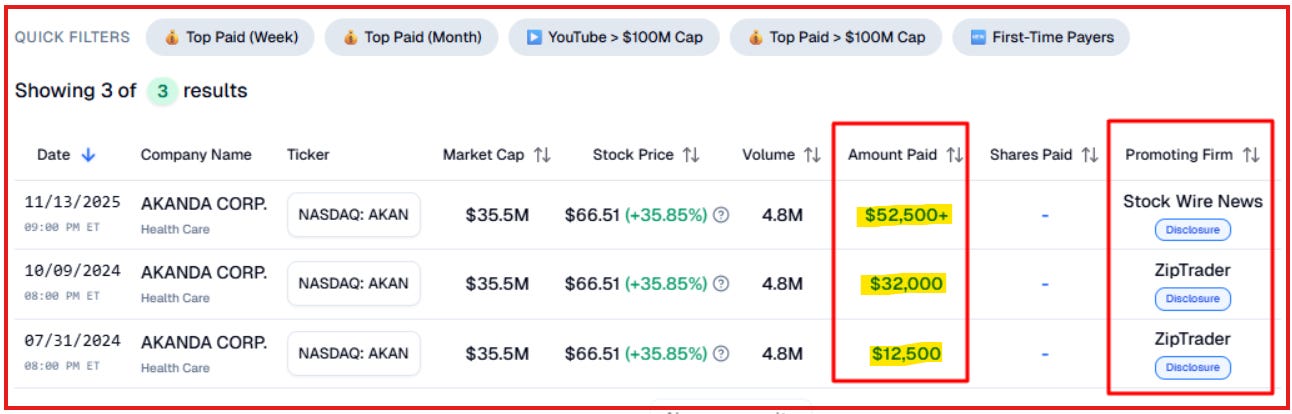

Between September 2025 and January 2026, Akanda raised $19 million in toxic convertible notes and paid $6.725 million (35% of gross proceeds) to IR Agency, LLC, a retail stock promotion firm. This is a documented dilution loop: raise notes, pay promoters to push stock, note holders convert at an 85% VWAP discount, price falls, execute a reverse split, and repeat.

Since March 2023, Akanda has executed six reverse stock splits, the last one being a 1 for 4.5 (April 2026). The cumulative ratio is approximately 1 for 56,340. The company has explicitly stated its intent to execute additional splits in 2026 and beyond, with Board authorization for a cumulative ratio of up to 1 for 100 without requiring further shareholder approval.

As of April 9, 2026, following their most recent reverse split, Akanda had approximately 534,400 common shares outstanding. The January 2026 convertible notes, adjusted for the 1-for-4.5 April 2026 reverse split, represent approximately 6.7 million shares registered for resale (more than 12 times the current float) at an adjusted floor conversion price of approximately $1.14 per share.

The filing record shows a failed legacy cannabis platform, a small replacement telecom asset, heavy financing reliance, promotional spending funded from note proceeds, repeated reverse splits, and a registered conversion-share supply far larger than the visible share count. We consider AKAN shares to be uninvestable at any price above liquidation value, which, in this case, considering the debt structure, cash burn rate, and going concern of the business, is likely near ZERO.

AKAN Financial Summary

Total accumulated deficit stands at $57.4 million, against $63.3 million in total paid-in capital since inception, meaning the company has accumulated losses equal to 91% of every $1 invested in it.

For the fiscal year ended December 31, 2024, Akanda generated $836,664 in revenue entirely from Canmart’s UK cannabis distribution operations. That subsidiary was shut down in March 2025.

Preliminary financial results show 2025 revenue of approximately $258,075, which represents one-third of what the company spent on salaries alone during the same period and less than one-twentieth of its total operating expenses of approximately $4,827,720.

Net loss from continuing operations for FY2024 was $3.26 million against $836,664 in revenue (a loss margin of approximately 391%). The operating loss was $4.38 million for FY2024.

Akanda burned through $3.9 million in operating cash during FY2024, up from $1.5 million the year before, a year-over-year increase of approximately 165%.

Cash fell from $3.8 million at December 31, 2024, to approximately $1.3 million as of February 28, 2026, a 66% decline in roughly 60 days following the January 2026 note offering, highlighting continued cash burn even after financing activity.

Akanda raised approximately $10 million through equity issuance during fiscal year 2024 alone, while generating $836,664 in total revenue. That is a ratio of roughly $12 in revenue from selling shares for every $1 in revenue from selling a product.

In twelve months, Akanda’s total debt went from $3.64 million to approximately $26 million. A 7x increase in debt engineered not by growth, but by the acquisition of a director-controlled company whose own pre-existing debts were assumed at closing.

Source: Akanda Corp. Form 20-F, fiscal year ended December 31, 2024. Filed April 30, 2025.

Source: Akanda Corp. Form F-1/A3, Filed March 20, 2026.

Source: Akanda Corp. Form 6-K, Exhibit 99.1, Filed March 26, 2026.

Source: Akanda Corp. Form NT-20F, Filed May 1, 2026.

The Setup

In the most recent development, AKAN notified Nasdaq that it will not be able to file its Form 20-F on time. The company cited an inability to compile the required disclosures, offering no further explanation. Besides the fact that these types of developments are true red flags, the most important development is that the company itself is now recognizing only $258,075 in revenue for the twelve months ended December 2025. This all stems from the First Tower fiber-optic contract and confirms our thesis that their cannabis business is practically dead. To confirm that the company is pivoting away from marijuana, one just needs to look at their latest filing and their most recent NT-20F. There is no single revenue source from their purported cannabis-related business. This is all disclosed by the company in plain sight. The company did not even make $1 in the weed industry since February 2025, with no hint of resuming weed operations in the future.

Source: Akanda Corp. Form NT-20F, Filed May 1, 2026.

Source: Akanda Corp. Form NT-20F, Filed May 1, 2026.

The run-up of AKAN began on April 22, 2026, when breaking news about the Trump administration’s expected reclassification of marijuana as a less dangerous drug. On Thursday, April 23, the US policy change went through. However, AKAN isn’t even focused on marijuana anymore. The company’s social media posts feature outdated stock images of marijuana and have not been updated since 2022. Their last paid promotions didn’t even mention anything about marijuana. The paid promotion mentioned a new large fiber network in central Mexico related to telecommunications infrastructure. (A zero relationship with the marijuana business.) This is misleading to potential momentum traders who are buying on the Trump marijuana headline. Retail investors are not looking deeper into the company and realizing it has pivoted to something completely different from the marijuana industry. AKAN is focusing marginally more on its fiber business in Latin America, which has nothing to do with weed and is also a minimal-scale revenue stream at best. As for a company that burned almost $5 million in operating expenses in FY2025, $258K in revenue is meaningless to cushion the already enormous and increasing deficit. If the company were focused on marijuana, they would likely have mentioned it in their paid promotions, which they have spent more on than the company's market cap.

Source: Akanda Corp. Form NT-20F, Filed May 1, 2026.

The Non-Existent Business

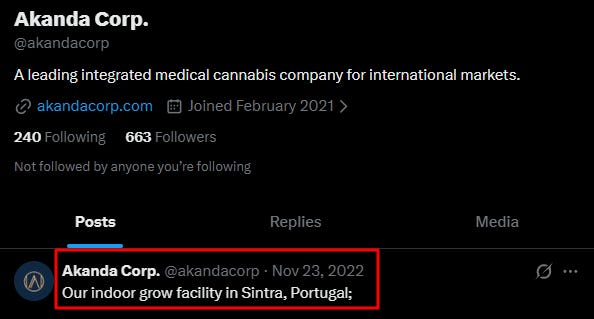

On their social media, Akanda has not updated any new information since November 2022; in that same post, they are promoting their indoor grow facility in Sintra, Portugal. However, it is important to note the fact that the Portugal facility has been sold since the beginning of 2024.

Back in 2022, AKAN was actually involved in the marijuana industry, as they had $2.6 million in revenue from cultivation and distribution. In 2023, they had $2.1 million, followed by $836,000. The pattern is clear: their weed business was declining and not working out, and to remain solvent, they would have to come up with anything they could to stay listed on the public markets. The miracle solution: fiber optic towers in Mexico doing $200k a year, while their shareholders get diluted as they desperately hold on to the idea that their investment is in the future of marijuana. As they are getting diluted in perpetuity, the market cap of AKAN keeps shrinking, down to a minuscule $1.5 million by April 23rd, 2026, during the run-up on Trump administration weed news.

While the company describes itself as a “leading integrated medical cannabis company,” it’s clear that Akanda is not a cannabis company; it has not been one for over a year, and now its own investor page and social media accounts have not acknowledged this.

What stands out most is the stock rising by over 2,000% in less than 2 weeks. This is artificially elevated at these levels due to an imbalance between supply and demand, as the stock is coming off a recent reverse split. AKAN had a reverse split on April 12 to keep the illusion of compliance or to maintain themselves out of the radar of regulators, as this is done in a consistent basis under different ratios to maintain the minimum price bid in order to keep existing in the market and taking advantage of their capital structure, they had to do a reverse split because their stock price was too low and trading for under a dollar for more than 30 days. When they did their sixth split in 3 years of 4.5 to 1, their float became 540,000. Their float is small for now; it is easy to manipulate to higher prices to do toxic, death-spiral financings, which will lead to more and more reverse splits until there is nothing left.

The legacy cannabis business no longer provides a base, and the company’s 2024 revenue came from Canmart; it completely ceased operations in 2025. The remaining now is a low-revenue pivot into a Mexican telecommunications asset that carries a new story but lacks true scale. This also generates problems on its own, as the same telecom transaction added leverage, including a $14.1 million note at 16% interest, while subsequent financings introduced a large convertible component. (A $19 million worth of convertible notes using toxic discount formulas.)

Source: Akanda Corp. Form F-1/A3, Filed March 20, 2026.

What remains is a company with 500k shares outstanding, against almost 7 million shares tied to resale registration just by convertibles alone. Or, in a simple context, if we had to define Akanda in 2026, it would be a failed business that has lost its original revenue base, replaced it with a smaller asset, layered on additional liabilities, and now carries a multiple of its float in potential supply sitting behind it.

Ownership and Float Reality

Akanda looks like a tight float only if investors ignore the registered conversion shares underlying the reported share count. The Form F-1/A destroys that argument: the visible share count is small, but the registered conversion-share pool is more than 12x larger. As of March 20, 2026, Akanda reported only 2,404,882 common shares outstanding, while the Form F-1/A registers 30,314,961 shares for resale upon conversion of the January Notes. The reported float appears tight only because the registered conversion supply has not yet fully been reflected in the common share count.

The problem is what happens next. Those shares are not passive. They come with conversion mechanics tied to discounted pricing, which creates a natural incentive to resale registration into sellable inventory once conversion shares are issued.

This is also where the impact of repeated reverse splits becomes harder to ignore. According to company filings, Akanda has executed six reverse splits since 2023, with a cumulative ratio of roughly 1-for-56,340. Adjusted for those splits, the current ~$60 price equates to a pre-split value measured in pennies — roughly in the $0.02–$0.05 range depending on the reference point — but in reality, we’re talking value in fractions of a penny, not dollars. In other words, what appears today as a high-priced equity is, on a normalized basis, still trading at levels typically associated with distressed microcaps.

That matters more than it seems. Reverse splits don’t create value — they compress share count and reset optics. The effect is psychological as much as mechanical. A $60 stock reads differently than a $0.03 stock, even if the underlying economics are the same. In names like this, that difference tends to attract incremental buyers at exactly the point where underlying supply is preparing to come through.

That disconnect between perceived float, visible price, and actual supply is the core of the trade.

Source: https://app.askedgar.io/ticker/AKAN/dilution

Promotion and Distribution

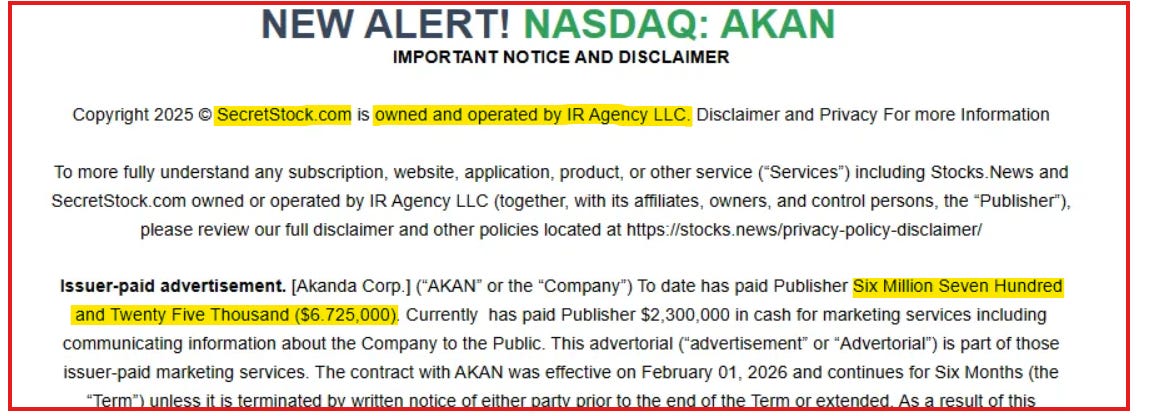

During the events of the paid promotions, it is important to mention that the company has spent 4x its market cap at the time, considering that at the time of their latest reverse split, their market cap was around $1.5 million (market cap April 12, 2026), against $6.7 million spent in paid promotions in the past two years to the IR Agency alone. Nobody can argue that AKAN has spent more on paid promotions than what their company is worth. This is a fact that is not only clear in all the disclaimers of the paid promotions, but it is also clearly mentioned in the filings.

Source: Akanda Corp. Form F-1/A3, Filed March 20, 2026.

Between September 2025 and January 2026, the company raised approximately $19 million in convertible notes, and a portion of those proceeds was directed toward “investor awareness campaigns” AKA “promo pumps”.

Companies with real operating traction and sufficient internal funding do not need paid promotion to generate investor demand; companies with a history of blatant paid stock promotion are notorious for pump-and-dump trading activity. The company pays for a “marketing campaign,” which generates temporary volume from unsuspecting, naive investors who eventually become the liquidity for those who paid for the campaign in the first place. The cost of the “marketing campaign” is covered by the rug-pull dumping of shares, leaving the losses to oblivious retail investors.

In structures like this, promotions are likely engineered events created by top management to obtain financing on an already distressed balance sheet, and they also don’t have a path to a true revenue or income stream. Discounted convertibles require liquidity to convert into, and that liquidity is often supported by visibility and outreach targeted at retail participants. By using StockPromotionTracker.com, we can see the recent documented history of paid promotions in which AKAN has been involved. The unique situation with AKAN is that the company openly admits it runs paid promotions. Usually, the modus operandi of shady companies is to cover their tracks when it comes to paid promotions or “marketing campaigns.” The fact that AKAN explicitly states in their filings that they engage in paid promotions is not only a red flag but also a warning to those buying. In the case of AKAN, the company can afford not to hide its paid promotions because the supply of its stock is so low that a small amount of volume would push it up, and at the same time, short sellers would have a tough time shorting it because of the tight supply, which could lead to a squeeze. The reverse split, together with the paid promotions, indicates the squeeze was likely manufactured.

The pattern is consistent. Capital is raised, attention increases, and the stock finds unsuspecting buyers. The mechanics behind it do not change, while history shows the rest.

Source: IR Agency LLC “Secret Stock” (AKAN) .

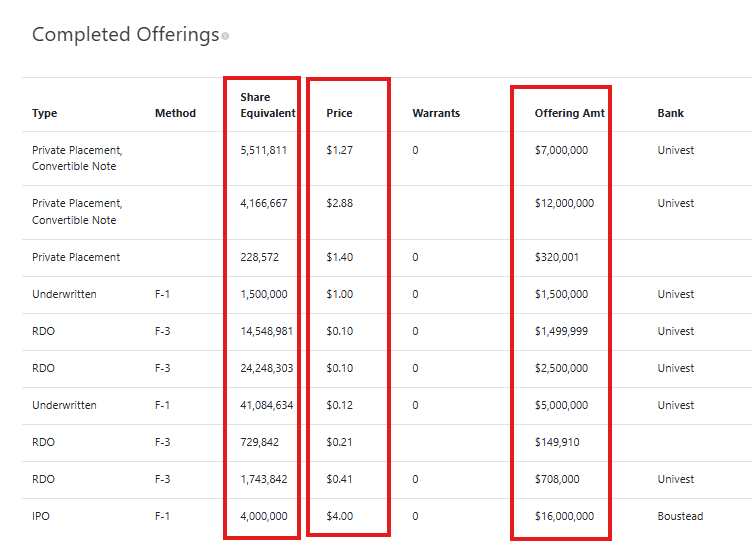

The Structure

To date, the company has completed 10 offerings totaling approximately $46 million USD, equivalent to 30x its standard market cap. Its IPO and subsequent offerings have all been done by lower-tier investment banks and underwriters. Just as with companies with a history of paid promotions, it is no secret that lower-tier underwriters are associated with shady companies. The archetype of this is AKAN. A company that, unaware, investors and hobbyist traders think is a weed company, when in fact it is a fiber optic tower company on the outskirts of Mexico for lower-end cell phone services. This shows that the company is not in the business of producing, distributing, or improving operational efficiency. But in complete capital market dependency.

Source: Dilution Tracker AKAN Completed Offerings

At the current scale, the revenue contribution is minimal relative to operating burn, expanded debt load, and the registered conversion-share overhang. Even with growth, the business would need to scale materially just to support the existing structure before any value accrues to equity.

The more important change is what came with the acquisition. Akanda layered on significant obligations, including a high-interest, secured note. That shifts the equation. The question is no longer whether the telecom business exists; it’s whether it can scale fast enough to carry the liabilities, interest burden, and dilution structure already attached to it. The telecom pivot gives Akanda a new operating story, but it does not change the financial reality underneath it.

The need for continuous dilution

Over the past year, the company moved from a lightly levered structure to one that is defined by its obligations. Total debt after the First Towers transaction was approximately $26 million, up from just a few million the year prior, while cash has declined to around $1.3 million.

That shift changes everything. The company is no longer operating with optionality; it is operating against a balance sheet that requires capital, time, and execution. A meaningful portion of those obligations comes from the telecom transaction itself, including a $14 million note carrying a 16% interest rate and secured by substantially all assets. That in itself is not passive capital; rather, it sits ahead of a behemoth of equity and accrues regardless of the business’s performance.

From here, the company has limited ways to bridge the gap. It can either raise more capital through dilution (the path of least resistance) or attempt to grow into the obligations (no healthy lender would take the risk). Each path has implications, but none of them leave equity untouched.

Conclusion

At these levels, the stock is no longer being bought on what the business is; it’s being bought on what the move has been. The company isn’t even in the weed business anymore. They are installing fiber-optic towers in Mexico. They have completely shifted away from weed, yet the herd, groupthink mentality of momentum traders chasing the “next hot weed stock” is not even aware that the company is focusing on their towers in Mexico. AKAN has not had any income from weed in over a year; they dilute shareholders based on their outdated reputation of being in the weed industry.

In addition, the company’s existence at this point is to finance sleazy paid-promotion marketing companies rather than contribute anything productive to society.

The current tight supply setup can plunge sharply at any moment, with dislocating price action to the downside. Eventually, shareholders will be getting the short end of the stick as the company looks to dilute at current inflated stock prices, which they have done through 10 toxic raises in just 4 years. In essence, the company has burned through over 45 million in cash while its market cap dwindled to less than 2 million before the run-up on April 22, 2026.

The filings still show the same picture: the legacy cannabis business is gone, the replacement telecom asset remains small, cash is limited, and the liability structure has expanded beyond what the current business can support. A tight visible float can drive price, but the registered supply sitting behind it does not disappear; it works over time. Reverse splits may reset the optics, but they don’t remove the overhang.

At these levels, this ranks among the more fragile long-term investments in the market, reliant on continued momentum rather than underlying support. We consider AKAN’s shares to be uninvestable and to have zero fundamental value.

Disclaimer

The research, commentary, reports, and other materials published by Fugazi Research LLC (“Fugazi Research,” “we,” “us,” or “our,”) are provided solely for informational and educational purposes. Fugazi Research is an independent research publisher and is not registered as an investment adviser, broker-dealer, or commodity trading advisor with the U.S. Securities and Exchange Commission or any other regulatory authority.

All content published by Fugazi Research represents our opinions as of the date of publication and is based on publicly available information, independent research, interviews, and analytical judgment. Our opinions are inherently subjective, may be incomplete, and are subject to change at any time without notice. We do not undertake any obligation to update or revise our content to reflect subsequent events, market developments, or new information.

Nothing published by Fugazi Research constitutes investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security or financial instrument. The information should not be construed as tailored to the investment objectives, financial situation, or particular needs of any individual or entity. Readers should conduct their own independent research and consult their own financial, legal, and tax advisors before making any investment decision.

Fugazi Research, its affiliates, principals, members, employees, consultants, or clients may have positions-long, short, or otherwise-in the securities discussed, and such positions may change at any time for any reason, including risk management, market conditions, or liquidity considerations. We may trade in securities covered by our research before, during, or after publication, and we may reduce, close, or reverse positions at any time without notice. Readers should assume that Fugazi Research has a financial interest in the securities discussed.

Our research may include forward-looking statements, estimates, projections, or opinions that involve known and unknown risks, uncertainties, and assumptions. Actual outcomes may differ materially from those expressed or implied. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

While we believe the information we present is accurate and reliable, it is provided “as is” and “as available,” without any representation or warranty, express or implied, as to accuracy, completeness, timeliness, or fitness for any particular purpose. Fugazi Research disclaims any liability for errors, omissions, or losses arising from the use of our content.

By accessing or using Fugazi Research’s materials, you acknowledge and agree that Fugazi Research shall not be liable for any direct, indirect, incidental, consequential, or other losses arising from reliance on our research or opinions. Use of our content is entirely at your own risk.

All content is the intellectual property of Fugazi Research and may not be reproduced, distributed, or shared without prior written consent.

Appreciate you taking the time to write this; it resonated.